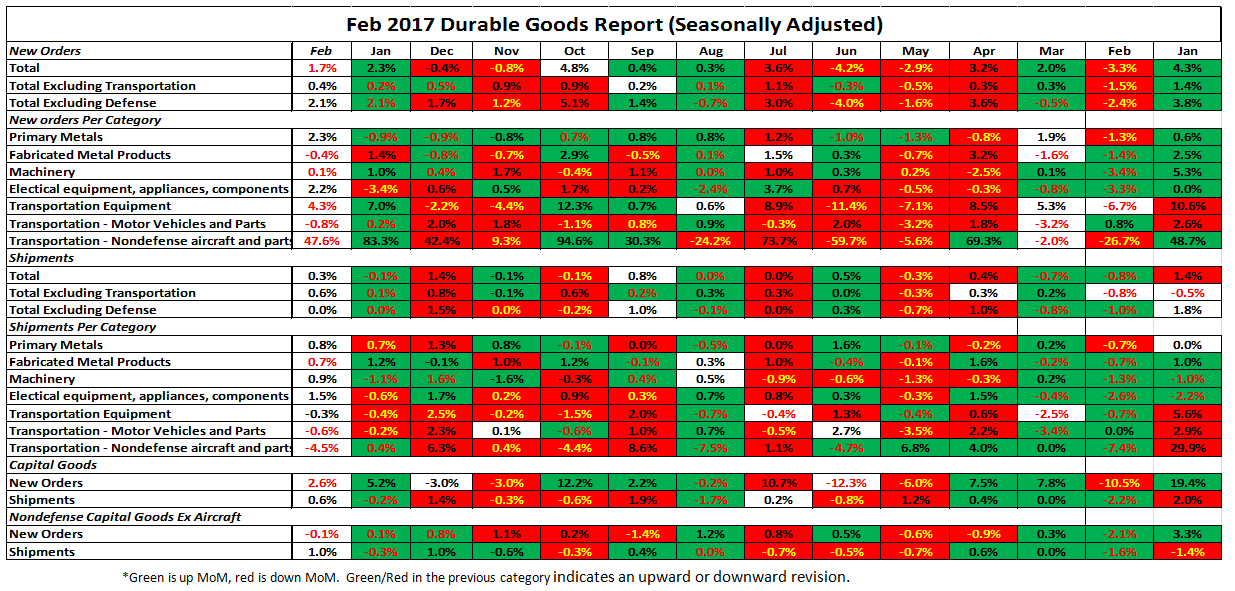

The February Durable Goods Report gained for the second month with new orders up 1.7% MoM, new orders ex-transportation up 0.4% MoM and new orders ex-defense up 2.1% MoM.

Capital goods orders gained 2.6% after a 5.2% gain in January. New orders for nondefense capital goods ex-aircraft slipped 0.1%, but as you can see in the chart below, the downtrend looks to have been broken.

February Capital Goods New Orders Nondefense Ex-Aircraft SA

YTD data below shows slight gains across the primary three categories. The sub-sectors primary metals, fabricated metals and machinery are off to a strong start after a dismal 2016.

February saw an increase in inventory spending just above 1% across the three primary categories. Most of January’s inventory spending was revised lower. Total inventory was down 0.1% YoY.

Domestic flat rolled prices continued higher while Chinese and ASEAN prices fell.

TSI North European HRC remains range bound while TSI ASEAN HRC moved lower.

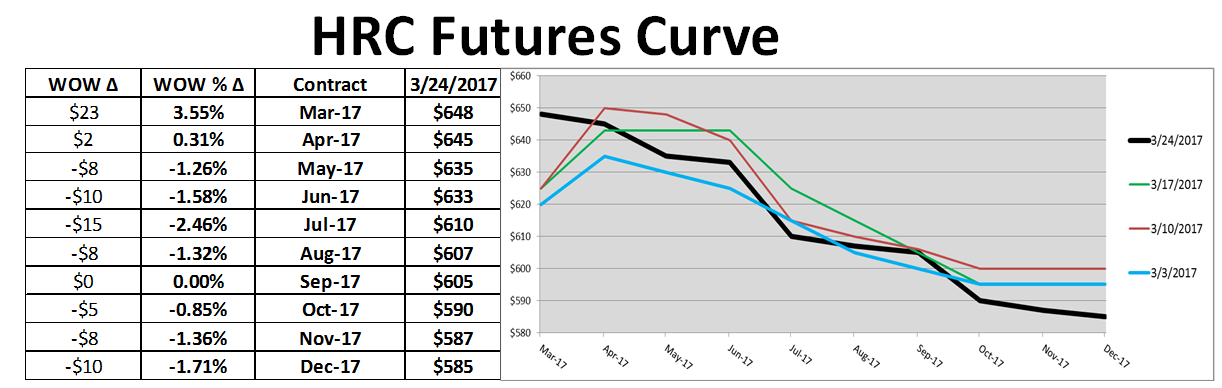

CME Midwest HRC futures were under pressure last week. April settled at $645/st, May at $635/st and June at $633/st. Q3 fell back into the $605-$610/st range while Q4 fell below $590.

The TSI Daily Midwest HRC Index gained $14/st to $654, now above April HRC futures at $645/st.

April CME HRC Futures vs. TSI Daily Midwest HRC Price

The March flat rolled import license forecast continues to remain subdued.

