Flack Capital Markets | Ferrous Financial Insider

January 24, 2025 – Issue #468

January 24, 2025 – Issue #468

Overview:

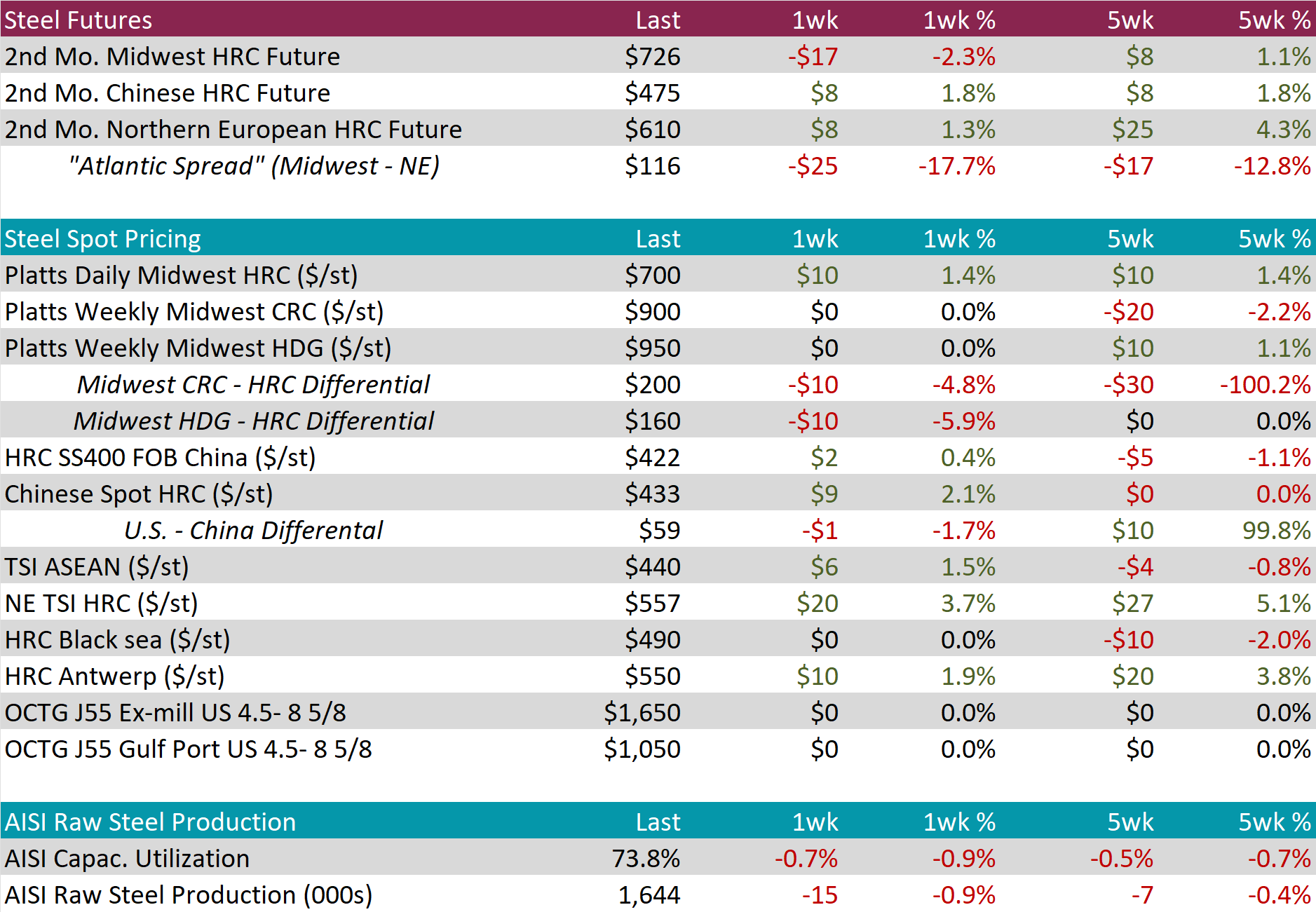

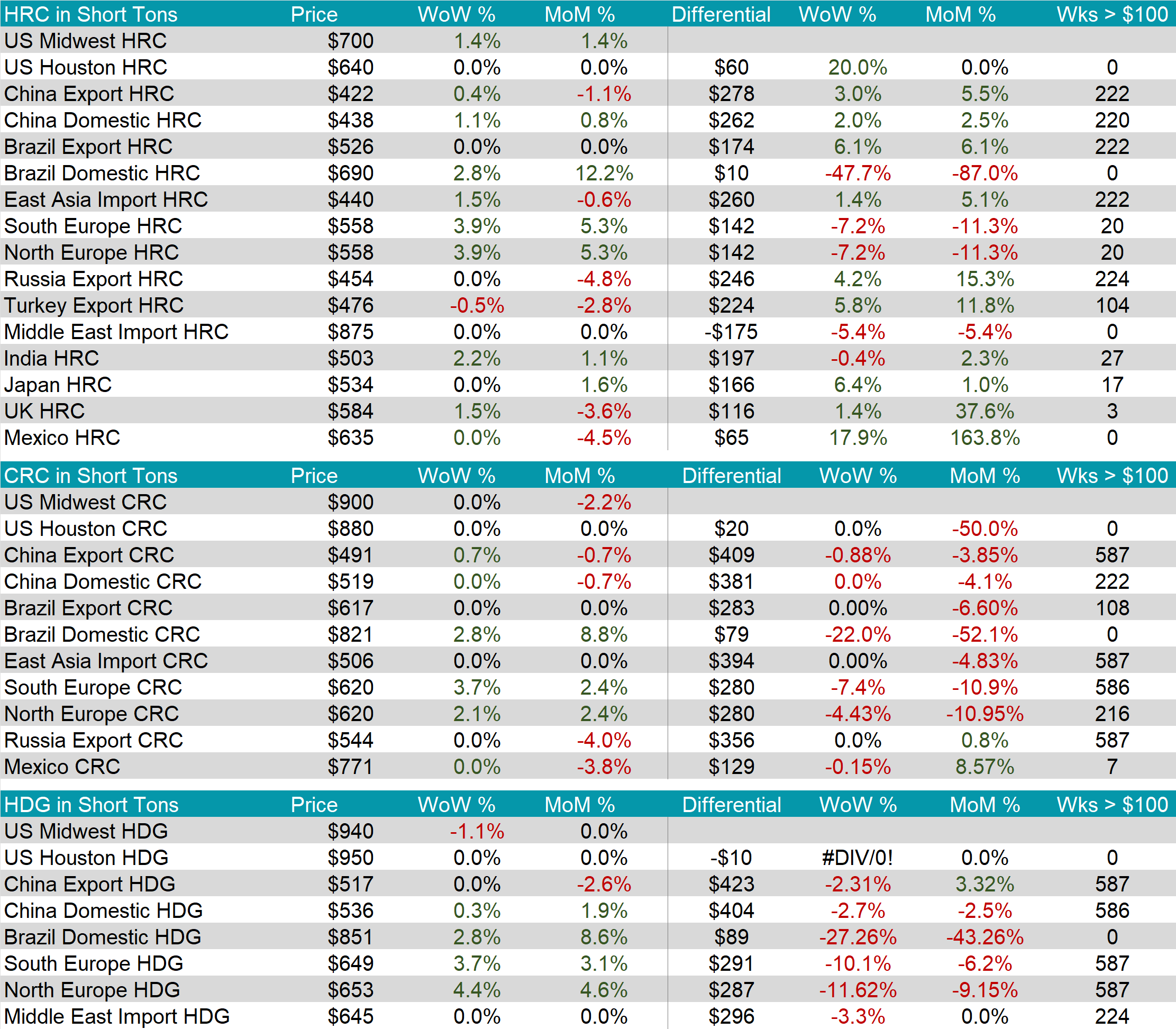

The HRC spot price rebounded by $10 or 1.4% to $700. At the same time, the HRC 2nd month future declined by $17 or -2.3% to $726, falling to the lowest level in 5 weeks.

Tandem products continued to remain unchanged, resulting in the HDG – HRC differential to slip by $10 or -5.9% to $160.

