Flack Capital Markets | Ferrous Financial Insider

November 17, 2023 – Issue #406

November 17, 2023 – Issue #406

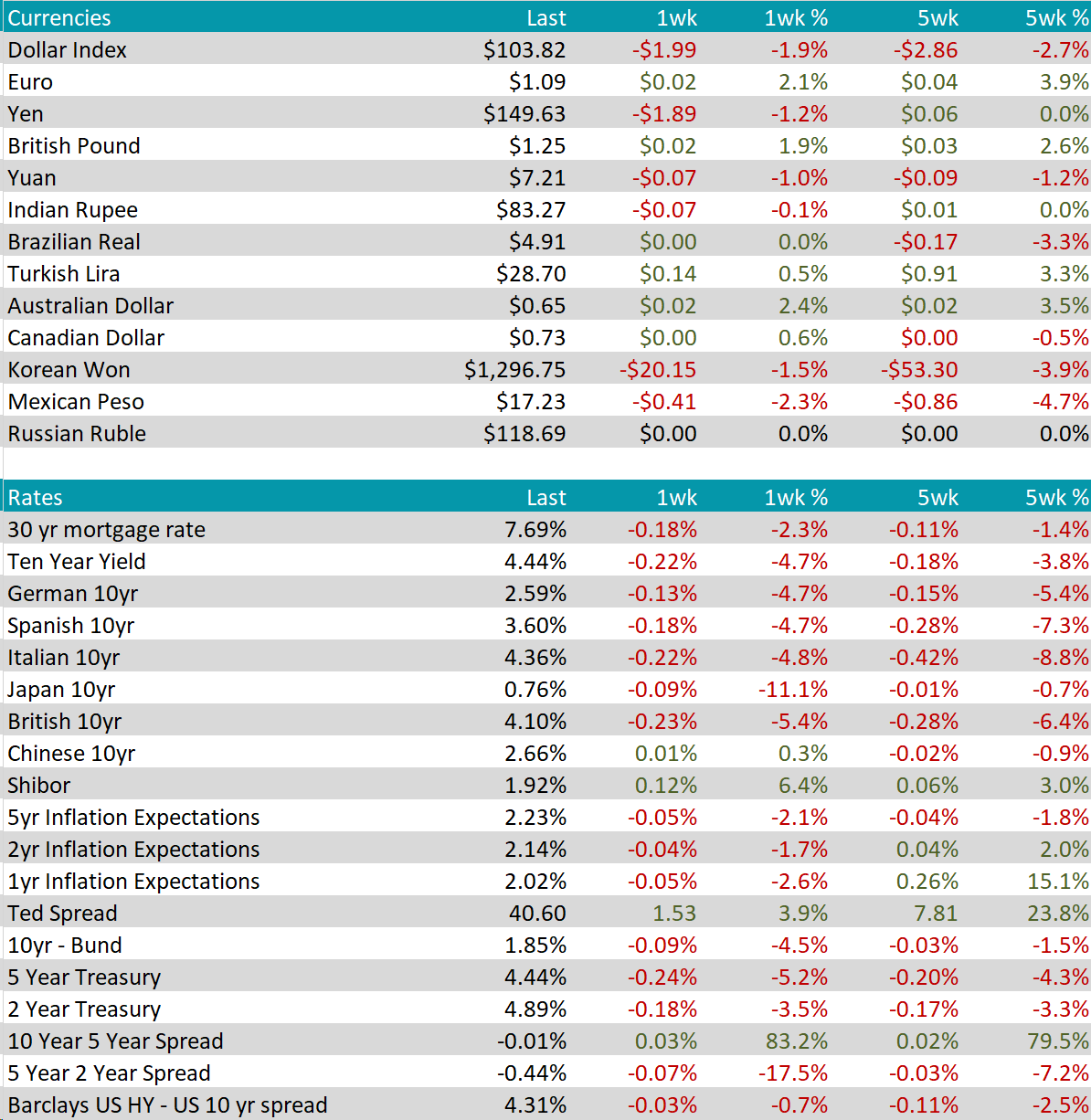

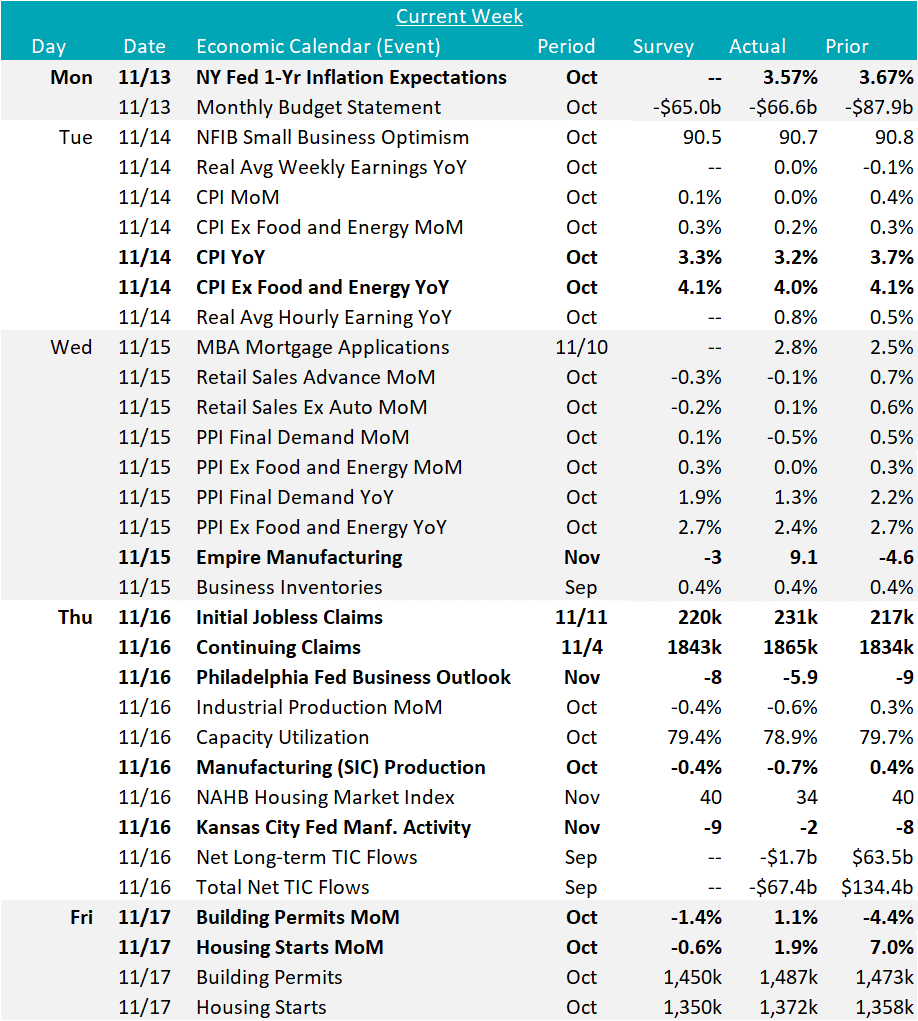

Although softer than expected CPI will take most of the headlines on the economic data front, there were several other important indicators on the industrial side that should be highlighted. First, on the underwhelming side, the FED’s Industrial Production index, which had been surprisingly resilient, decreased in October, down 0.7% versus expectations of down 0.4%. This mirrors the move we saw in all the Fed manufacturing surveys and the ISM PMI for October, as well.

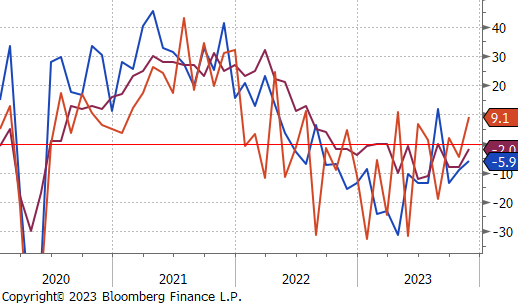

Moving to a more current set of releases, the first round of the November Fed Manufacturing Surveys were released, all 3 surprising to the upside. NY (Empire) surged into expansion territory at 9.1, the highest since April, gaining 14 points and well above expectations of a slight contraction of -3. In a similar fashion, Philadelphia rose to -5.9, above expectations of -8, and Kansas City rose to -2, well above expectations of a decrease to -9. While the latter two indexes remain in contraction territory, the summation of the moves (on the right) indicate an improving albeit restrained environment. While headwinds such as elevated interest rates and customers reporting elevated inventories, it is important to recognize that the worst of the cycle is likely in the rear-view mirror.

