Content

-

Weekly Highlights

- Market Commentary

- Upside & Downside Risks

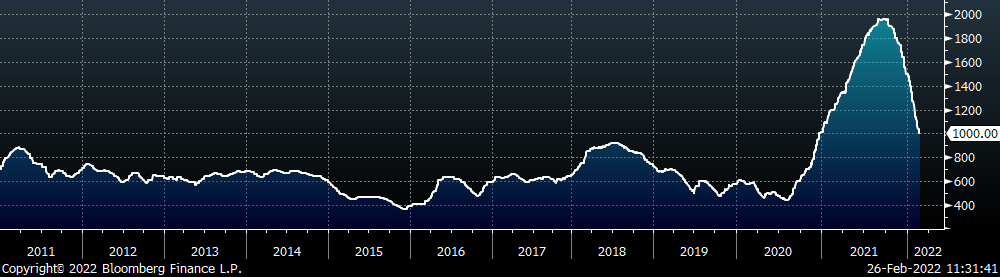

Since the beginning of February, we have been noting the progressive shift in mill behavior, where the increased volume of inquiries has led them to pull back in negotiations. As the weeks went on, this dynamic became more pronounced, and as prices continued to rapidly fall, we have also been highlighting the fact that upside price risks were rapidly mounting. From the buyer’s side, if you read these reports and keyed in on the fact that we anticipated lower spot prices, you were right to do so. Now, those lower prices have arrived – the spot price today is $200 lower than it was at the beginning of the month. We anticipate that the bottom of HRC prices is right around the corner. While some lagging indexes may continue to print lower in the next couple of weeks, new deals for HRC below $1,000 have all but dried up. The increased number of inquiries are now becoming orders, and as the rest of the market wakes up to this new reality, we anticipate very few headwinds to slow down the rising spot market.

More importantly, for buyers who did not listen to our bullish perspective on the second half of the year and locked in HRC price below $1,000, unfortunately, that opportunity has passed by entirely. Here’s what has changed since last week:

As it stands today (March 1st), the current fixed HRC base price for the remainder of 2022 is $1,175. That’s $225 higher than what was available on February 18th. You may have noticed that we have not mentioned the Russian invasion into Ukraine up to this point, when talking about the upside risk for the remainder of the year. That is because the bottom was going to happen anyway, the result of the escalating conflict in the CIS has not yet been priced into the U.S. domestic spot market but it will push the ceiling higher and extend the upcycle.

While it is far too early to know every way this conflict and the retaliatory sanctions will impact global trade, we do know that millions of tons of steel production and iron ore will be been taken out of the market. Russia and Ukraine are the 3rd and 13th largest steel producers, respectively, according to the Department of Commerce & S&P Global. Additionally, Ukraine is the 5th largest producer of global iron ore, and the CIS is the most significant exporter of pig iron to the U.S. Global steel prices are already meaningfully higher than they were at the beginning of 2022. Pulling these expected tons out of circulation will put more pressure on global supply chains and on prices. Here in the U.S. the immediate impact will cause higher raw material prices, as global availability and substitute goods evaporate. Furthermore, if the already severed relationship between the E.U. and Russia gets any worse, the E.U. may be forced to dramatically reduce steel production due to their limited access to Oil & Gas. It’s not out of the question that the U.S. may end up being a source of steel supply both here domestically and in Europe.

Below are the most pertinent upside and downside price risks:

Upside Risks:

Downside Risks:

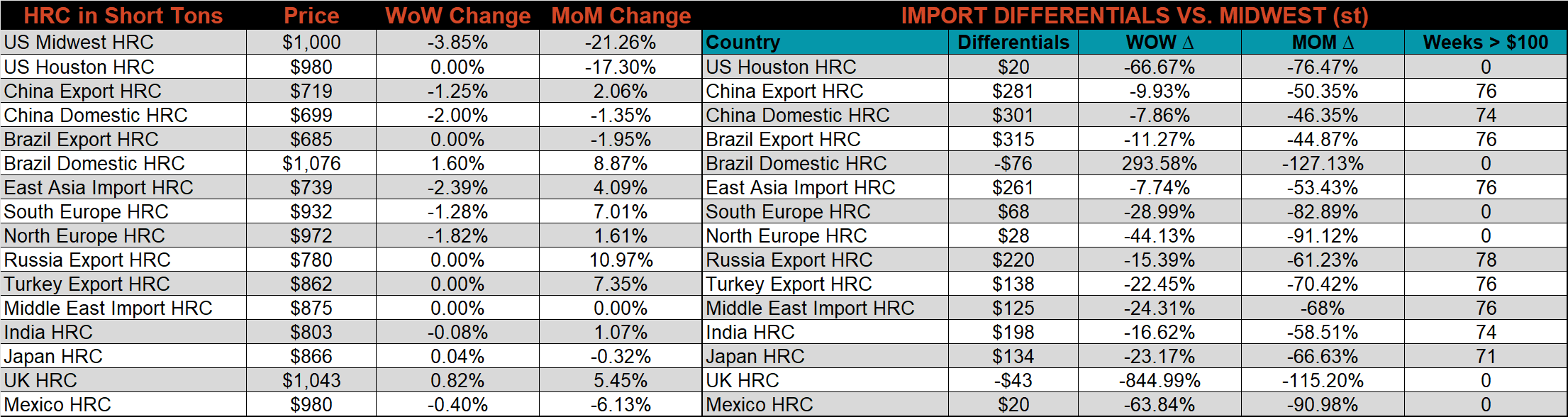

The Platts TSI Daily Midwest HRC Index decreased by another $40 to $1,000.

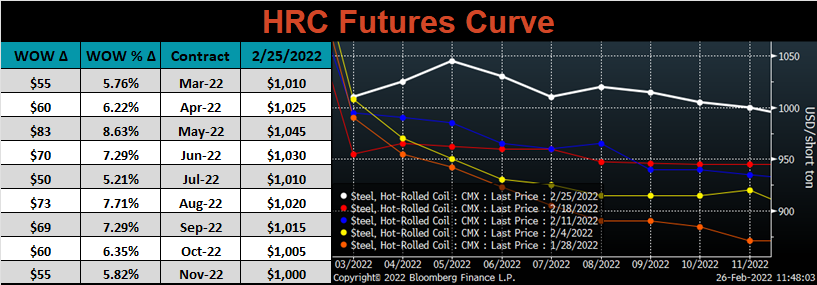

The CME Midwest HRC futures curve is below with last Friday’s settlements in white. The entire curve shifted higher, as the market reacted to price announcements and the prospect of higher input costs caused by the Russian-Ukrainian conflict.

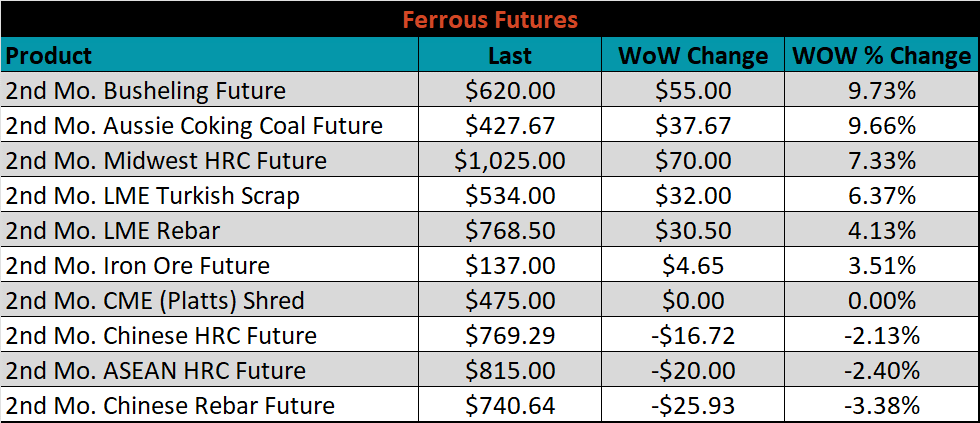

April ferrous futures were mixed. Midwest busheling gained another 9.7%, while Chinese rebar lost 3.4%.