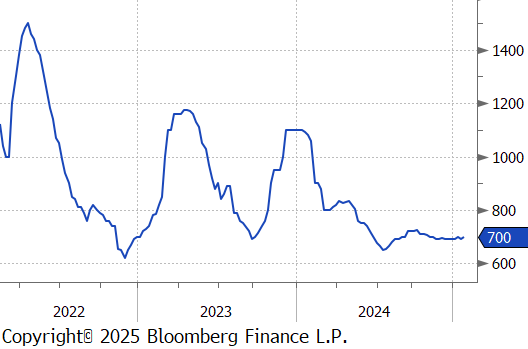

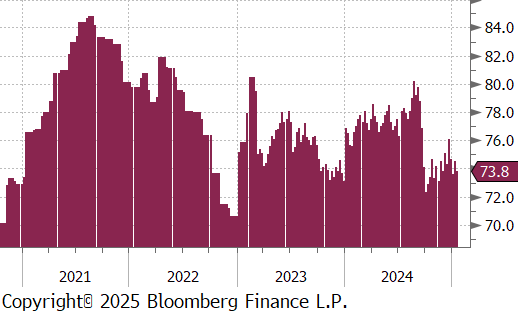

Mill production eased once again, with capacity utilization ticking down by -0.7% to 73.8%, bringing raw steel production down to 1.644m net tons.

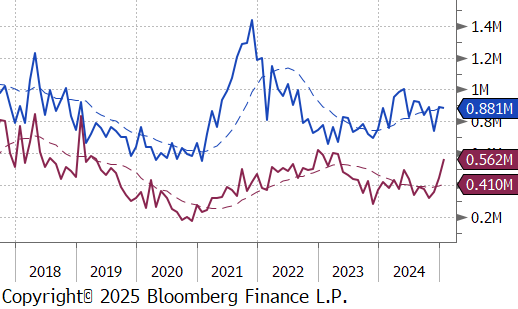

January Projection – Sheet 881k (down 7k MoM); Tube 562k (up 115k MoM)

December Projection – Sheet 888k (up 145k MoM); Tube 447k (up 87k MoM)

