Flack Capital Markets | Ferrous Financial Insider

November 8, 2024 – Issue #457

November 8, 2024 – Issue #457

Overview:

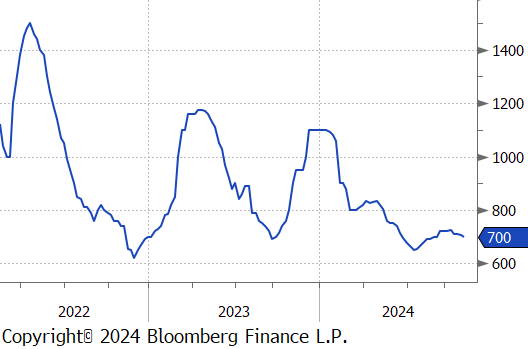

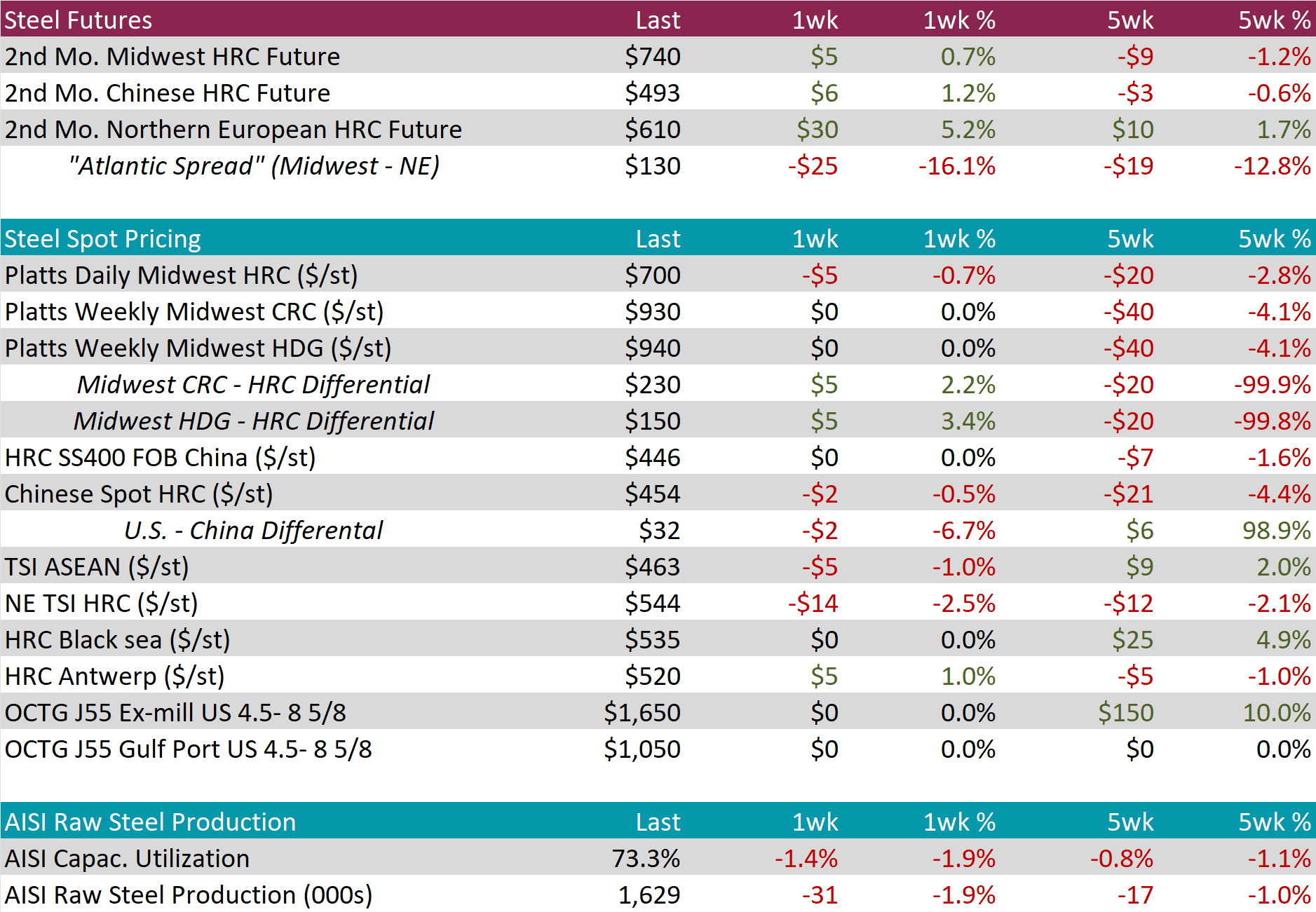

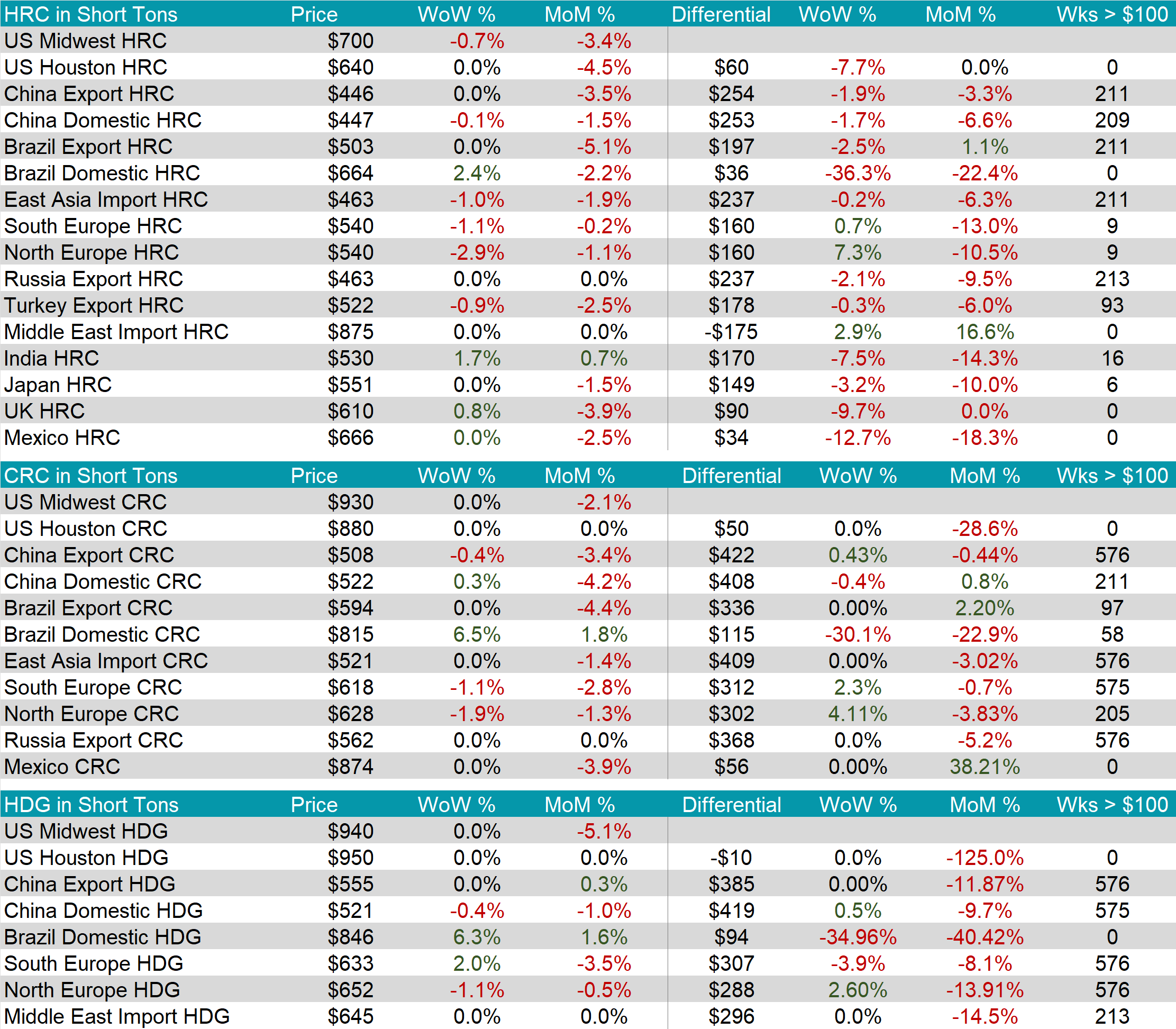

The HRC spot price fell by $ 5 or -0.7% to $700, furthering the recent downward trend and hitting the lowest level since late August. At the same time, the HRC 2nd month future rose by $5 or 0.7% to $740, building upon last weeks gain.

Tandem products both remained unchanged, resulting in the HDG – HRC differential to increase by $5 or 3.4% to $150, coming off of last weeks recent low.

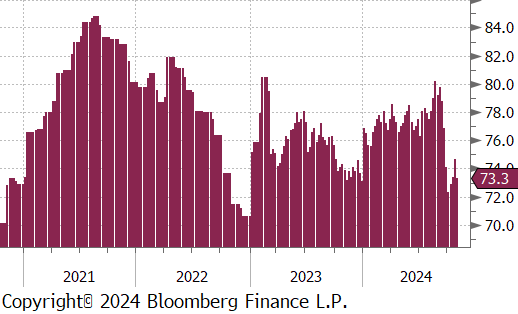

Mill production remains somewhat subdued, with capacity utilization ticking down by -1.4% to 73.7%, bringing raw steel production down to 1.629m net tons.