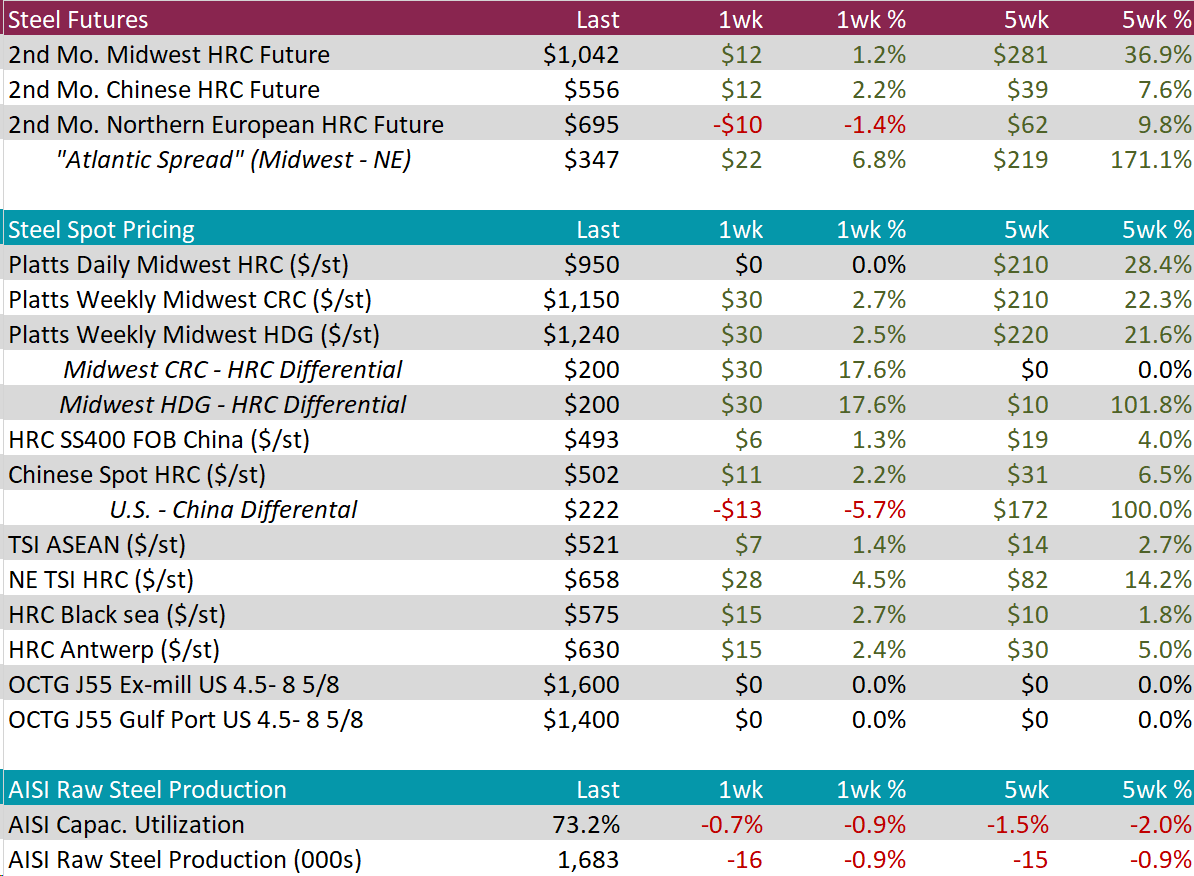

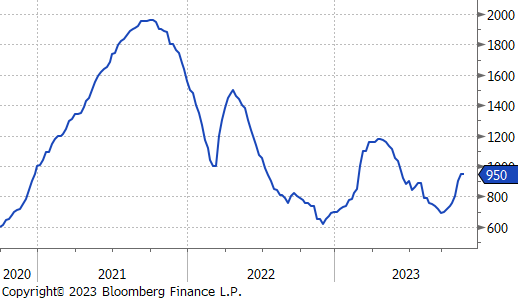

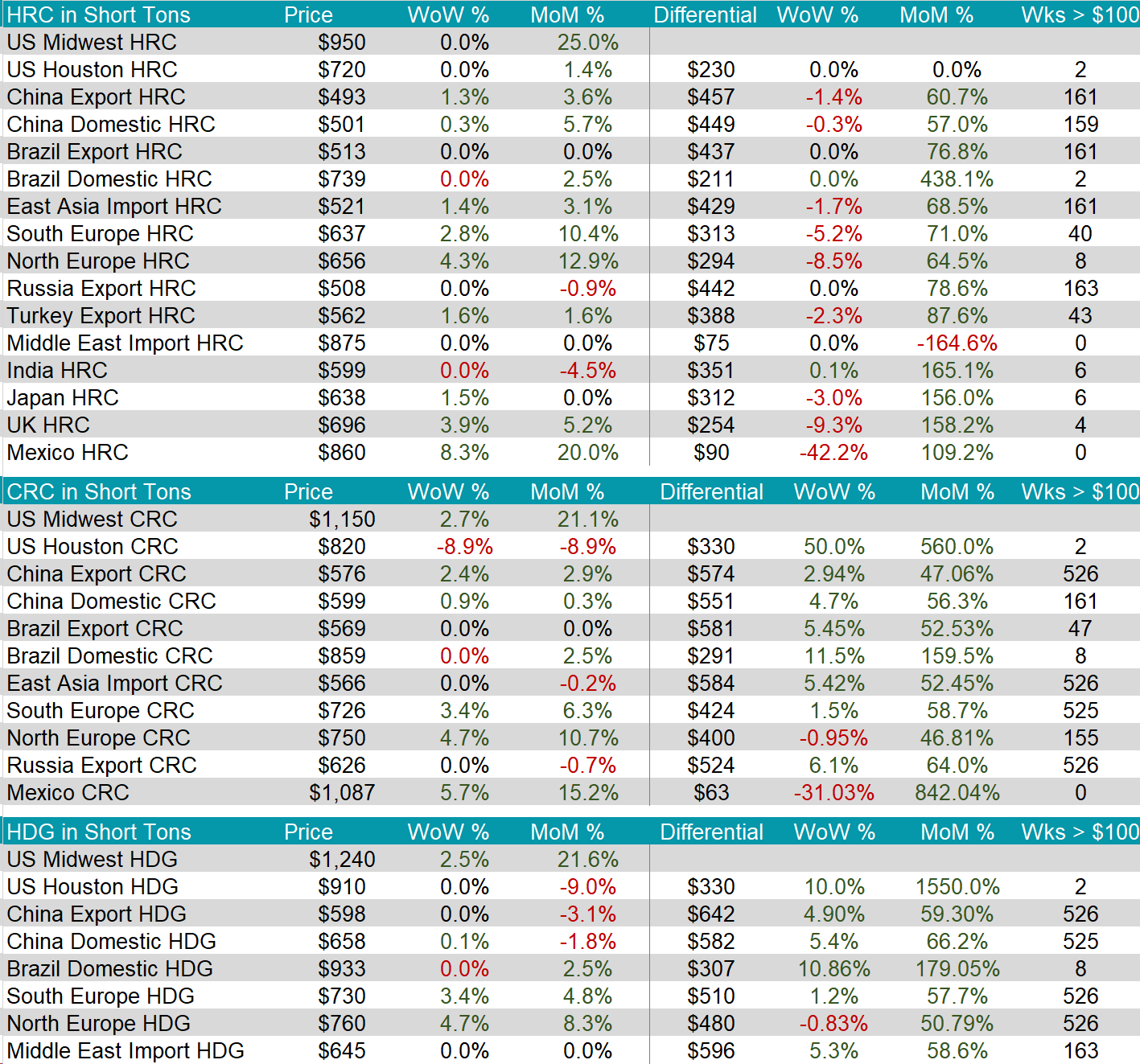

HRC spot price stayed at $950, bringing the five-week percentage increase to 36.9%, or up $281 over five-weeks, while the 2nd month future rose by $12, or 1.2%, to $1,042, reaching the highest price since mid-April.

Tandem products both increased by $30, bringing the CRC up to $1,150 and HDG up to $1,240, resulting