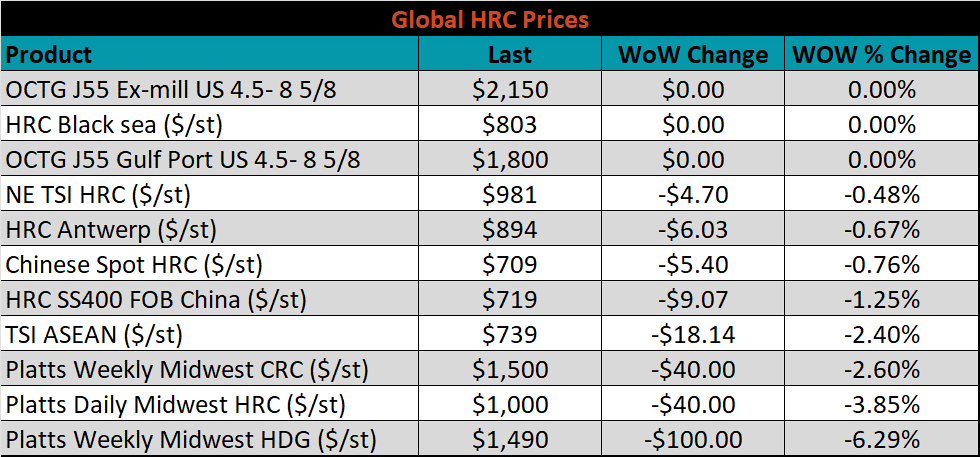

Global flat rolled indexes were all lower, led by Midwest HDG, down another 6.3%.

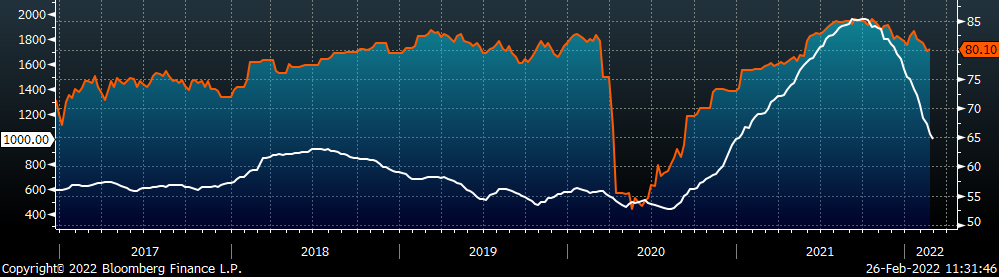

The AISI Capacity Utilization was up 0.3% to 80.1%.

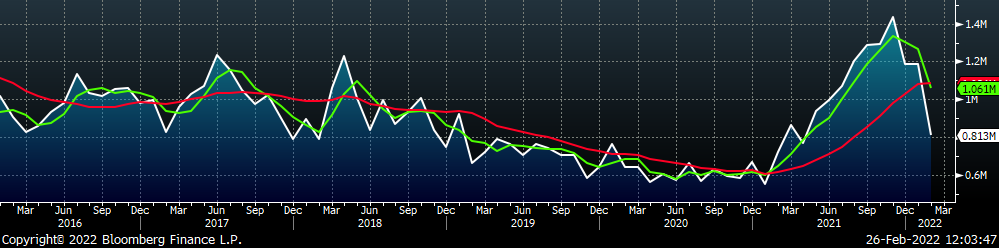

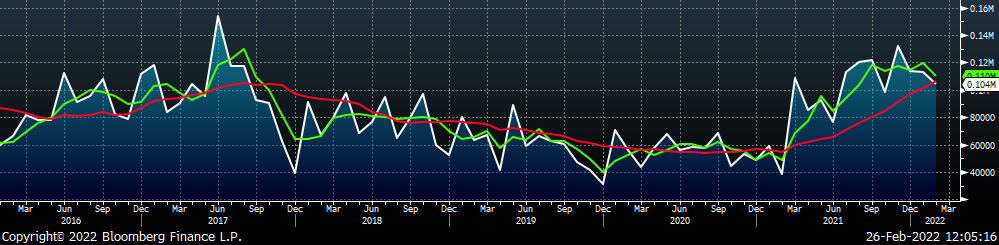

February flat rolled import license data is forecasting a decrease of 371k to 813k MoM.