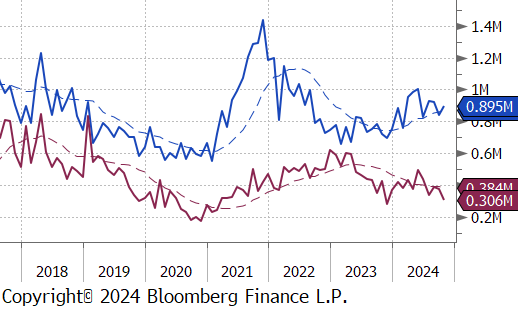

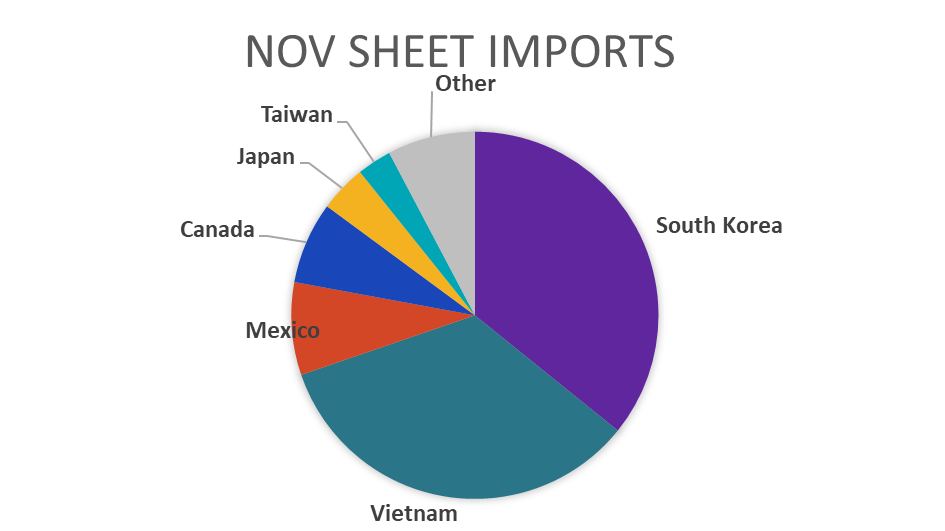

October Projection – Sheet 895k (up 54k MoM); Tube 306k (down 67k MoM)

September Census – Sheet 841k (down 78k MoM); Tube 373k (down 15k MoM)

