Flack Capital Markets | Ferrous Financial Insider

August 9, 2024 – Issue #444

August 9, 2024 – Issue #444

Overview:

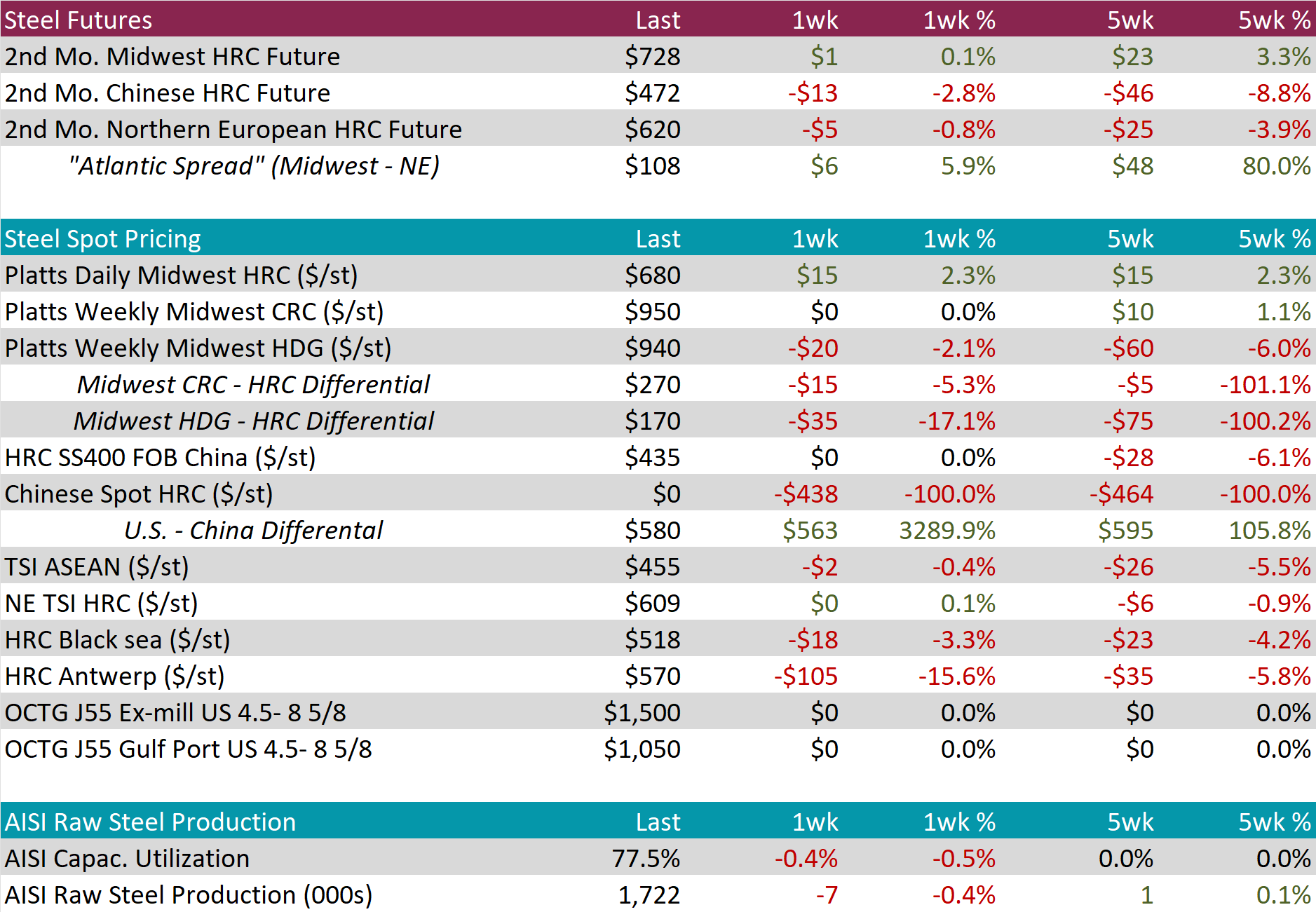

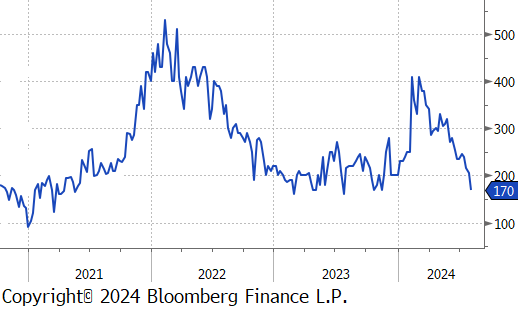

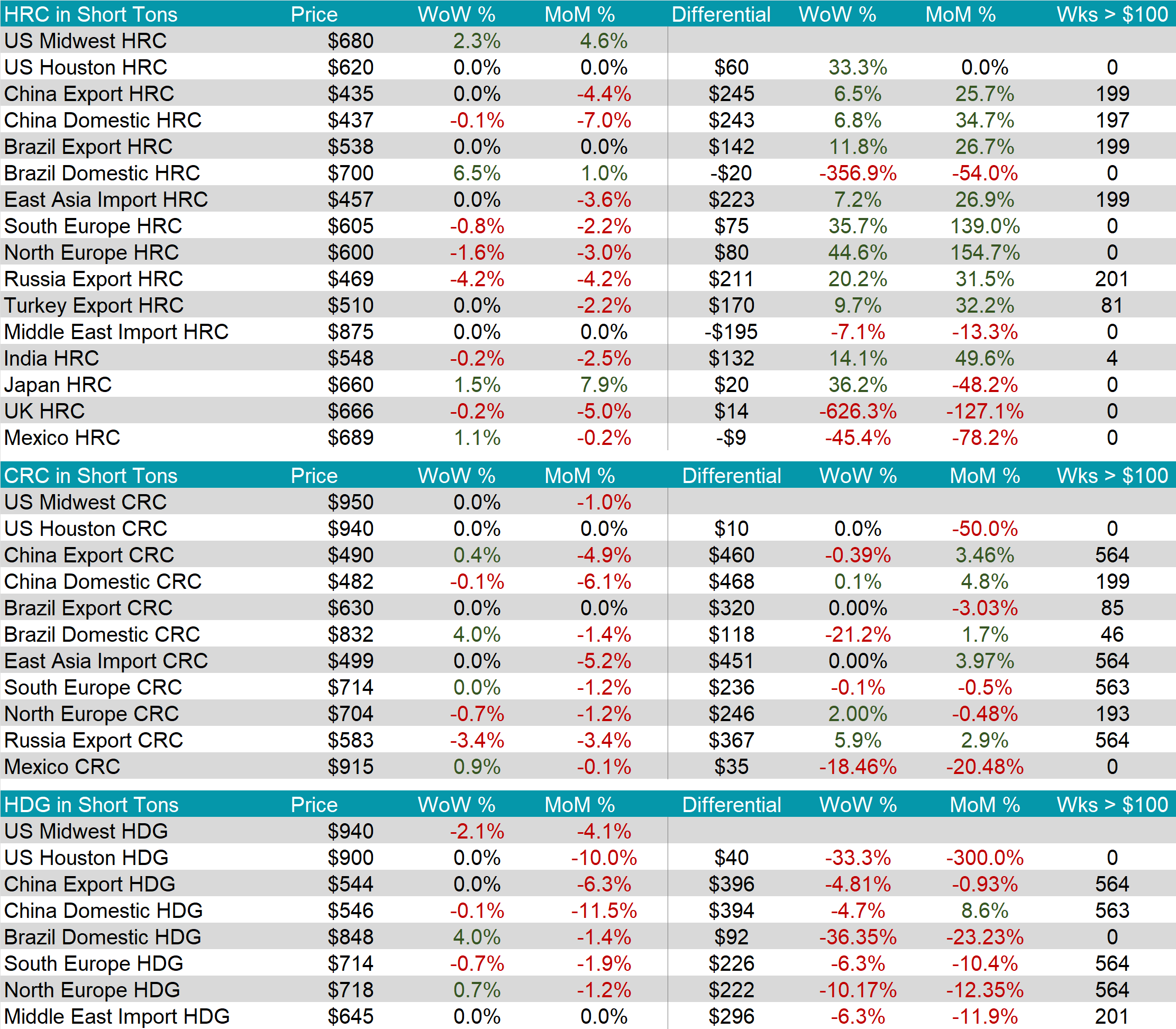

The HRC spot price increased further, rising by $15 or 2.3% to $680, reaching the highest price in seven weeks. At the same time, the HRC 2nd month future inched up by $1 or 0.1% to $728, marking the third consecutive week of price increases.