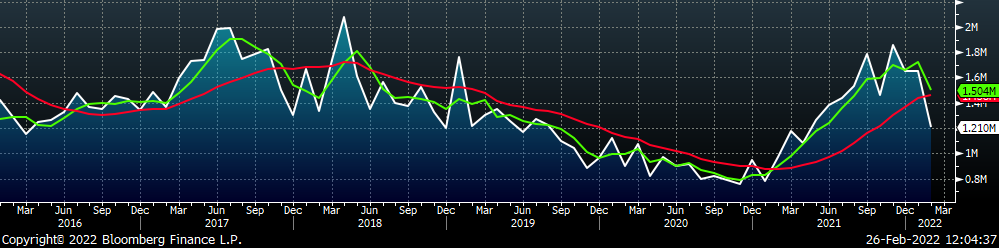

Tube imports license data is forecasting a decrease of 68k to 397k in February.

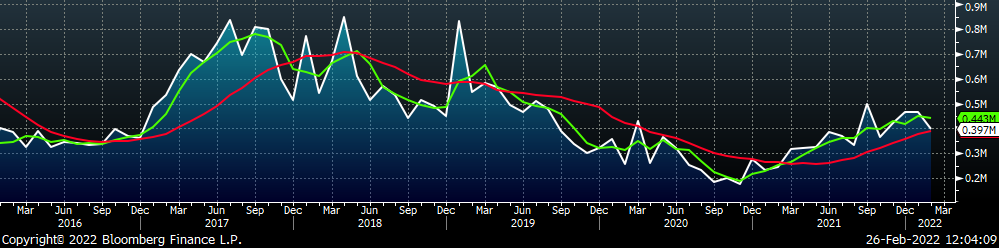

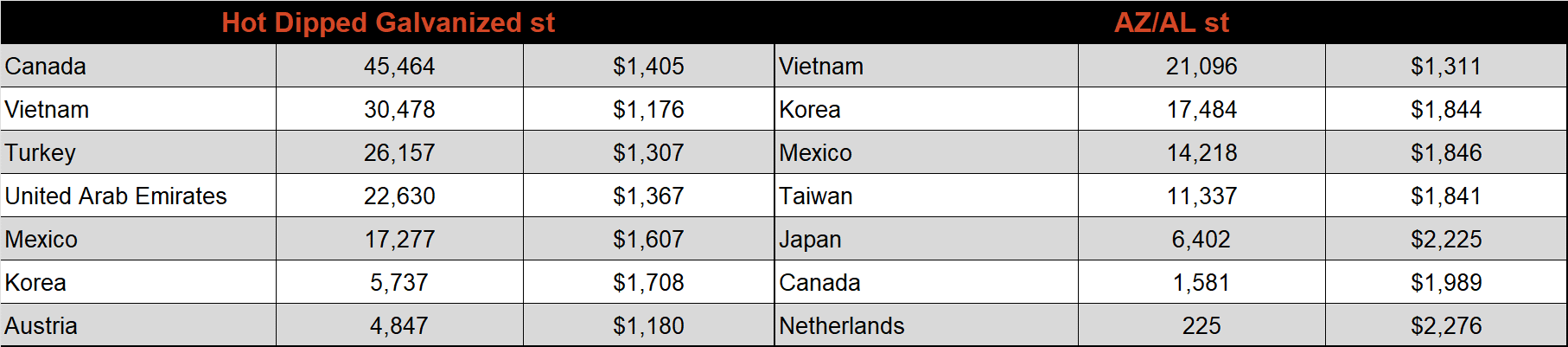

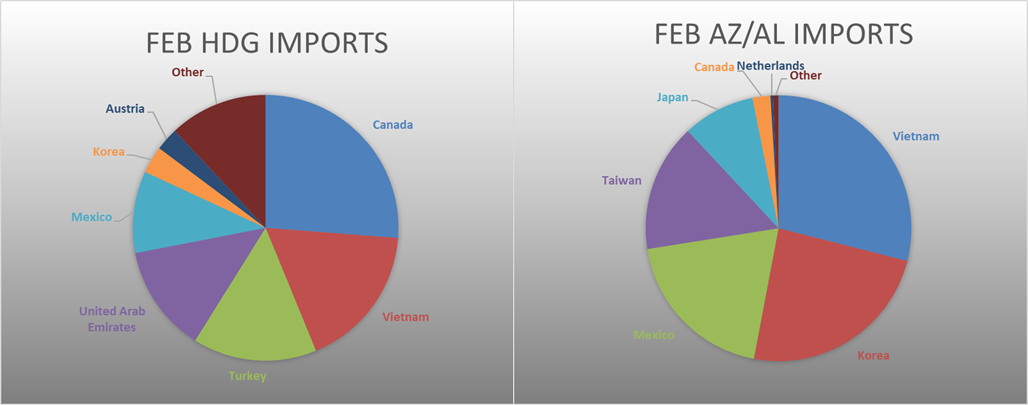

February AZ/AL import license data is forecasting a decrease of 9k to 104k.