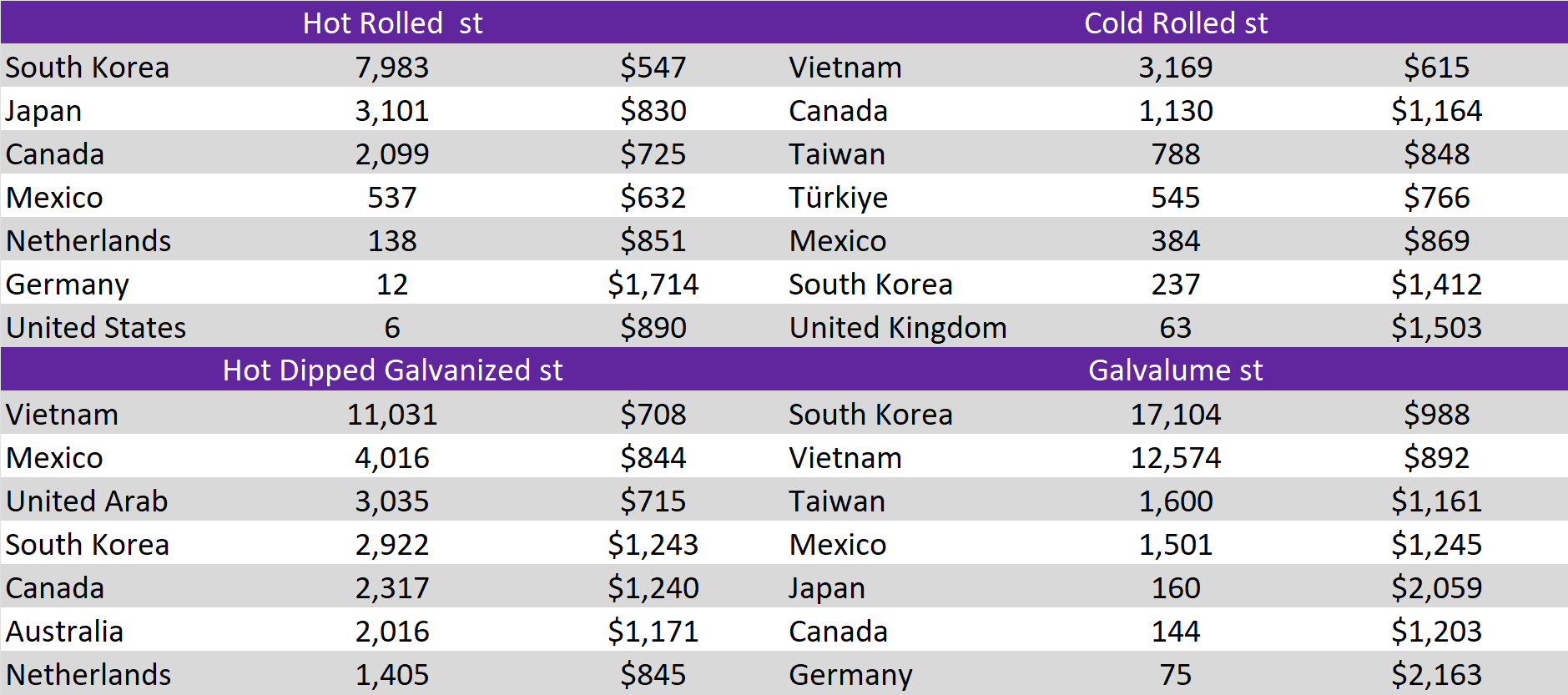

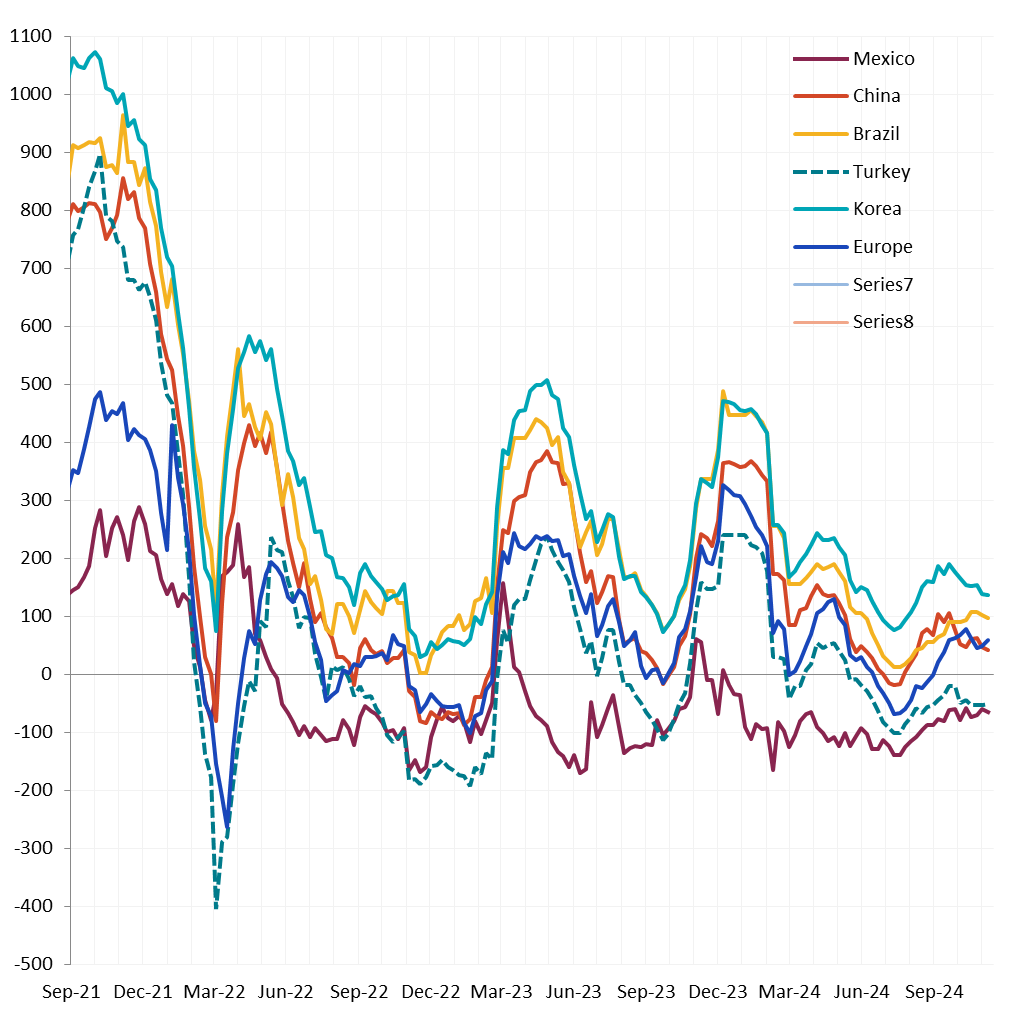

Watched global differentials mainly contracted except to Europe, as North Europe HRC fell by -2.9%, and Turkey Export HRC declined -0.9%.