Tandem products were mixed, with CRC remaining unchanged while HDG fell by $20 or -2.1% to $940, resulting in the HDG – HRC differential to decline by $35 or -17.1% to $170. hitting the lowest spread of this year.

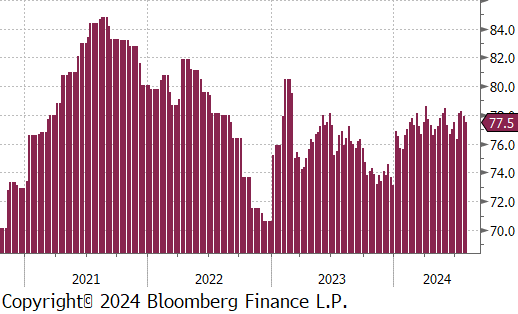

Mill production scaled back further, with capacity utilization ticking down by 0.4% to 77.5%, bringing raw steel production down to 1.722m net tons.

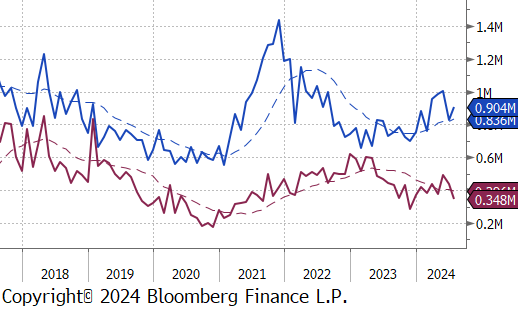

July Projection – Sheet 904k (up 79k MoM); Tube 348k (down 65k MoM)

June Census – Sheet 825k (down 179k MoM); tube 414k (down 80k MoM)

All watched global differentials expanded further, with Brazil Domestic HRC having the largest increase of 6.5% and Russia Export HRC having the largest decrease of -4.2%.