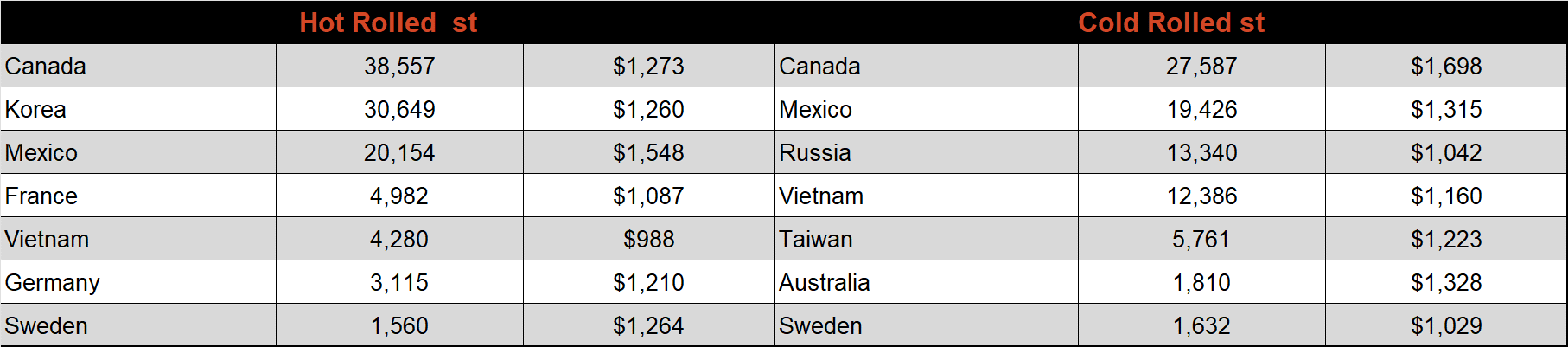

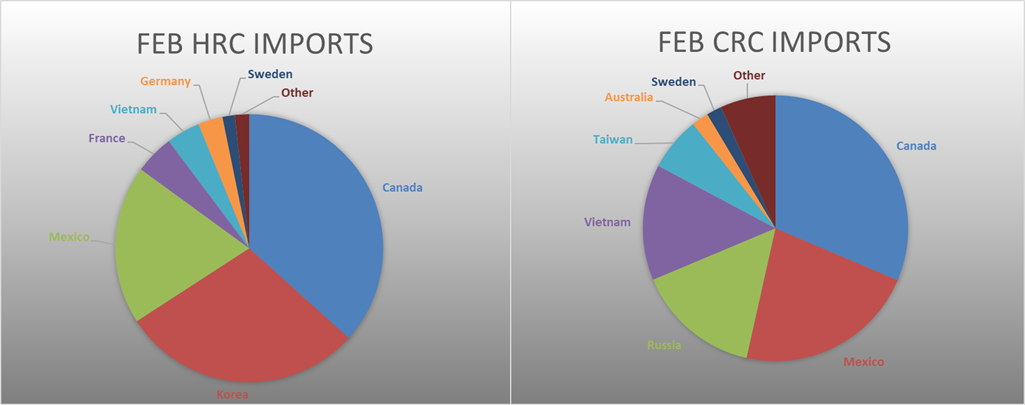

Below is February import license data through February 21th, 2022.