Scrap

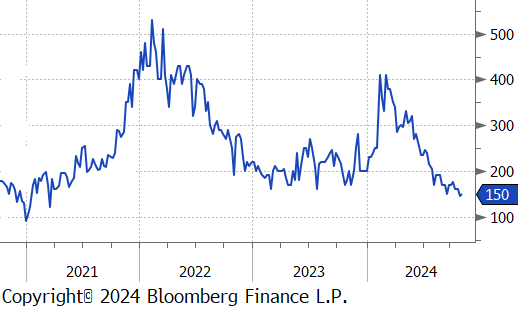

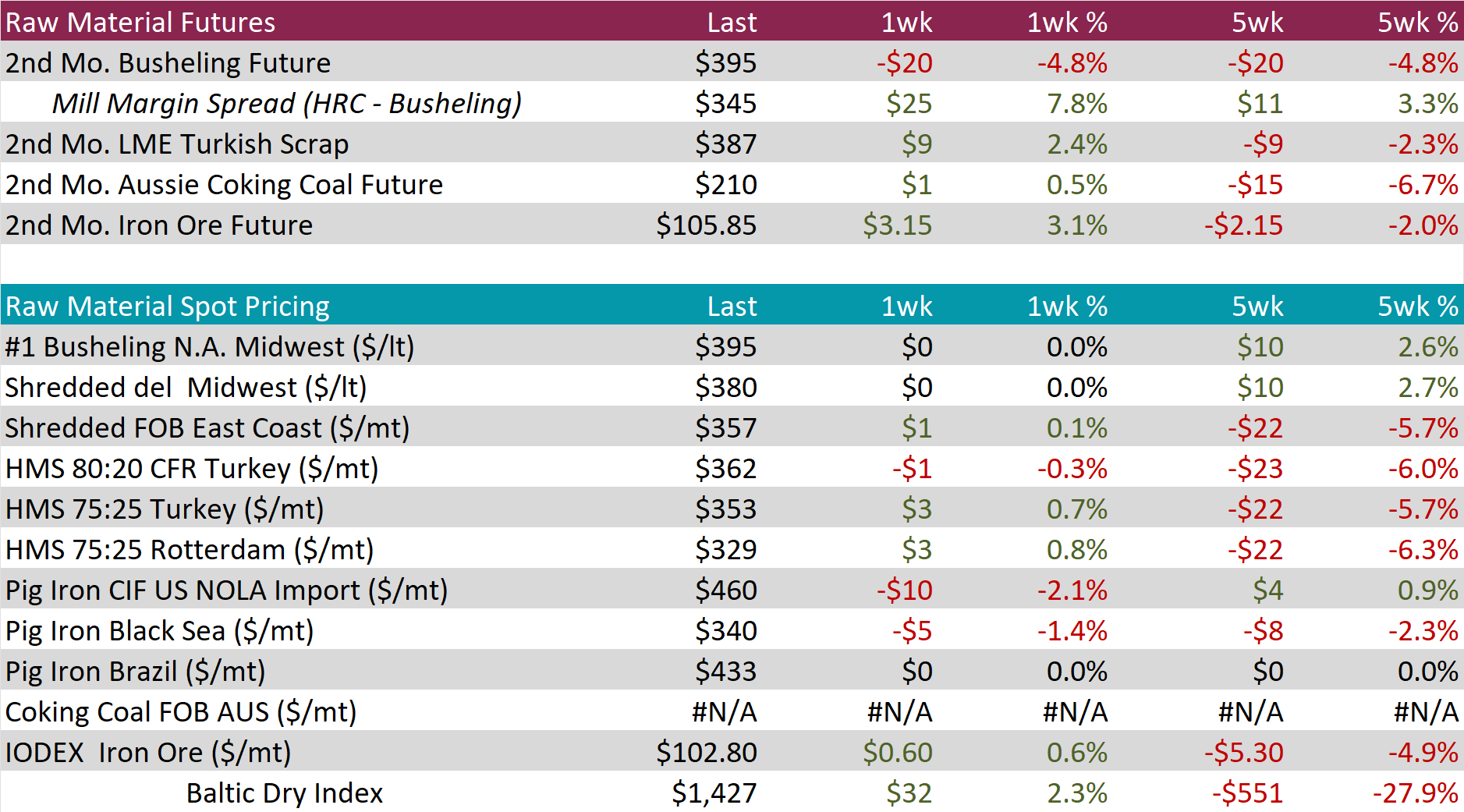

The busheling 2nd month future dropped by $20 or -4.8% to $395, adding to last week’s decline.

The LME Turkish scrap 2nd month future rose by $9 or 2.4% to $387, marking the second consecutive week of increases and hitting the highest price in four weeks.

The iron ore 2nd month future increased by $3.15 or 3.1%, marking the third consecutive week of increases and the highest level in four weeks.

Dry Bulk / Freight

The Baltic Dry Index rose by $32 or 2.3% to $1,427, rebounding from five straight weeks of declines.

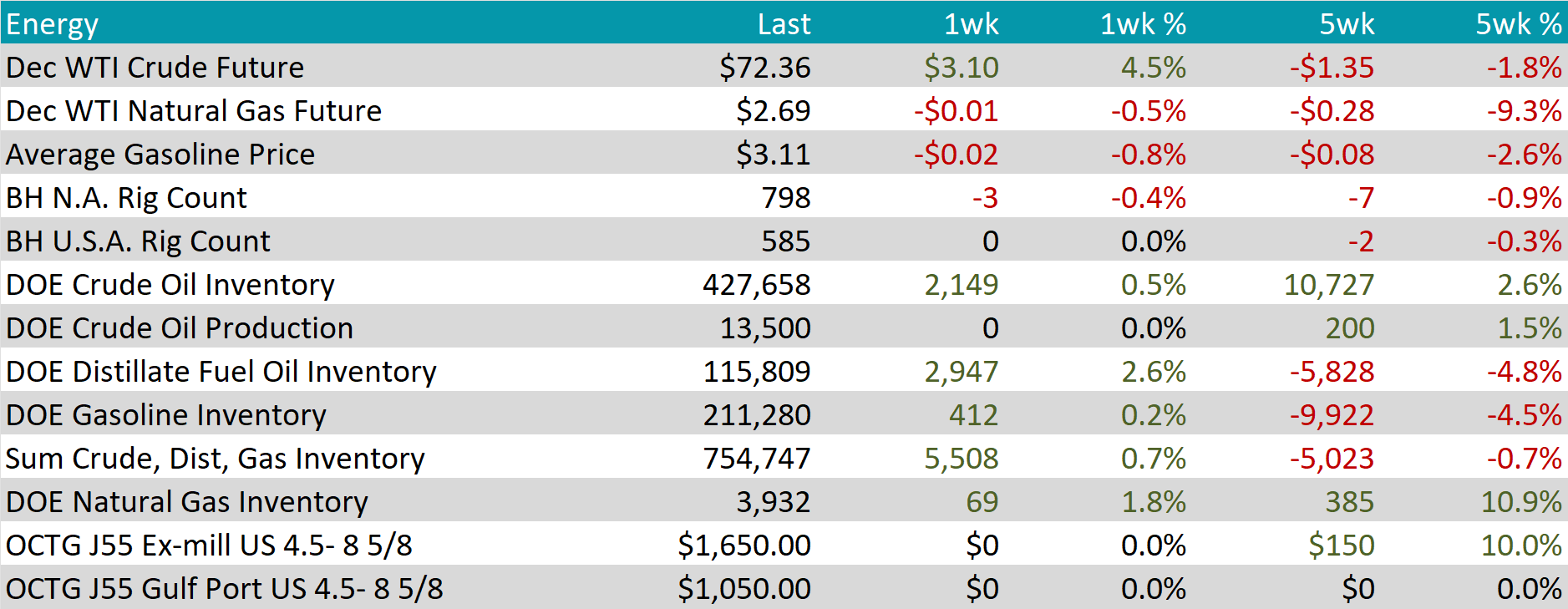

WTI crude oil future gained $3.10 or 4.5% to $72.36/bbl.

WTI natural gas future lost $0.01 or -0.5% to $2.69/bbl.

The aggregate inventory level experienced an increase, rising by 0.7%.