Scrap

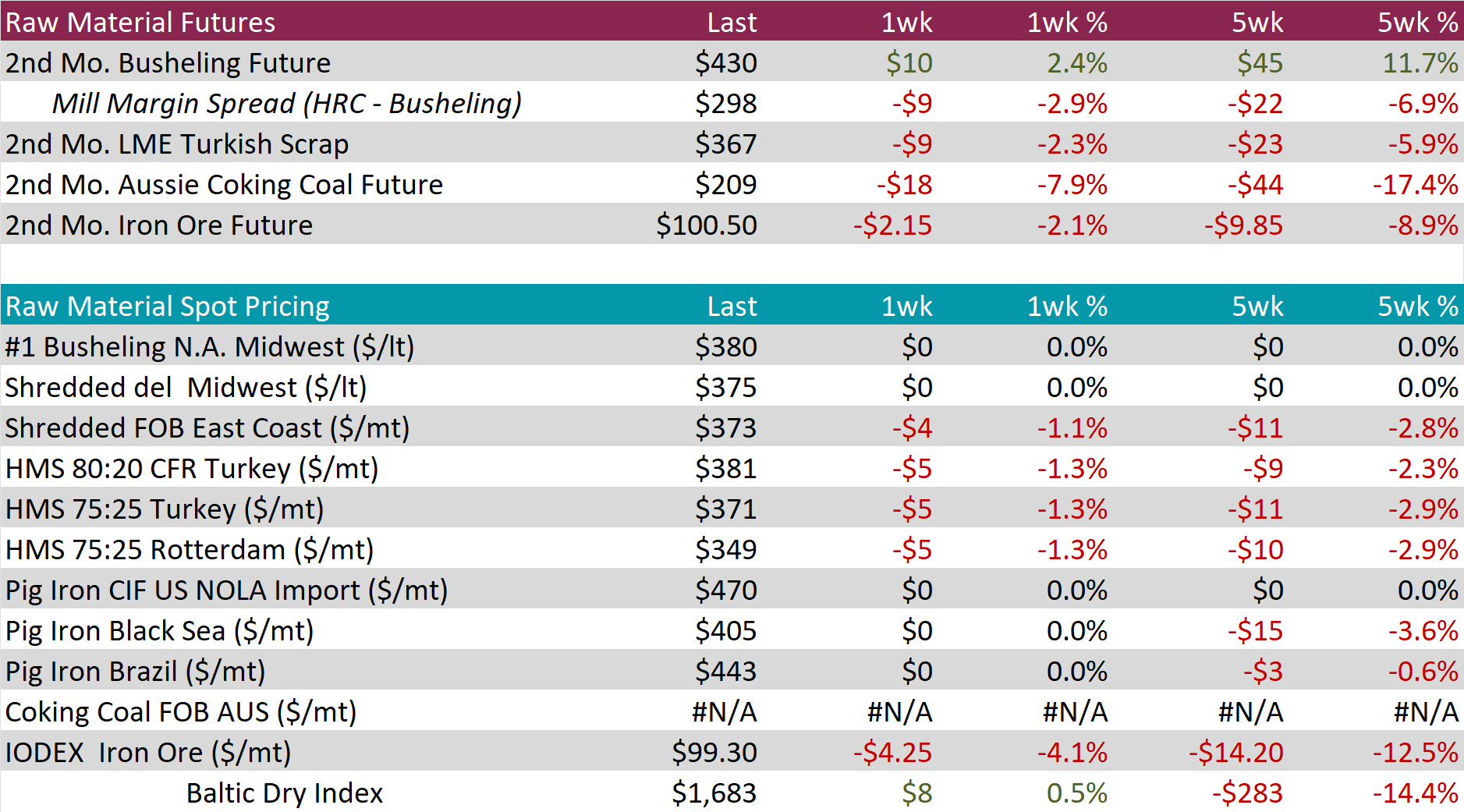

The 2nd month busheling future jumped up by $10 or 2.4% to $430, resulting in the five-week price change to be up by $45 or 11.7%.

The Aussie coking coal 2nd month future dropped by $18 or -7.9% to $209, reaching the lowest price since July 2022.

The iron ore 2nd month future slipped by $2.15 or -2.1% to $100.50, falling to the lowest price since April.

Dry Bulk / Freight

The Baltic Dry Index climbed by $8 or 0.5% to $1,683, rebounding slightly from last weeks notable price drop.