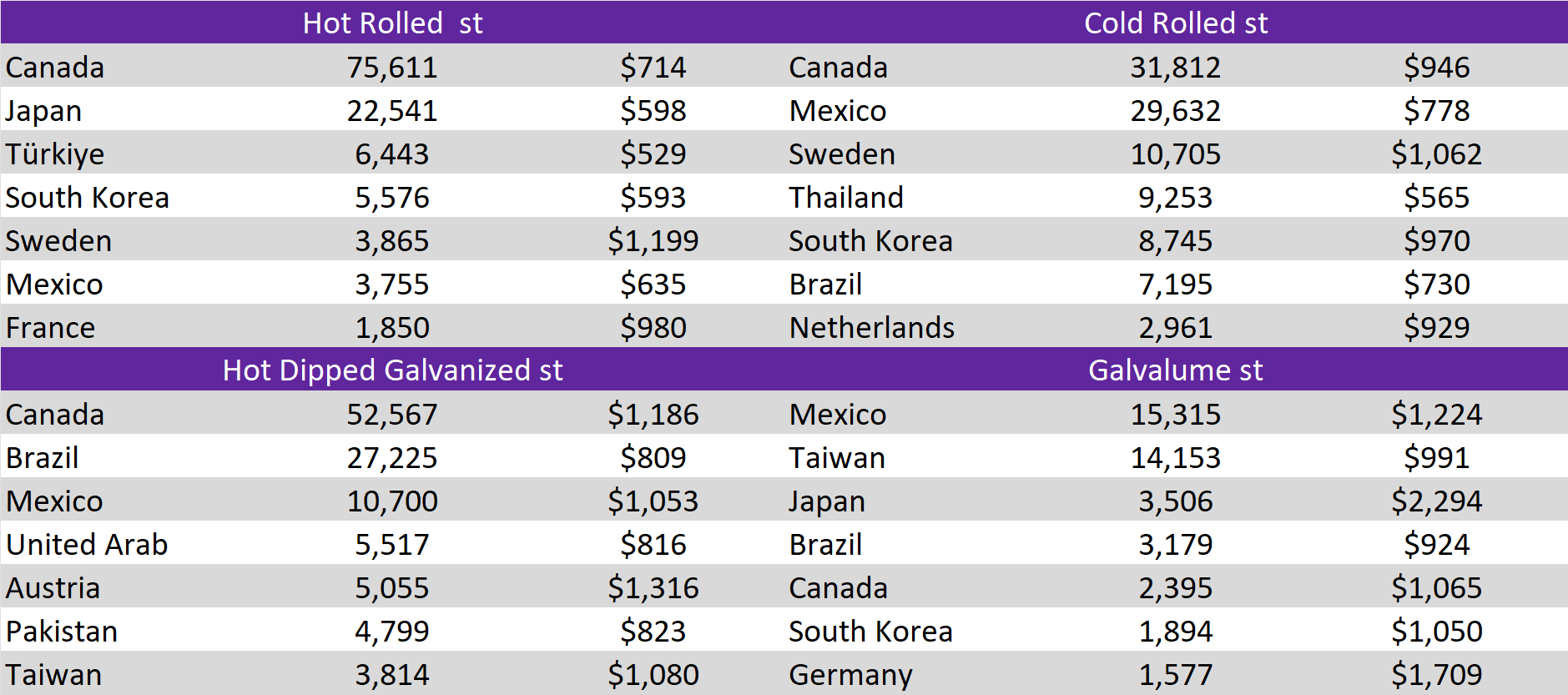

The watched global differentials were mixed this week, as the China Export HRC grew slightly by 0.4%, the Korea HRC price rose by 1.5%, N Europe HRC up by 3.9%, while the Turkey Export HRC slipped by -0.5%.

Scrap

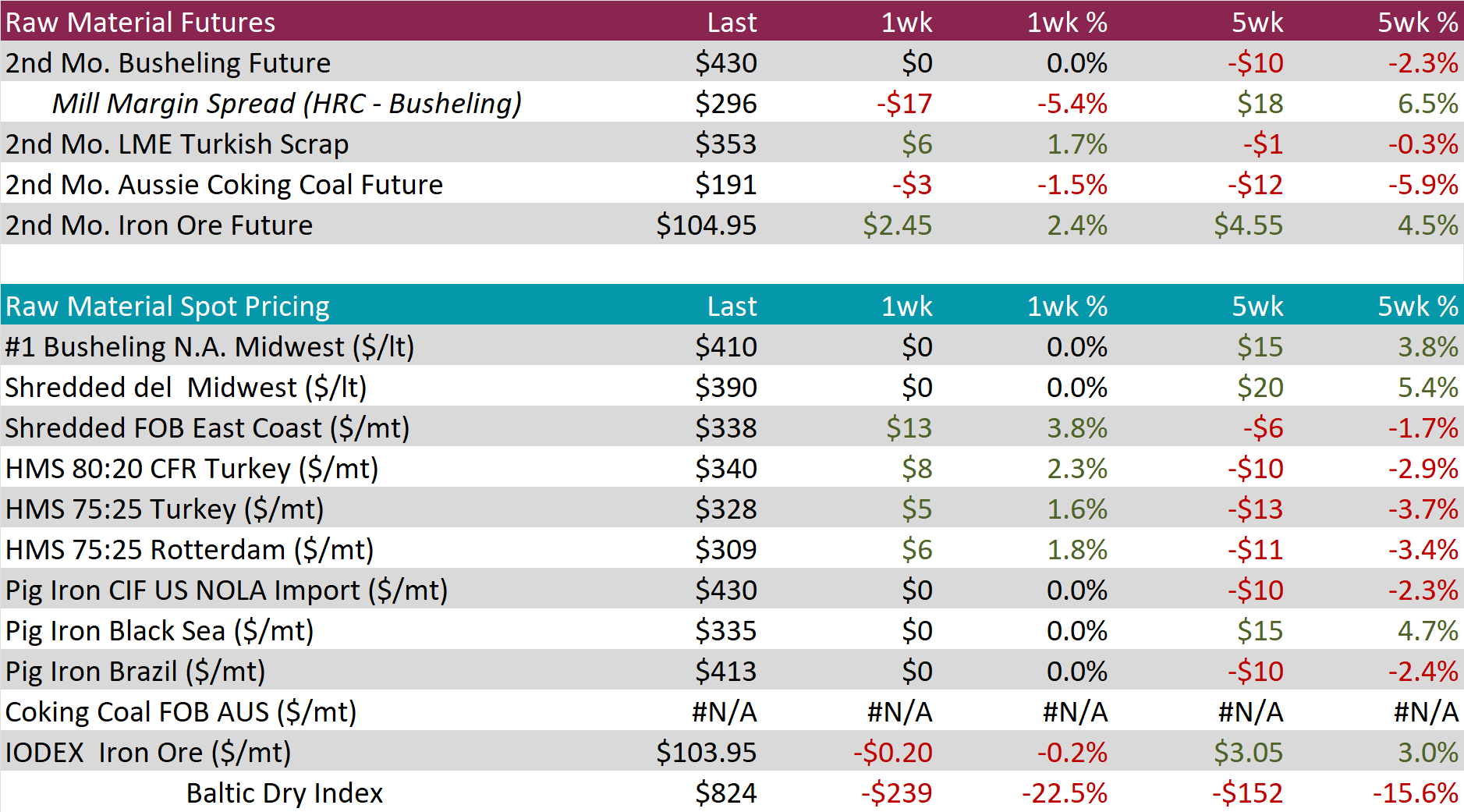

The busheling 2nd month future held steady at $430, resulting in the five-week price change to be down by $10 or -2.3%.

The LME Turkish scrap 2nd month future rose by $6 or 1.7% to $353, marking the second consecutive week of increases and the highest price in five weeks.

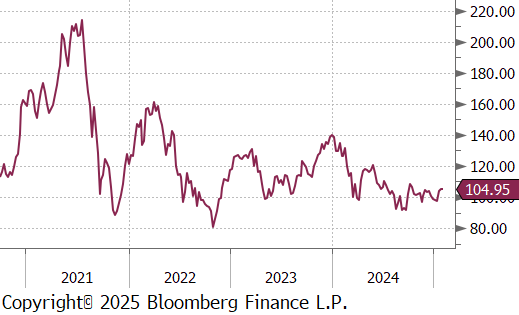

The iron ore 2nd month future inched up by $2.45 or 2.4% to $104.95, increasing for the second consecutive week, reaching the highest in 11 weeks.

Dry Bulk / Freight

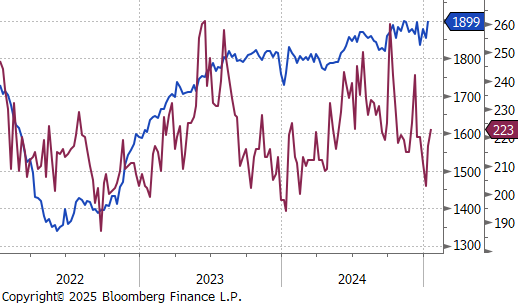

The Baltic Dry Index dropped by $239 or -22.5% to $824, falling to the lowest level since February 2023.

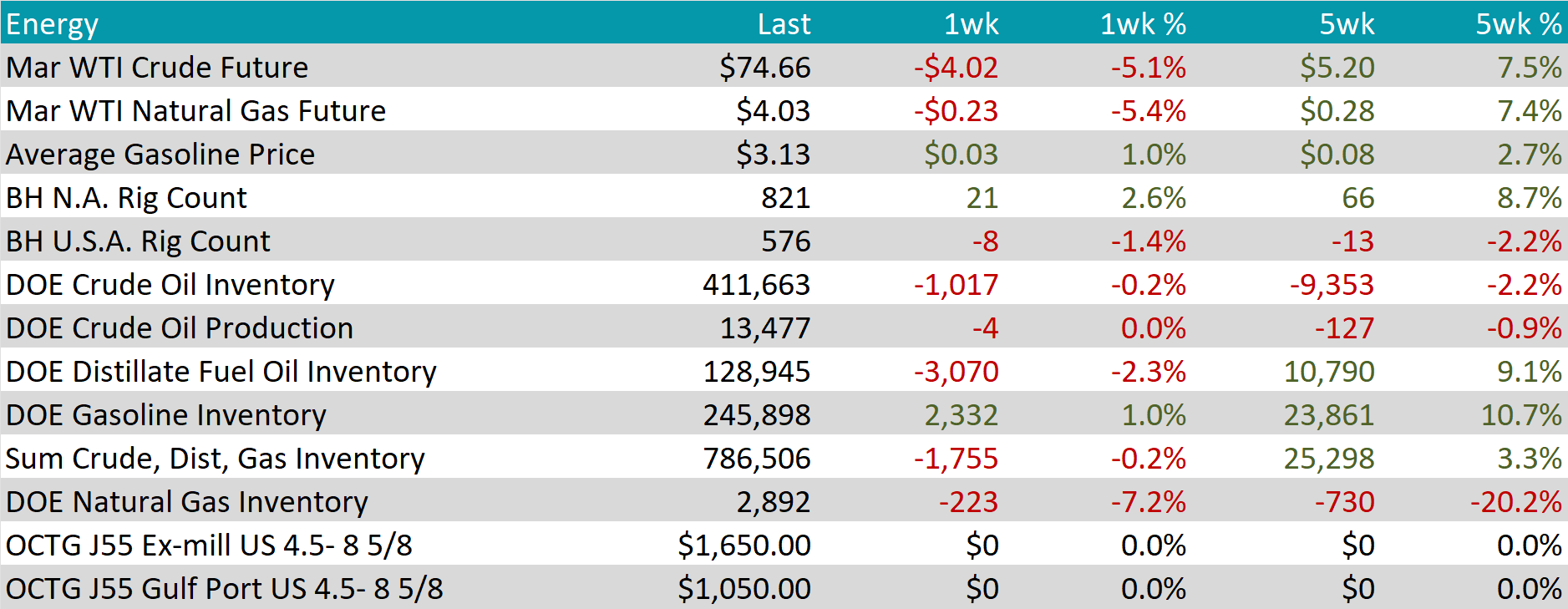

WTI crude oil future lost $4.02 or -5.1% to $74.66/bbl.

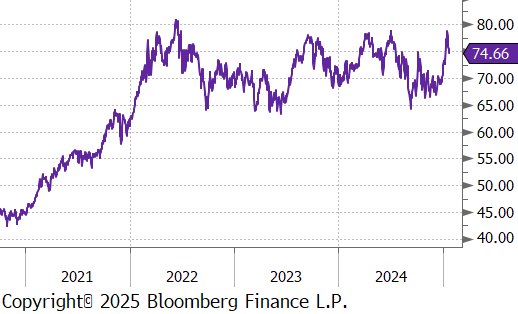

WTI natural gas future lost $0.23 or -5.4% to $4.03/bbl.

The aggregate inventory level eased, declining by -0.2%.

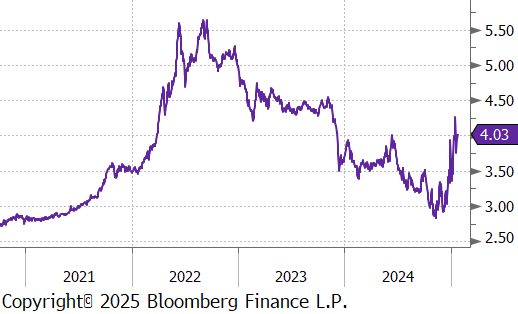

The Baker Hughes North American rig count jumped by 21, bringing the total count to 821 rigs. At the same time, the US rig count reduced by 8, bringing the total count down to 576 rigs.