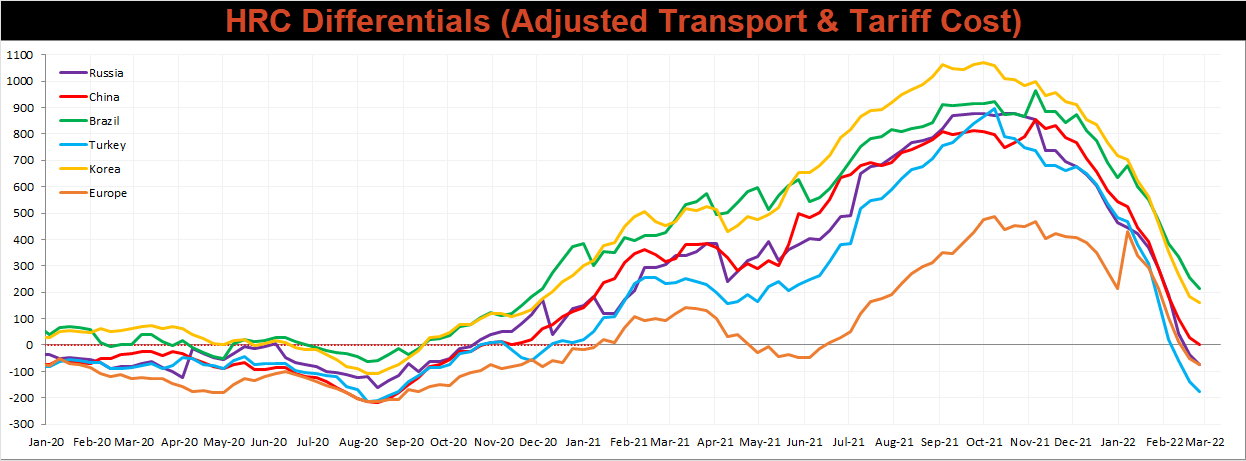

Below is the Midwest HRC price vs. each listed country’s export price using pricing from SBB Platts. We have adjusted each export price to include any tariff or transportation cost to get a comparable delivered price. All the watched countries differentials decreased again this week.

SBB Platt’s HRC, CRC and HDG pricing is below. The Midwest HDG, HRC, and CRC prices were down 6.3%, 3.9%, and 2.6%, respectively. Outside of the U.S., the East Asian HRC price was down, 2.4%.

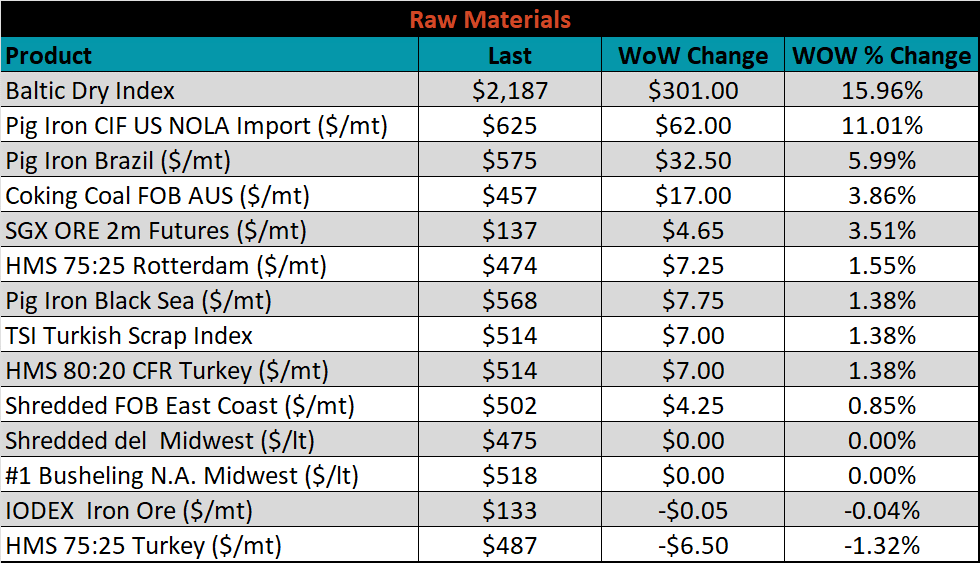

Raw material prices were mostly higher. The group was led by NOLA imported pig iron, up another 11%, while Turkish 75:25 HMS was down 1.3%. The Russian invasion into Ukraine is a significant driver of this space because much of the raw materials used to make steel are mined or produced in the CIS. Any prolonged engagement will likely lead to significant disruptions and even higher prices.

