June 4, 2021

Market Commentary

Last week, the momentum in physical market continued, as spot HRC prices pushed higher, albeit at a slower pace than the recent trend. However, interpreting this slowed pace as a sign of weakness would be a mistake. While the current rally continues to prove itself incomparable to the historical data, we at Flack believe there are trends forming which need to be recognized and put into context. As we approach the half-way point of 2021, one pattern that has formed is the way mills are selling to the spot market. Historically, spot buyers were able to keep light inventories because of the 4-week average lead time. Now, mills are selling limited tons nearly two months in advance of delivery dates and closing their books early. Once they have a clear view on the remaining availability, they throw small quantities back into the market only to be immediately sold at significantly higher prices. In the beginning of the rally, when mills were producing below their full potential, the obvious conclusion for bearish analysts and commentators was that a correction was imminent as soon as production came back online. We are now 10 months into this rally, and based on the AISI capacity utilization, steel production has mostly recovered to pre-pandemic levels over the last few months, yet this pattern has continued. If you have not caught on by now, you are actively ignoring the facts on the ground. The apathetic, “take it or leave it” tone from the mills, should tell you one thing – mills know demand for steel is strong and broad, and if you will not buy at these levels, someone else will.

As unintended consequences from the global pandemic continue to impact all sectors of the economy, steel intensive sectors continue to be acutely impacted by broken supply chains. We believe these constraints are another reason the current rally will be more sustained than any in the past. In many areas, steel consumption is higher than it was before the pandemic, and steel demand is even higher than consumption. Moreover, once every car, home, appliance and manufactured good that consumers are willing to buy becomes available, service centers and OEMs will still have record-low inventories that are not sustainable for regular operations. As you will see in the economic data below, demand for steel has not flinched and our outlook for HRC prices remains bullish.

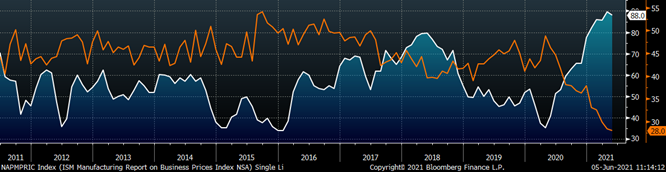

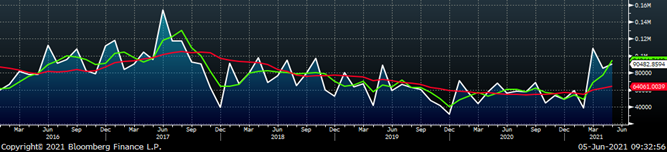

The chart below is the Platts Midwest HRC index (orange) and the ISM Manufacturing PMI (white).

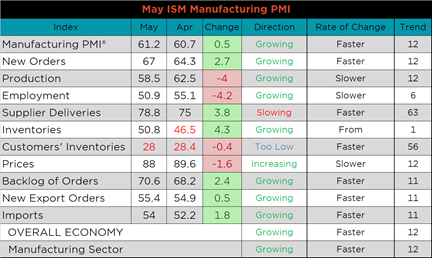

ISM PMI

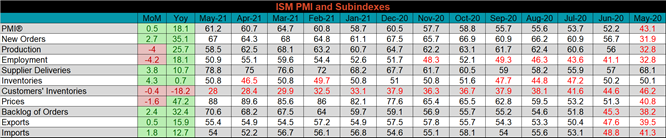

The May ISM Manufacturing PMI and subindexes are below.

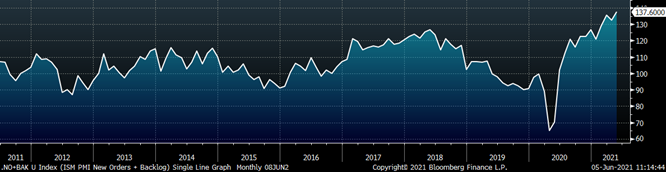

The chart below compares the ISM prices subindex with the ISM customer inventories subindex. The customer inventories and prices subindexes both printed lower with customer inventories at a record low and prices at their second highest level, surpassed only by last month’s print. The prices subindex has printed above 80 since February, if this were impacting demand, we would look for a contraction in new orders. The second chart shows the new orders plus backlog subindexes at record high levels, which represent demand for manufactured goods increasing despite these elevated prices. The final chart shows supplier deliveries surpassing the previous record high which occurred in March, this shows that supply chains continue to be under pressure representing an additional constraint that is pushing demand further out.