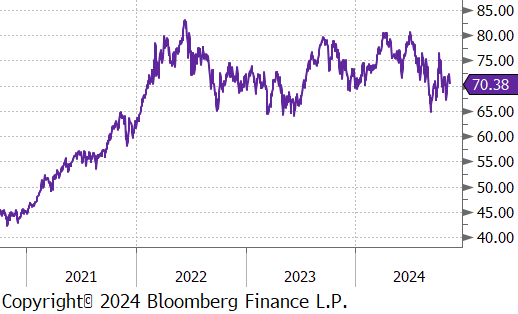

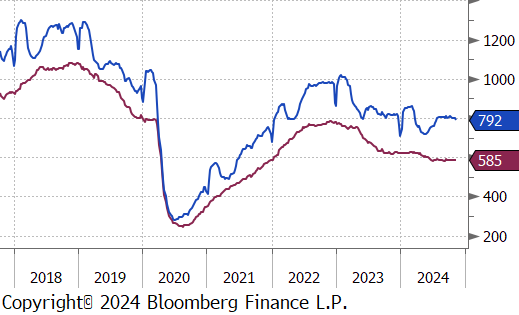

The Baker Hughes North American rig count reduced by 3 rigs, bringing the total count down to 798 rigs, while the US rig count remained unchanged at 585.

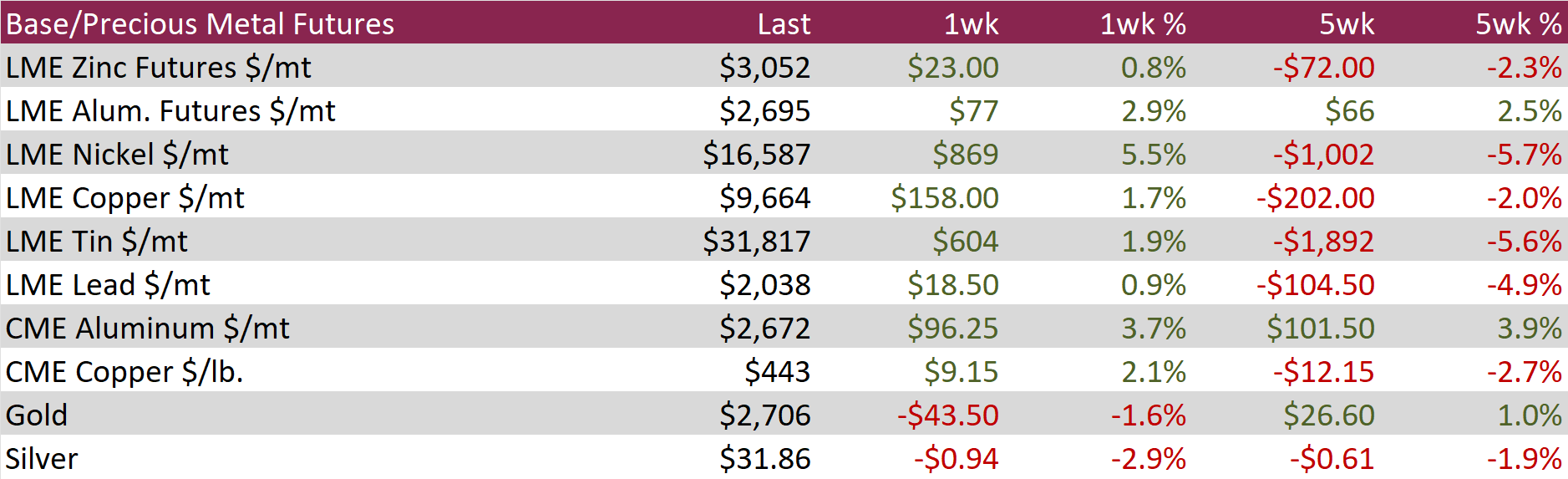

Aluminum futures rose by $77 or 2.9% to $2,695. China unveiled a $1.4 trillion package allowing local governments to swap off-balance sheet debt for better financing terms but stopped short of introducing measures to directly boost consumption. This dampened market expectations for more aggressive stimulus that could spur manufacturing demand. Aluminum has outperformed other base metals this year, supported by a persistent supply crunch for alumina, a critical input for aluminum production. Adding to the supply strain, bauxite prices neared record highs after Guinea, the world’s top bauxite exporter, halted shipments from Emirates Global Aluminum. This disruption, combined with reduced bauxite output from Australia and Jamaica, has squeezed Chinese smelters, driving ore inventories to their lowest levels since 2015.

Copper futures increased by $9.15 or 2.1% to $443. The National People’s Congress announced a CNY 10 trillion debt swap package aimed at helping local governments restructure off-balance sheet debt and access cheaper financing. However, the absence of direct consumer-focused stimulus dampened hopes for a boost in manufacturing demand, clouding the outlook for industrial metals like copper. Adding to the bearish sentiment, China’s low credit growth in October limited the effectiveness of the People’s Bank of China’s (PBoC) recent monetary support. Meanwhile, the U.S. dollar continued its post-election rally, driven by expectations of higher interest rates to counter the expansionary fiscal policies proposed by President-elect Trump. This stronger dollar pressured dollar-denominated commodities like copper and raised concerns about reduced manufacturing demand in emerging markets.

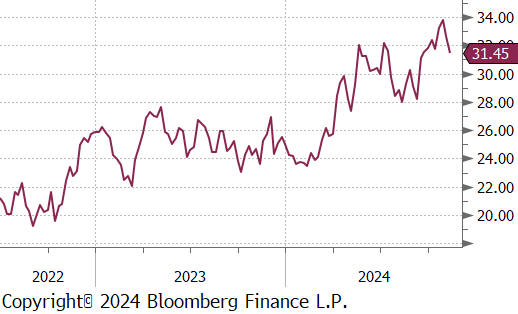

Silver dropped by $0.94 or -2.9% to $31.86 as improved risk sentiment reduced demand for safe-haven assets. Investor focus shifted toward growth equities and cryptocurrencies, driven by expectations of expansionary fiscal policies under Donald Trump’s anticipated second term. Meanwhile, China’s fiscal measures fell short of market expectations, with authorities opting to restructure public debt rather than introduce fresh stimulus to support industrial demand. This lack of targeted support weighed heavily on industrial metals, including silver, which plays a critical role in electrification technologies like solar panels. Adding to the pressure, Chinese-owned solar panel manufacturers reportedly began cutting production in response to fears of higher U.S. tariffs under Trump’s administration, further dampening the demand outlook for silver.

The final results for September’s Durable Goods Orders exceeded expectations, declining by -0.7% versus -0.8%, and up from August’s -0.8% fall. Similarly, Durables Ex Transportation rose by 0.5% versus the 0.4% forecast, improving from August’s 0.4% gain. Together, these suggest that the transportation sector remains weak, with decline in three of the last four months. A key highlight was the 0.7% increase in Orders for Nondefense Capital Goods Ex Aircraft, a leading indicator of business investment plans, following a 0.5% jump in August. This sustained growth reflects optimism and could create a more stable foundation for future steel demand.

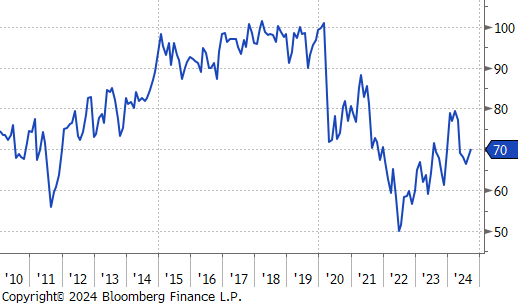

Initial Jobless Claims were slightly below market expectations, 221k vs 222k, but up from the prior week’s 216k. Despite this increase, the figure is significantly lower than the averages from earlier in the month, indicating ongoing resilience in the labor market. Conversely, Continuing Claims rose to 1892k, the highest level since November 2021, surpassing the anticipated climb to 1873k from 1862k in the previous week.

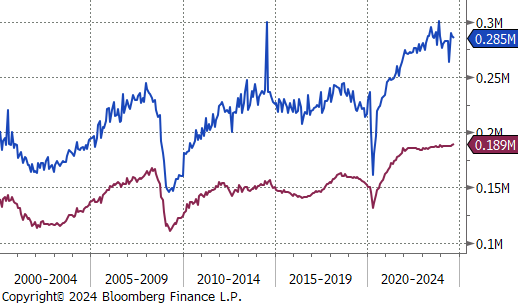

Preliminary estimates for November’s University of Michigan consumer surveys, which do not capture any reactions from the election results, showed the Sentiment Index rising to 73, marking the highest level in seven months, up from 70.5 in October and beating the forecasted 71. Additionally, the 1-Yr Inflation Expectation ticked down to 2.6% versus the expectation to hold steady at 2.7%, hitting the lowest rate since December 2020.

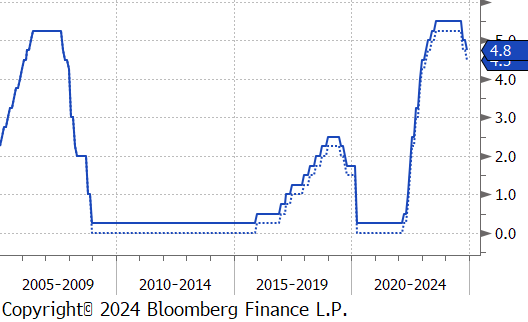

The Federal Open Market Committee (FOMC) unanimously voted for a 25bps interest rate cut, bringing down the range of FED Funds down to 4.5-4.75% from 4.75-5%. The committee noted in the statement that they view risks to the labor market and inflation as “roughly in balance.” While the cutting cycle will continue, Chair Powell also noted that economic data has come in better than expectations of late, suggesting that they may not be as aggressive as the market anticipated a few weeks ago.