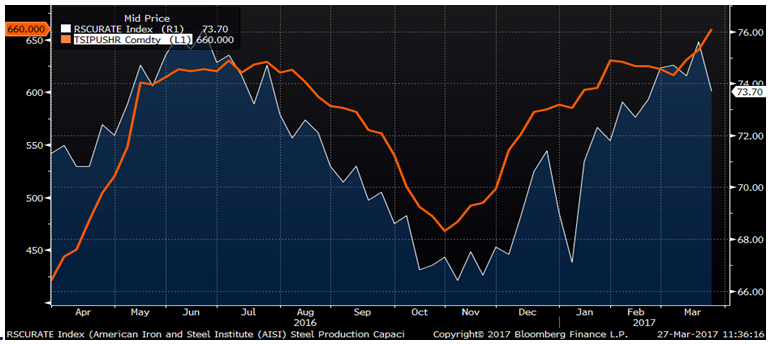

AISI Steel Capacity Utilization Rate and TSI Daily HRC Price

.

AISI data saw an abrupt fall in production last week.

Black Sea pig iron gained another $10 while the rest of the complex was under massive pressure.

The iron ore curve shifted lower remaining steeply backwardated through 2018.

Chinese rebar futures fell 5%, Black Sea billet fell 5% and Turkish rebar dropped 3%.

The Kansas City Fed increased to 20 from 14 as the energy sector continues to gain momentum. February New Home Sales increased to 592k up from 558k in January and beat expectations of 525k. February Existing Home Sales fell to 5.48m annualized from 5.69 in January and missed expectations of 5.55m homes.

The S&P fell over 1% after the health care bill was pulled. China saw its markets gain nicely while Japan fell over 1%. Europe was unchanged.

Steel related stocks were clubbed after sharp drops in raw materials and the faltering reflation trade, even with HRC indexes breaking above the $650/st level.

Olympic Steel

Iron ore miners fell sharply with ore prices.

Aluminum gained 1.3% while the other base metals were down noticeably.

LME Alumninum

LME Nickel

The dollar index fell below 100 while the Japanese yen gained over 1%. The Mexican Peso gained almost 2% and the Aussie dollar fell 1%.

US Dollar Index

Japanese Yen

Mexican Peso

Australian Dollar

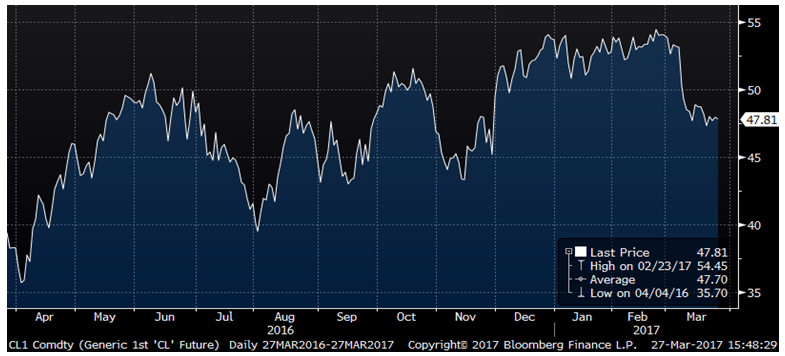

Crude oil prices were under pressure again closing the week just below $48/bbl. Production continued higher, crude oil inventory gained almost 1% while the aggregate energy inventory level was unchanged. The US rig count gained 20 rigs while the Canadian rig count fell sharply. Natural gas gained 4% to $3.08/mbtu with inventory falling 7%.

April WTI Crude Oil Futures

Aggregate Energy Inventory (Blue) vs. WTI Crude Oil Futures

D.O.E. Crude Oil Inventory

D.O.E. Crude Oil Inventory Perspective (1982 – Present)

Baker Hughes US Rig Count

D.O.E. Crude Oil Production

D.O.E. Crude Oil Production Perspective (1984 – Present)

Ten year treasury rates fell also as confidence slid after the failed healthcare reform attempt.

U.S. 10 Year Bond Yield

The list below details some upside and downside risks relevant to the steel industry. The bolded ones are occurring or look to be highly likely. Upside risks look to be in charge.

Upside Risks:

– China pumping up its “old economy”

– Energy industry rebound

– Border adjustment tax

– Big rally triggered by price increases/low inventory/restocking

– President Trump’s agenda

– Infrastructure bill/long-term solution to highway spending bill

– China getting serious about curtailing steel production

– Transportation supply constraints

– Essar labor issues

– Post-election economic pick up

– Massive restocking (domestic and/or global)

– Unplanned domestic supply side disruptions

Downside Risks:

– Political uncertainty – Reflation trade reversing

– Increasing oil and iron ore inventory levels

– Automotive industry under pressure

– US domestic producers bringing back on capacity

– Higher interest rates slowing residential construction and auto sales

– Tightening financial conditions pressuring auto sales driven by sub-prime financing

– Chinese restrictions in property market

– The Chinese Financial Crisis

– Unexpected sharp China RMB devaluation

– Rebound in import volumes

– Increasing import differentials

– Resumption of US dollar rally/currency issues/sovereign default

– U.S. (manufacturing) recession

– Falling ferrous raw materials and global finished steel prices

– Economic downturn, especially in China or Europe reverberating to U.S.A.

– Weak demand in housing or automotive