in the HDG – HRC differential increasing by $30, or 17.6%, to $200.

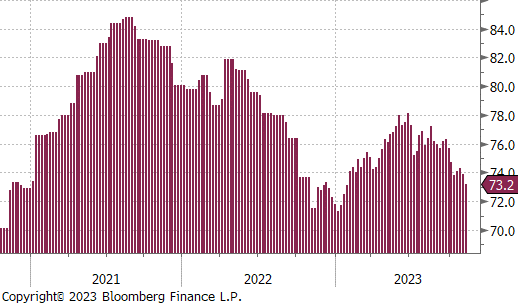

Mill production ticked down by -0.7% to 73.2%, bringing raw steel production down to 1.683M tpm. This is the second week in a row of capacity utilization reductions.

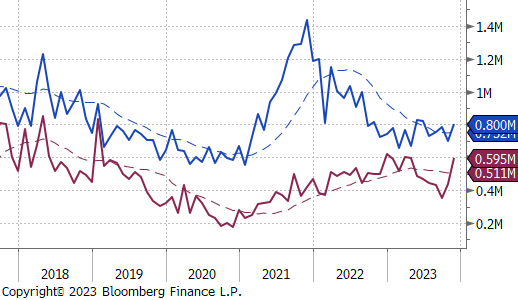

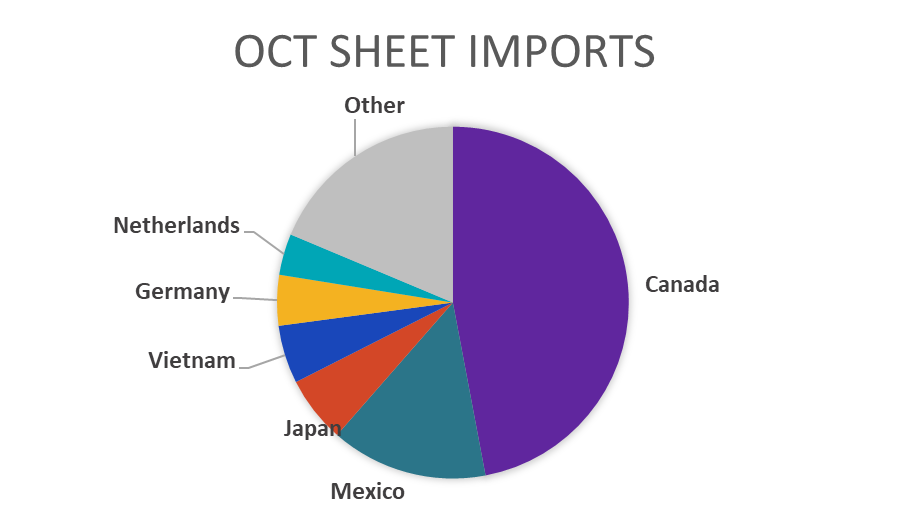

November Projection – Sheet 800k (up 100k MoM); Tube 595k (up 159k MoM)