ISM Manufacturing PMI Customer Inventories Subindex (orange) & Prices Subindex (white)

ISM Manufacturing PMI New Orders plus Backlog Subindexes

ISM Manufacturing Prices Subindex

As an important reminder, year over year readings come from May 2020 when manufacturing demand was being suppressed by uncertainty and different local government restrictions.

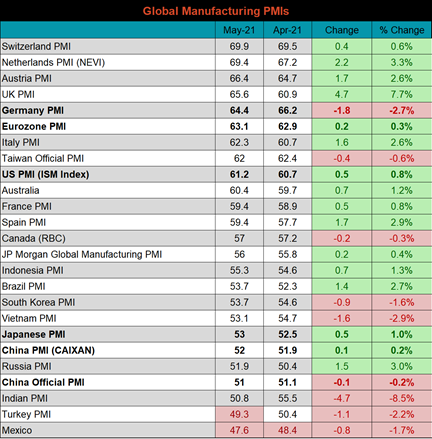

Global PMI

The May global PMI printings continue to show additional global strength with 16 of the 24 watched countries showing further expansion with only Mexico and Turkey, currently in contraction. The five most significant countries (bold) all continue to expand.

J.P. Morgan Global Manufacturing

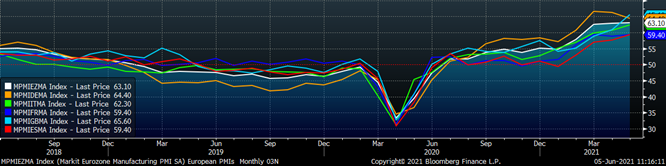

Eurozone (white), German (orange), Italian (green), Spanish (red), and French (blue), U.K. (teal) Manufacturing PMIs

US (white), Euro (blue), Chinese (red) and Japanese (green) Manufacturing PMIs

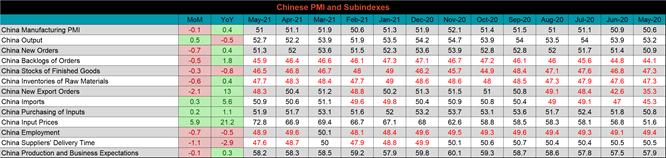

China’s official manufacturing PMI decreased slightly, while the Caixan PMI was slightly higher. Both remain in expansion territory.

China Official (white) and Caixan (red) Manufacturing PMIs

The table below breaks down China’s official manufacturing PMI subindexes. The input prices subindex was up the most significantly, 5.9 points compared to April and 21.2 points compared to May of last year. For an export heavy market, like the Chinese manufacturing industry, high input prices (inflation) could be a significant drag on growth.

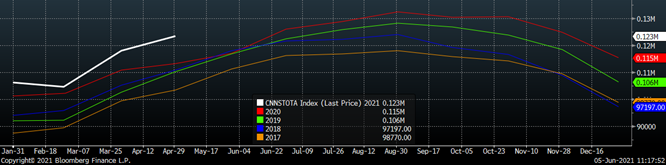

Construction Spending

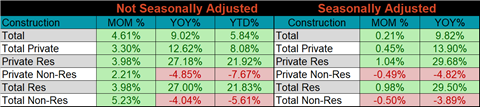

April seasonally adjusted U.S. construction spending was up slightly, 0.2% compared to March, and 9.8% higher than a year ago.

April U.S. Construction Spending

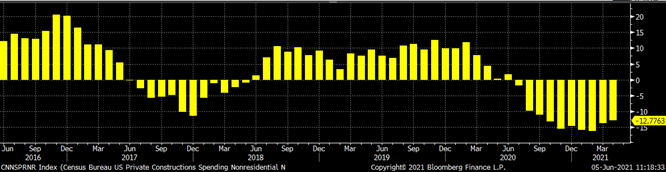

The white line in the chart below represents not seasonally adjusted construction spending in 2021 and compares it to the spending of the previous 4 years. Overall spending continues to expand and is higher than any point in the last 4 years. The last two charts show the YoY changes in construction spending. Private non-residential spending decreased further in April, for the tenth month in a row, albeit at an improving rate. Residential spending remains significantly elevated compared to last year’s levels, as demand for homes remains red hot.

U.S. Construction Spending

U.S. Private Nonresidential Construction Spending NSA YoY % Change

U.S. Residential Construction Spending NSA YoY % Change

Auto Sales

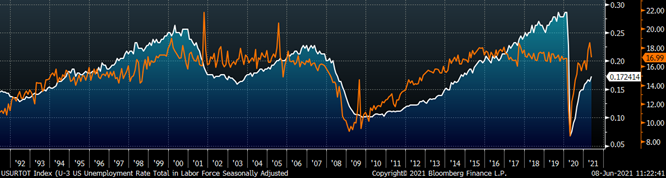

May U.S. light vehicle sales moved lower after last month’s recent high, to a 17m seasonally adjusted annualized rate (S.A.A.R) but remains well above the 10-year average. The second chart shows the relationship between the unemployment rate and auto sales. The unemployment rate is inverted to show that declining unemployment typically leads to increasing auto sales. The labor market recovered further, but has a long way to go, while demand for autos remains robust, only hampered by supply chain woes and the continued chip shortage.

May U.S. Auto Sales (S.A.A.R.)

May U.S. Auto Sales (orange) and the Inverted Unemployment Rate (white)

Risks

Below are the most pertinent upside and downside price risks:

Upside Risks:

- Higher share of discretionary income allocated to goods from steel intensive industries

- Strengthening global flat rolled and raw material prices

- Unplanned & extended planned outages

- Low current import levels

- Declining/low inventory levels at end users and service centers

- Broad increases in commodity prices due to a weakening US Dollar

- Limited spot transactions skewing market indexes to extreme levels

Downside Risks:

- Increased domestic production capacity

- Increasing price differentials and hedging opportunities leading to higher imports

- Steel consumers substitute to lower cost alternatives

- Steel buyers and consumers “double ordering” to more than cover steel needs

- Weak labor and construction markets

- Tightening credit markets, as elevated prices push total costs to credit caps

- Reduction and/or removal of domestic trade barriers

- Supply chain disruptions allowing producers to catch up on orders

HRC Futures

All of the below data points are as of June 4, 2021.

The Platts TSI Daily Midwest HRC Index increased by $20.25 to $1,636.25.

Platts TSI Daily Midwest HRC Index

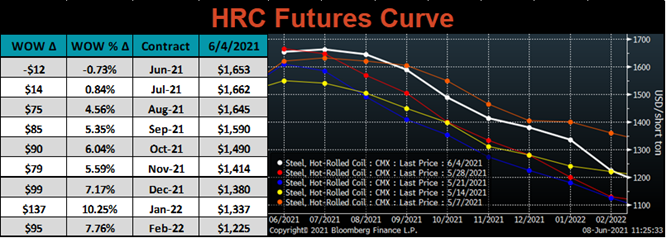

The CME Midwest HRC futures curve is below with last Friday’s settlements in white. Last week, the entire curve shifted higher, except for the June expiration. This move was most significant in 4Q21 and 1Q22, while July and August both reached all-time highs.

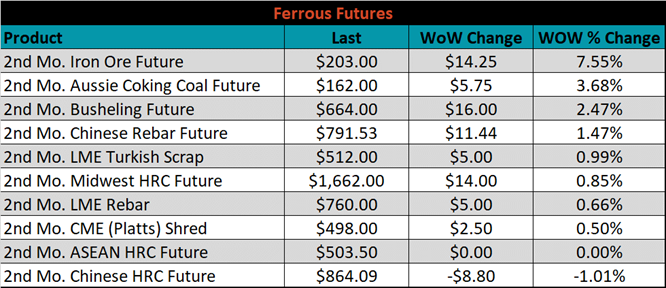

July ferrous futures were mixed. Iron ore gained 7.6%, while Chinese HRC was down 1%.

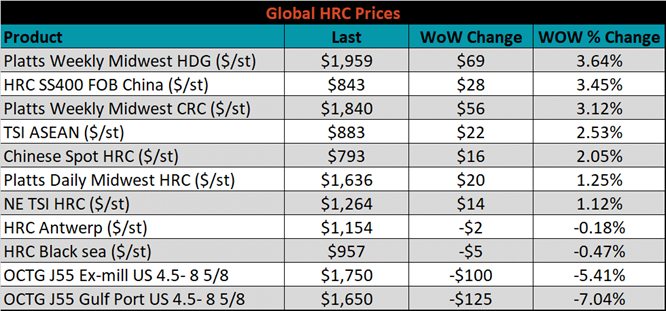

Global flat rolled indexes were mostly higher, led by TSI Platts Midwest HDG, up 3.6%.

The AISI Capacity Utilization rate increased 2.5% to 81.5%.

AISI Steel Capacity Utilization Rate (orange) and TSI Daily HRC Price (white)

Imports & Differentials

May flat rolled import license data is forecasting an increase of 124k to 890k MoM.

All Sheet Imports (white) w/ 3-Mo. (green) & 12-Mo. Moving Average (red)

Tube imports license data is forecasting an increase of 11k to 331k in May.

All Tube Imports (white) w/ 3-Mo. (green) & 12-Mo. Moving Average (red)

All Sheet plus Tube (white) w/ 3-Mo. (green) & 12-Mo. Moving Average (red)

May AZ/AL import license data is forecasting an increase of 5k to 90k.

Galvalume Imports (white) w/ 3 Mo. (green) & 12 Mo. Moving Average (red)

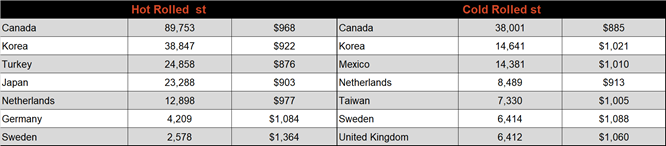

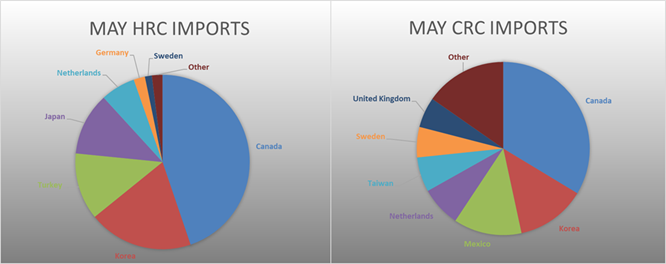

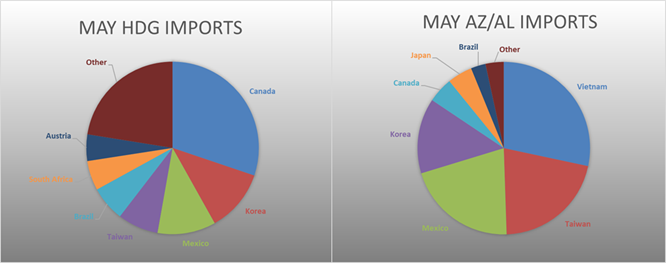

Below is May import license data through May 31, 2021.

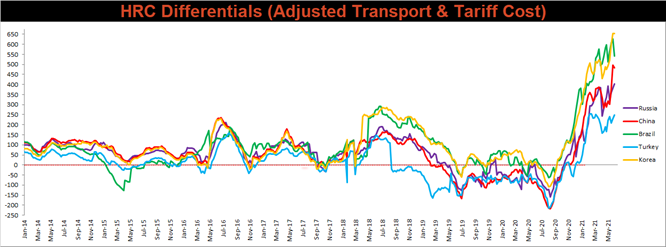

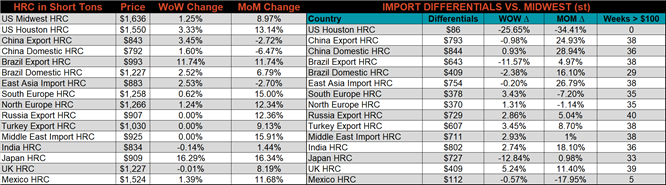

Below is the Midwest HRC price vs. each listed country’s export price using pricing from SBB Platts. We have adjusted each export price to include any tariff or transportation cost to get a comparable delivered price. The differentials decreased for China, Brazil, and Korea, but increased for Turkey and Russia.

SBB Platt’s HRC, CRC and HDG pricing is below. The Midwest HDG, CRC & HRC prices were up, 3.6%, 3.1% and 1.3%, respectively. Globally, the Japanese domestic HRC price was up 16.3%.

Raw Materials

Raw material prices were mixed, with the IODEX up 10%, while pig iron was down 0.8%.