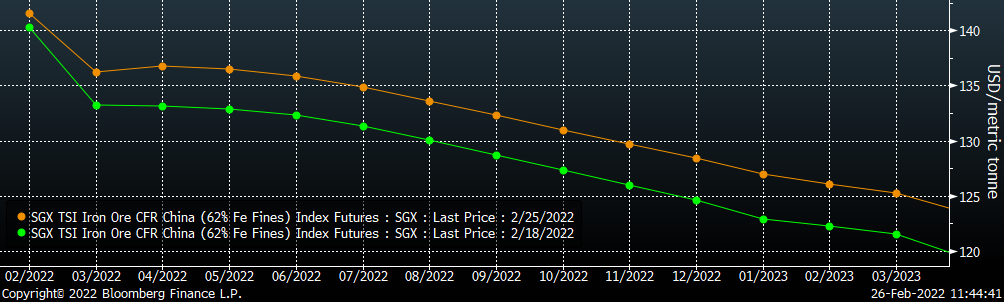

Below is the iron ore future curve with Friday’s settlements in orange, and the prior week’s settlements in green. Last week, the entire curve shifted higher, most significant in later expirations.

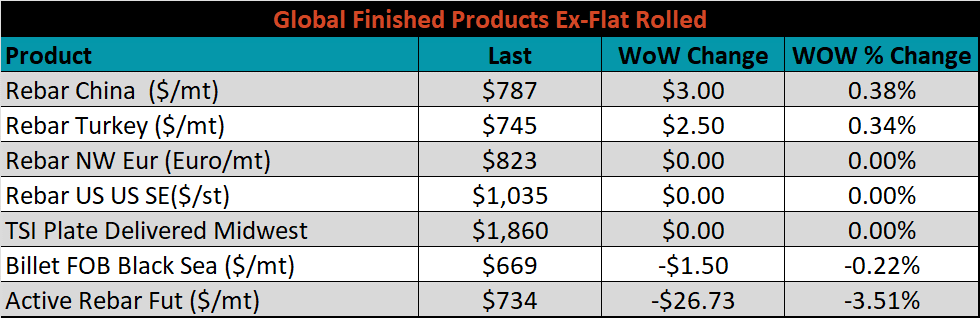

The ex-flat rolled prices are listed below.

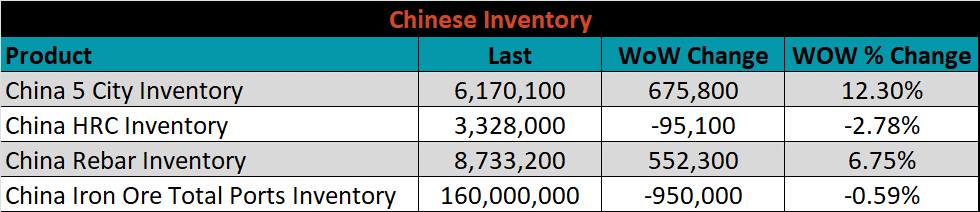

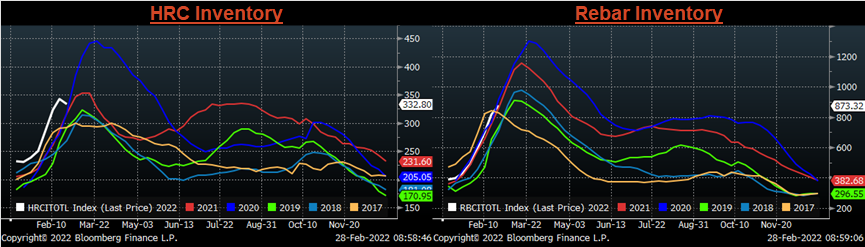

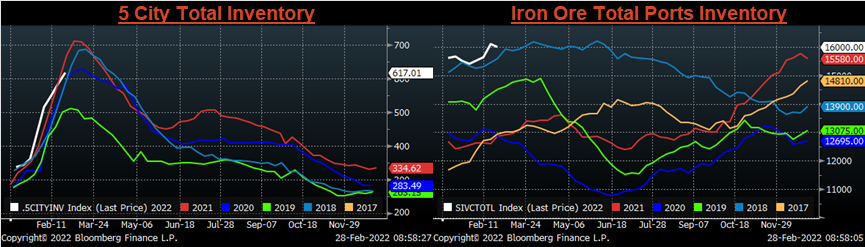

Below are inventory levels for Chinese finished steel products and iron ore. The rebar, and 5-city inventory levels increased again this week, while HRC inventory was lower, if this is the end of the seasonal build in HRC inventories, it would be just shy of last year’s peak and well below 2020 levels. The iron ore ports inventory was also down slightly.