October Projection – Sheet 700k (down 81k MoM); Tube 436k (up 87k MoM)

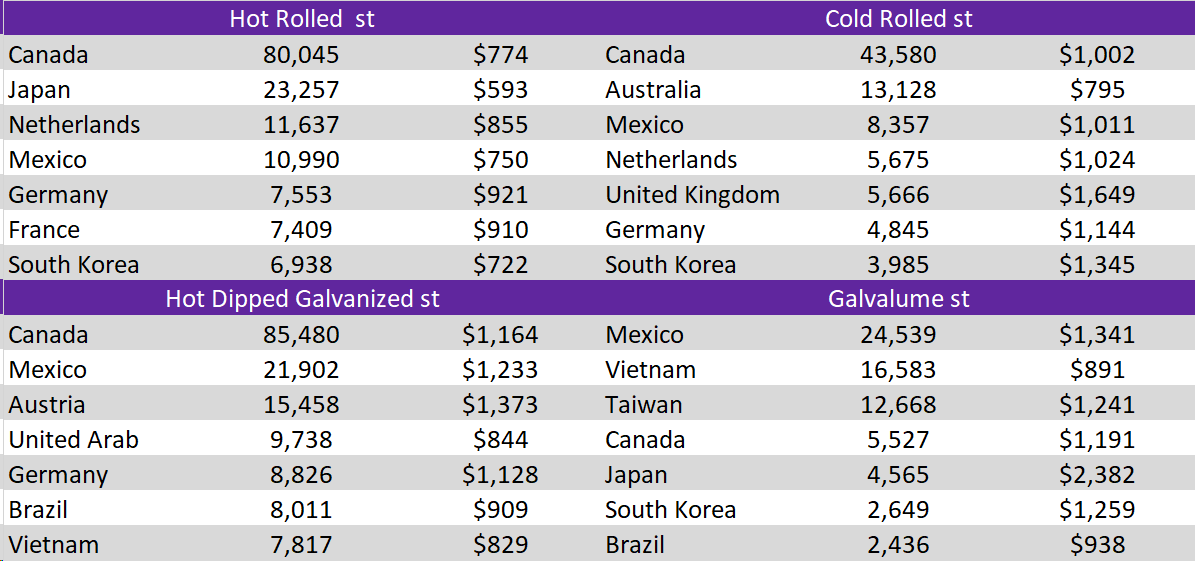

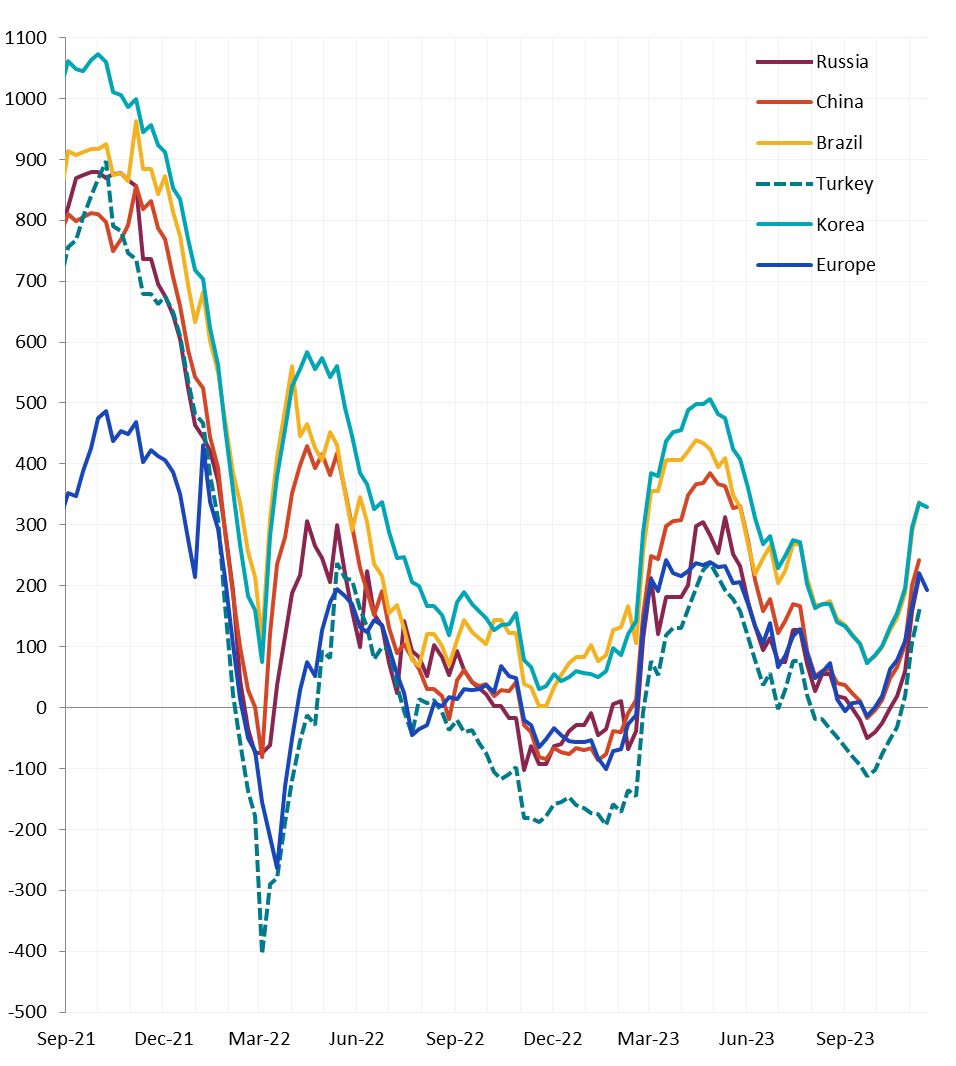

Global differentials were mixed with some remaining unchanged and others decreasing. Most notably, North Europe decreased by 8.5%, South Europe decreased by 5.2%, and China decreased by 1.4%.