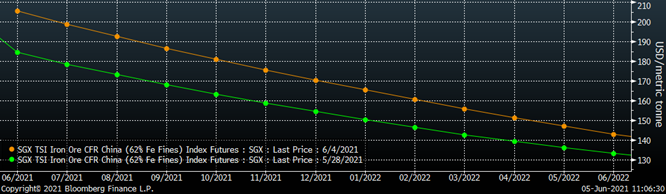

Below is the iron ore future curve with Friday’s settlements in orange, and the prior week’s settlements in green. Last week, the entire curve shifted higher, most significantly in the front.

SGX Iron Ore Futures Curve

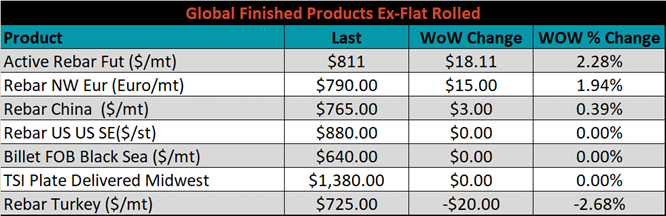

The ex-flat rolled prices are listed below.

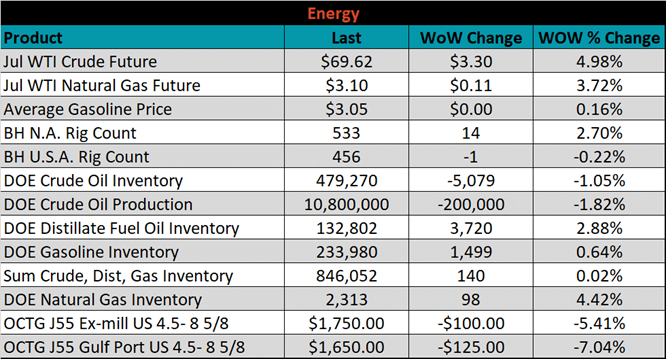

Energy

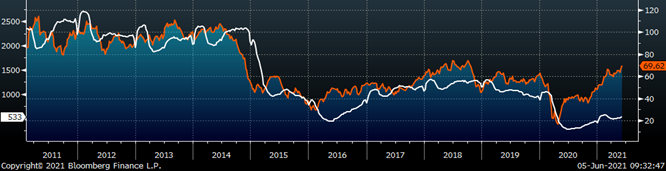

Last week, the July WTI crude oil future was up another $3.30 or 5% to $69.62/bbl. The aggregate inventory level was up 0.2%, while crude oil production was down to 10.8m bbl/day. The Baker Hughes North American rig count was up 14 rigs, and the U.S. rig count was up 1 rig.

July WTI Crude Oil Futures (orange) vs. Aggregate Energy Inventory (white)

Front Month WTI Crude Oil Future (orange) and Baker Hughes N.A. Rig Count (white)

The list below details some upside and downside risks relevant to the steel industry. The orange ones are occurring or look to be highly likely. The upside risks look to be in control.

Upside Risks:

- Higher share of discretionary income allocated to goods from steel intensive industries

- Changes in China’s policies regarding ferrous markets, including production cuts and imports

- Strengthening global flat rolled and raw material prices

- Unplanned & extended planned outages, including operational issues leaving mills behind

- Declining/low inventory levels at end users and service centers

- Broad increases in commodity prices due to a weakening US Dollar

- Limited spot transactions skewing market indexes to extreme levels

- Chinese economic stimulus measures

- Fiscal policy measures including a new stimulus and/or infrastructure package

- Low interest rates

- China strict steel capacity cuts

- Energy industry rebound

- Unexpected inflation

- Further section 232 tariffs and quotas restricting supply

Downside Risks:

- Increased domestic production capacity

- Increasing price differentials and hedging opportunities leading to higher imports

- Steel consumers substitute to lower cost alternatives

- Steel buyers and consumers “double ordering” to more than cover steel needs

- Weak labor and construction markets

- Tightening credit markets, as elevated prices push total costs to credit caps

- Reduction and/or removal of domestic trade barriers

- Supply chain disruptions allowing producers to catch up on orders

- Political & geopolitical uncertainty

- Weak global economics/PMIs

- Trade slowdown in China due to tensions with US, Hong Kong, and others

- Domestic automotive industry under pressure

- Chinese restrictions in property market

- The Chinese Financial Crisis

- Unexpected sharp China RMB devaluation