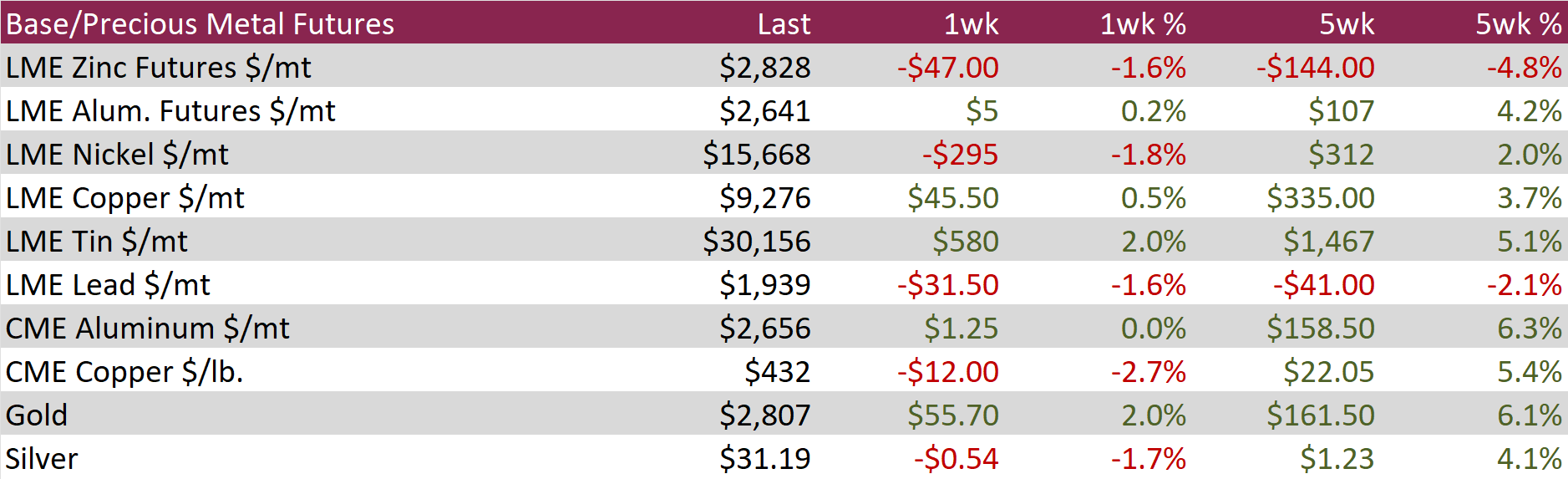

Aluminum future rose by $5 or 0.2% to $2,641, as President Trump’s comments signal potential tariffs against China. The prospect of heightened trade tensions pressured the outlook for foreign demand. Aluminum futures remained nearly 5% above this year’s near four-month low, underpinned by concerns over tighter supply. The European Union is set to sanction imports of primary aluminum from Russia in its next package, reinforcing the ongoing phase-out of Russian metals after its 2022 invasion of Ukraine. Meanwhile, China produced a record 44 million tons of aluminum in 2024, approaching the government-imposed cap of 45 million tons established in 2017 to prevent oversupply and support carbon emissions targets. This production ceiling is expected to slow output growth, balancing global supply dynamics.

Copper futures fell by $12 or -2.7% to $432 as market sentiment weakened amid geopolitical tensions and softer economic data. President Trump’s threat of tariffs and sanctions against Colombia, following its decision to block U.S. military aircraft carrying deported migrants, added to global trade uncertainties. Disappointing data from China, the world’s largest copper consumer, further pressured prices. Manufacturing activity unexpectedly contracted, and growth in the services sector slowed significantly, raising concerns about demand. Additionally, caution ahead of China’s week-long Lunar New Year holiday contributed to subdued trading volumes. On the supply side, Freeport-McMoRan reported it missed fourth-quarter production targets and warned of a sharp decline in first-quarter output, signaling potential supply challenges.

Precious Metals

Gold jumped by $55.70 or 2.0% to $2,807, staying close to record levels. Market confidence remains strong that the Federal Reserve will cut interest rates further this year. While the Fed is expected to hold rates steady this week following 100 basis points of cuts since September, investors are optimistic that Chair Jerome Powell will adopt a cautious tone, especially after recent CPI data showed signs of softening inflation. Pro-inflationary risks from U.S. trade policies have eased, with President Trump dialing back rhetoric on tariffs against China and reaching an expatriation agreement with Colombia to avert tariff threats. Markets currently anticipate two Fed rate cuts this year, with a slight consensus for the first move in May, bolstering the appeal of non-yielding assets like gold.

Manufacturing data for January continued its recent encouraging trend although the Kansas City Fed Manufacturing Survey printing down to -5, below the expectation of an increase to 0. From a broader perspective, the preliminary January S&P Global Manufacturing PMI beat expectations and printed at 50.1, the first expansionary print in 6 months.

The housing sector showed growth as well, with December existing home sales increasing to 4.24M, above the expected increase to 4.2M, even amid the current elevated National Average 30yr Fixed Mortgage Rate hovering above 7% for most of the month.

Finally, the final January University of Michigan Consumer Sentiment survey came in well below the expectation of a 73.2 print, declining to 71.1, and showing the first “lower” print in 6 months. This was driven by consumer deteriorating view on both current conditions and expectations. Additionally, the 1-yr inflation expectation rose to 3.3%. All that said, the significant volatility in expectations by political affiliation suggests that we should wait a few months before jumping to any conclusions.