Scrap

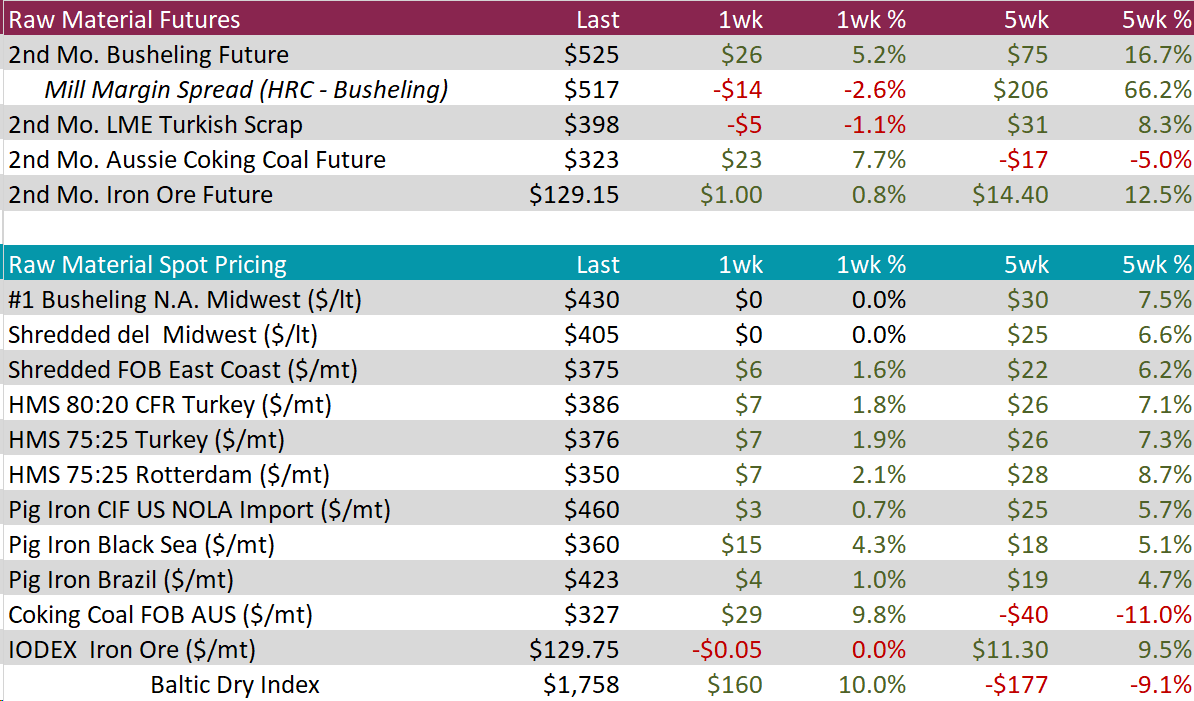

The 2nd month busheling future continued to increase, surging up by $26, or 5.2%, to $525, hitting the highest price seen since early April. Furthermore, since hitting the most recent low of $425 six-weeks ago, the price has rallied by $100.

The 2nd month LME Turkish scrap slightly dipped down by $5, or -1.1%, to $398, after experiencing a $46 increase in price over three-weeks.

The 2nd month Aussie coking coal future continues to jump around, this time rising by $23, or 7.7%, to $323, after experiencing a decrease of $36 over two-weeks.

Dry Bulk / Freight

The Baltic Dry Index rebounded by $160, or 10%, to $1,758, after three-weeks of falling from recent high of $2,046.

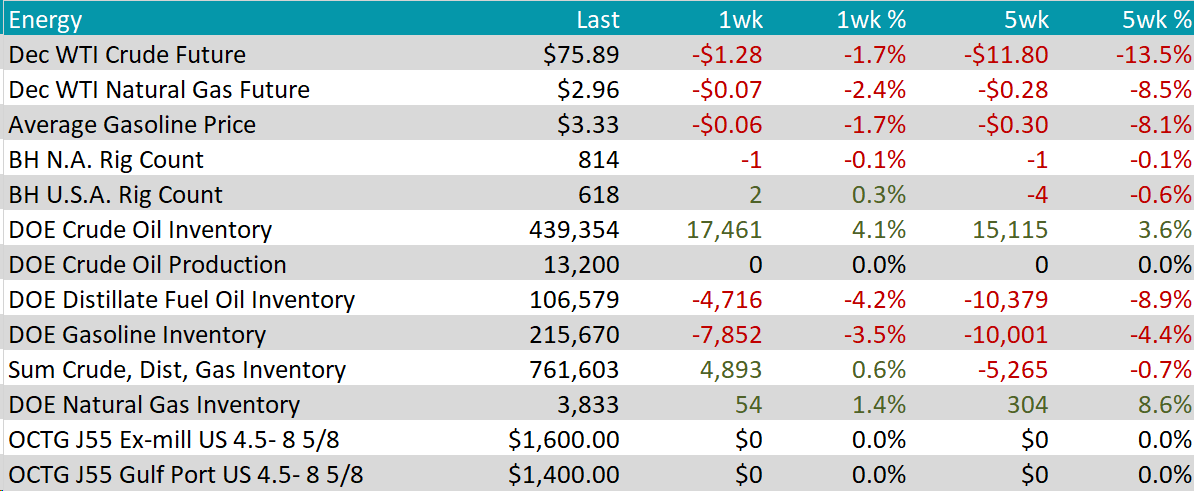

WTI crude oil future lost $1.28 or 1.7% to $75.89/bbl.

WTI natural gas future lost $0.07 or 2.4% to $2.96/bbl.

The aggregate inventory level rose by 4,893 or 0.6%.

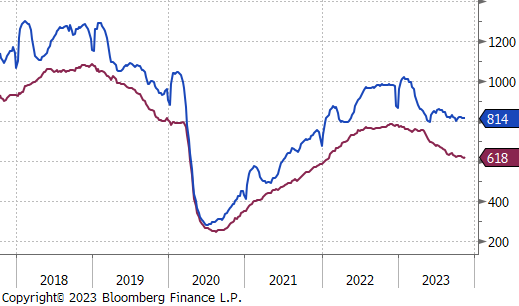

The Baker Hughes North American rig count declined by 1, bringing the total count to 814 rigs. The US rig count saw an increase of 2 rigs, bringing the total count to 618 rigs.

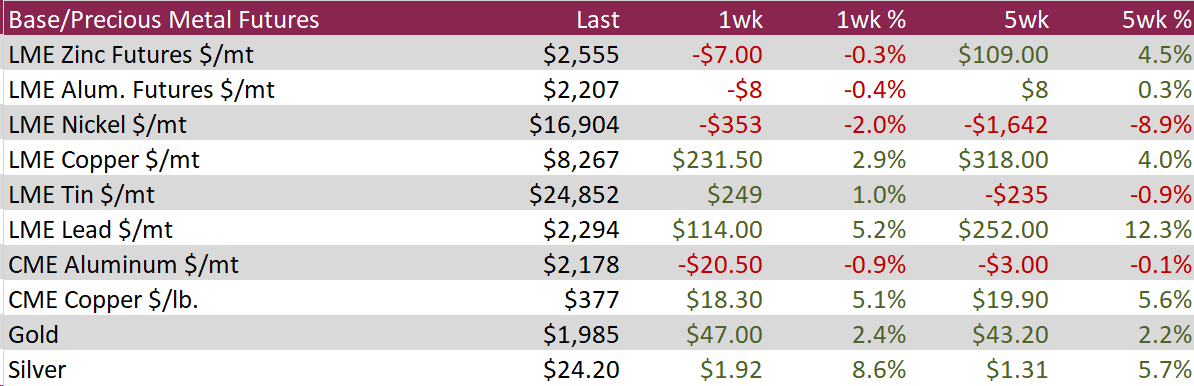

Aluminum fell by $8, or -0.4%, to $2,207, staying over the $2,200 per ton level, continuing momentum since rallying from the two-month low of $2,176 touched on October 23rd as supply concerns continue to coincide with growing forecasts of higher demand. China has stopped expanding production capacity and production is also capped by Indonesia’s ban on bauxite exports. Meanwhile, China pledged to borrow an additional CNY 1 trillion to assist infrastructure and manufacturing, meeting the demand for resources. Furthermore, there have been speculations indicating that the PBoC would potentially provide an additional CNY 1 trillion in liquidity to other policy banks to stimulate construction activity.

In the same regards, copper rose by $18.30, or 5.1%, maintaining two-month highs, as lower inventories and bets of stronger demand in the near term continue. Inventories at the SHFE dropped by 45%, and evidence of slowing prices in the US pressured the dollar used to price copper raised hopes of manufacturing financial conditions. Furthermore, the CNY 1 trillion from China and the reports of PBoC potentially injecting CNY 1 trillion lifted the outlook for copper as well.

After gaining more than 2% last week, or $47, gold prices steadied at $1,985. This was supported by an easing in US inflation, which gave traders hope that the Fed’s tightening cycle is coming to an end, as they shifted their attention to possible interest rate cuts next year. The markets predict a 30% possibility that the Fed may start cutting rates as early as March 2024. For more direction, investors are currently awaiting the most recent FOMC minutes as well as a plethora of US economic data. As anticipated, the PBoC in Asia maintained its prime rates for one- and five-year loans at 3.45% and 4.2%, respectively.

Initial jobless claims jumped up to 231k, hitting the highest in nearly three-months, and well above market expectations of an increase to 220k from the prior reading of 217k. At the same time, continuing claims rose to 1865k, the highest in nearly two-years and sharply above expectations of a rise to 1847k from the prior reading of 1834k, indicating that those unemployed are starting to have a more difficult time finding suitable employment. This represents a clear indication that the labor market has more softening in the pipeline. Alarm bells around missing the soft landing will not start ringing unless the 3-week moving average pushes well above 260k for initial claims.

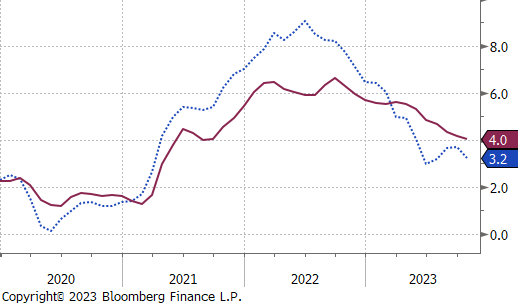

CPI came in below the market forecasts, with CPI YoY falling to 3.2%, MoM Core CPI (ex. food and energy) decreasing to 0.2% from September’s print of a 0.3% increase, and the YoY Core CPI slowing to a rate of 4%, marking the slowest increase since September 2021. This was a welcome sign of continued relief from rising prices after recent indicators and reports have been pointing to sticky prices, as well as bolstering views that the Fed’s rate hikes are ending.

Finally, building permits and housing starts continue to show resilience. Both beat expectations with permits up 1.1% versus expectations of being down 1.4% and starts were up 1.9% versus the expectation of down 0.6%. This continues to show that the appetite for housing remains strong, with existing home inventories at decades low levels.

The euro strengthened to $1.09, nearing its highest since mid-August, driven by anticipation for the Federal Reserve and European Central Bank’s meeting minutes. The prevailing weakness of the dollar, fueled by the belief that the Federal Reserve has completed its rate hikes, contributed to the euro’s momentum. Market sentiment suggests a potential 100 basis point reduction in US interest rates next year, countered by ECB President Christine Lagarde and policymaker Villeroy de Galhau’s commitment to maintaining higher interest rates.

The Japanese yen appreciated beyond 150 per dollar, nearing its strongest in two months amid a broader decline in the US dollar. Weaker-than-expected US inflation and labor readings raised hopes that the Federal Reserve might initiate interest rate cuts next year, putting pressure on the DXY. Investors looked to manufacturing and services PMI figures and inflation data for guidance, while recent data revealed Japan’s Q3 economic contraction due to slowing global demand. The Bank of Japan reaffirmed accommodative monetary policies, making minor adjustments to yield curve controls.

The yield on the US 10-year Treasury note edged down to 4.44%, marking its lowest in about two months, distancing itself from October highs of 5%. The Federal Reserve’s November meeting conveyed a more dovish tone, signaling a potential peak in interest rates and prompting investor speculation about rate cuts as early as March. Ongoing economic indicators suggested a slowdown, with cooling inflation and labor market trends contributing to downward pressure on the 10-year Treasury note yield.