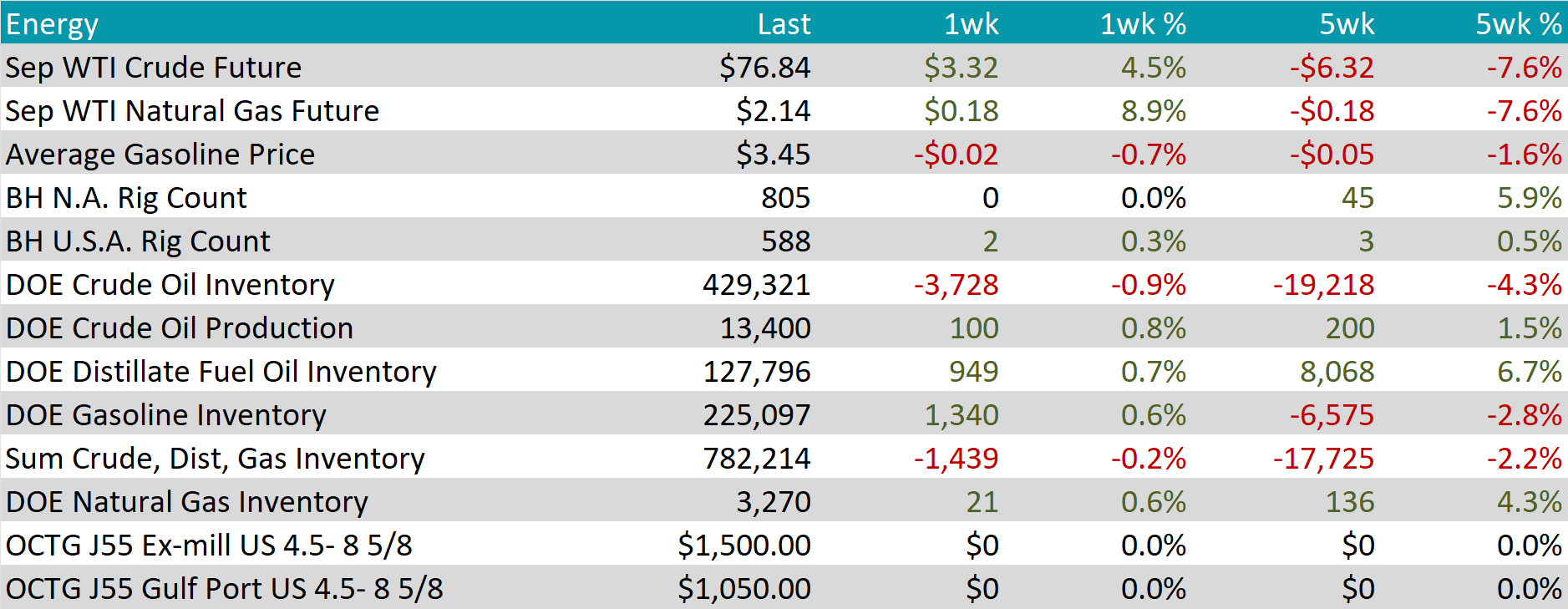

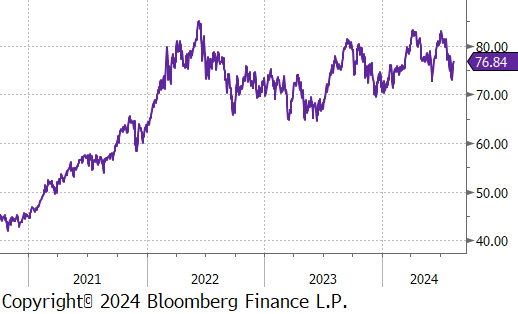

WTI crude oil future gained $3.32 or 4.5% to $76.84/bbl.

WTI natural gas future gained $0.18 or 8.9% to $2.14/bbl.

The aggregate inventory level shrank further, declining by -0.2%, marking the third consecutive week of decreases.

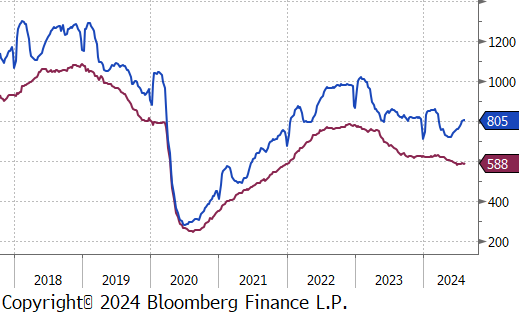

The Baker Hughes North American rig count held steady at 805 rigs, while the US rig count gained 2 rigs, bringing the total count to 588 rigs.

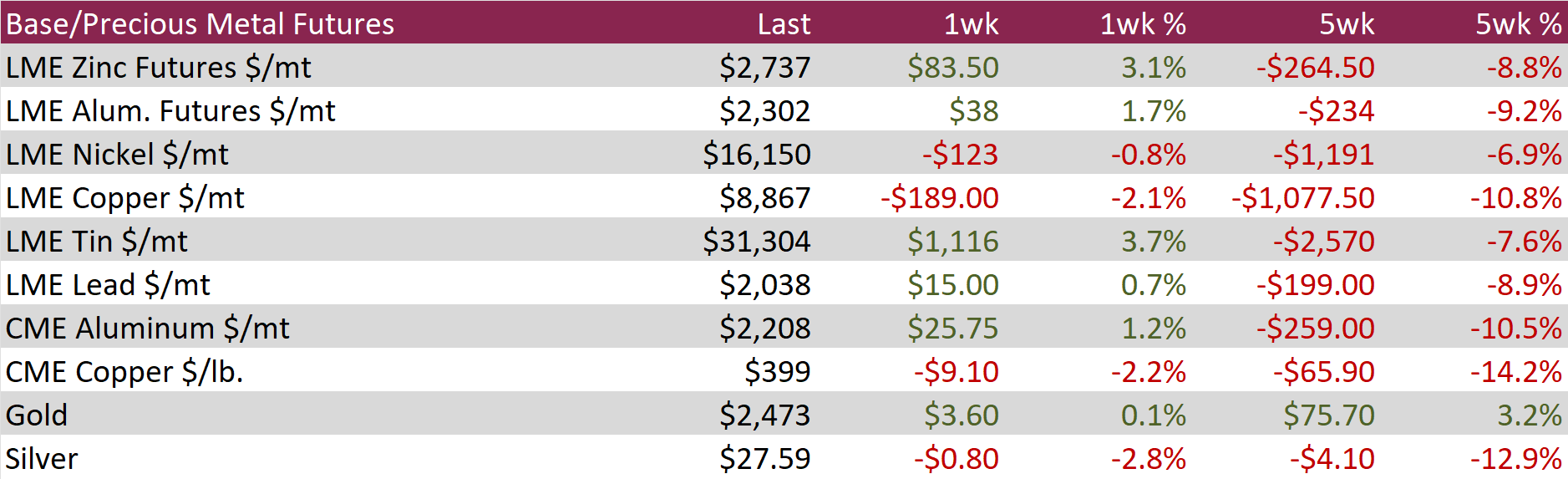

Aluminum futures grew by $38 or 1.7% to $2,302, rebounding slightly from a near five-month low as concerns over weak demand and abundant supply continue. Increased rainfall in Yunnan, a key production hub in China, improved hydropower availability, allowing smelters to restart idled capacity. This alleviated earlier concerns about dry weather disrupting production and led to a 6.2% annual increase in China’s primary aluminum output in June, reaching 3.76 million tonnes, the highest since November 2014. However, economic data indicated that domestic demand for factory goods in China remained subdued. The NBS manufacturing PMI showed its third consecutive contraction in July, while the broader Caixin gauge also unexpectedly contracted, suggesting that Chinese factories are struggling to find foreign clients to compensate for weak domestic demand.

Copper futures fell by $9.10 or -2.2% to $399, as markets weighed supply threats against ongoing weak demand. Zambia’s decision to close its border with the Democratic Republic of Congo, the world’s second-largest copper producer, disrupted copper shipments due to escalating trade disputes. Despite this, muted demand from China continued to exert downward pressure on copper prices. Demand for base metals in China is expected to remain weak, as the government refrained from implementing significant stimulus measures during its recent Third Plenum. Additionally, reports that some Chinese smelters are pursuing new projects to meet output mandates, despite earlier plans for joint production cuts to raise treatment charges, have eased supply concerns and added to the bearish sentiment.

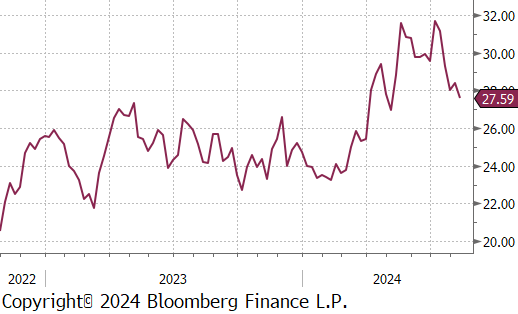

Silver declined by $0.80 or -2.8% to $27.59 as investors turned their attention to the upcoming US inflation data, seeking clues about the Fed’s next move on monetary policy. While expectations for a Fed rate cut in September are still strong, some Fed officials indicated last week that inflation might be easing enough to justify a rate cut as soon as next month. However, the positive jobs report released last week has created some division among market participants regarding the size of the anticipated rate cut, as it alleviated fears of a recession triggered by a weakening labor market. The market will closely watch producer inflation data, set to be released on Tuesday, followed by consumer inflation figures on Wednesday.

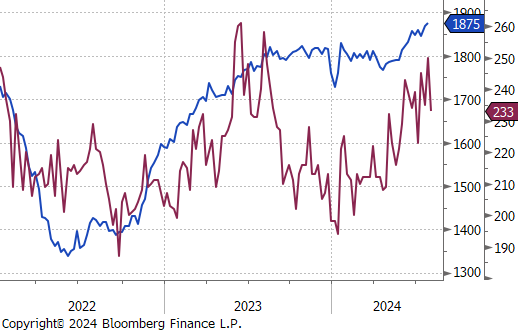

Initial Jobless Claims dropped by 17k to 233k versus the market expected 240k, marking the largest decline in nearly a year. This follows the previous week’s upwardly revised figure of 250k, which had been the highest in a year, easing some concerns about the labor market cooling too rapidly. Meanwhile, Continuing Jobless Claims increased by 6k to 1875k, the highest since November 2021.

The S&P Global US Composite PMI was revised down to 54.3 in July from a preliminary estimate of 55, showing a slight decrease from June’s 54.8. Despite the revision, the reading still indicates solid monthly expansion in private sector business activity, primarily driven by the service sector. The S&P Global US Services PMI was revised lower to 55 from a preliminary 56, compared to 55.3 in June. Although the rate of growth in the services sector eased slightly, the reading continues to point to robust expansion, with new business rising for the third consecutive month at a solid pace.