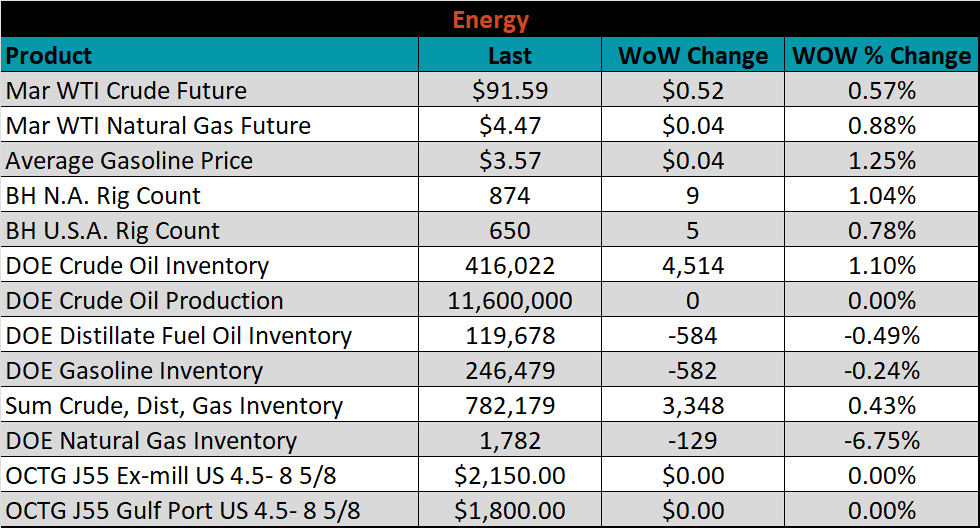

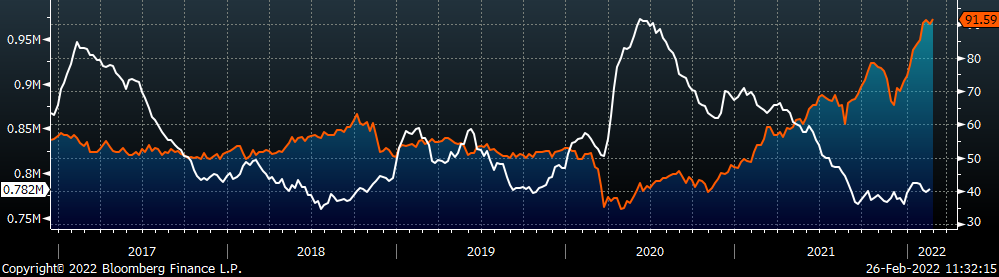

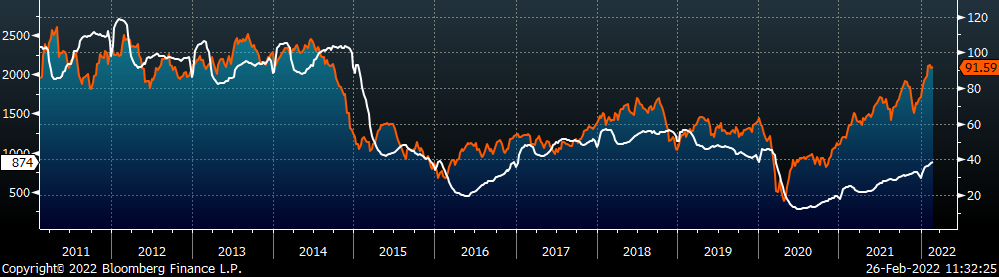

Last week, the March WTI crude oil future gained $0.52 or 0.6% to $91.59/bbl. The aggregate inventory level was up 0.4%, while crude oil production remains at 11.6m bbl/day. The Baker Hughes North American rig count was up by another 9 rigs, and the U.S. rig count was up 5 rigs.

The list below details some upside and downside risks relevant to the steel industry. The bolded ones are occurring or highly likely.

Upside Risks:

Downside Risks: