Content

-

Weekly Highlights

- Market Commentary

- ISM PMI

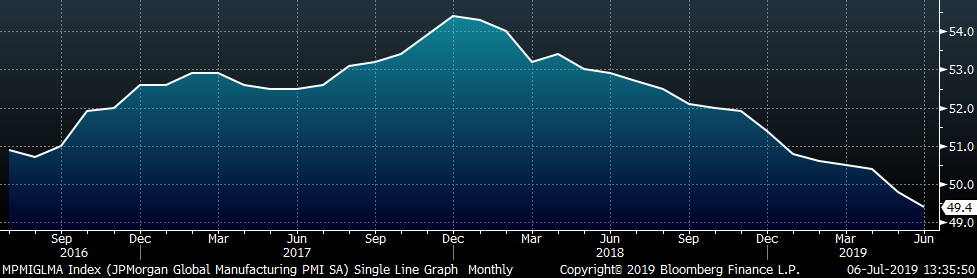

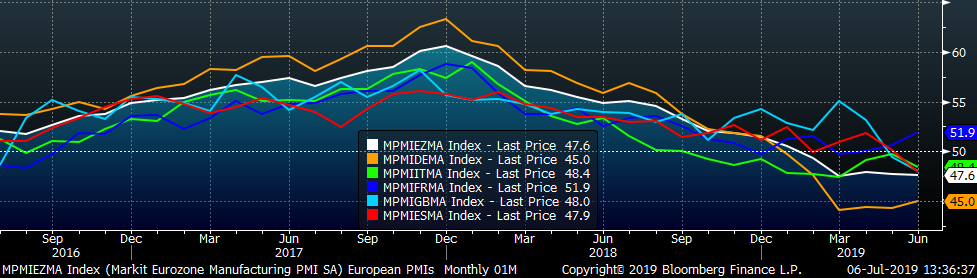

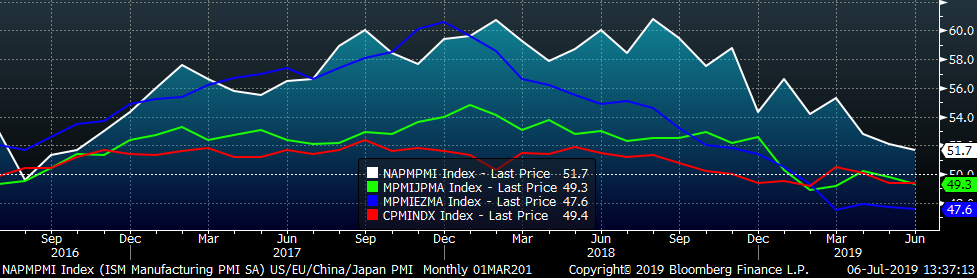

- Global PMI

- Construction Spending

- Auto Sales

- Risks

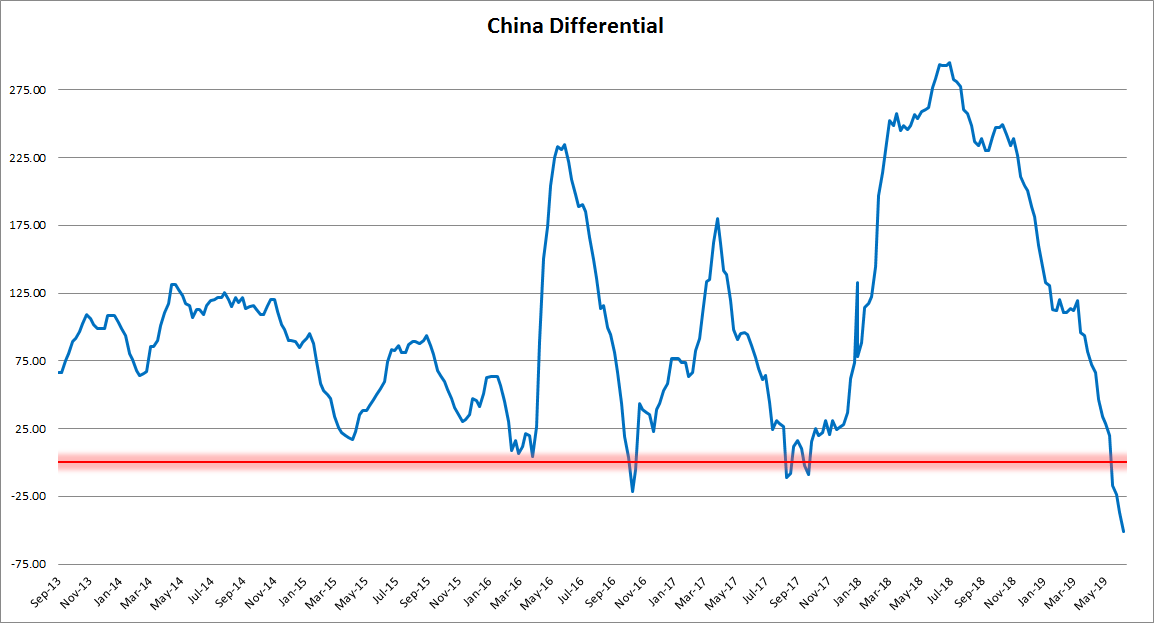

The HRC price has seems to have found a bottom on the back of reduced production and producer price increases. Now the question is “How far can prices rally?” To help us understand the answer, we analyzed the historical price relationship between domestic pricing and the China export price.

Several weeks ago, this report analyzed the differential between the Platts TSI Daily Midwest HRC Index and the Platts China Export price. At that time, May 10th, the differential was near $100, meaning the Midwest price was $100 above the domestically delivered China price, which adds transportations costs to the export price. Since then, the Midwest price had fallen, and the China price has moved slightly higher. This has driven the differential to below negative $50, the lowest level over the past 6 years.

We know this is unsustainable and the relationship between the two prices will eventually revert to normal levels. This means the domestic price will rally, and/or the China price falls. Based on the historical, pre-Section 232, differential average of positive $80, for this relationship to return to it’s average level, domestic price would need to move to approximately $640. The range one standard deviation around this average is $580 to $700. Therefore, we see a $100 to $200 rally in domestic prices from current levels as likely based on this relationship.

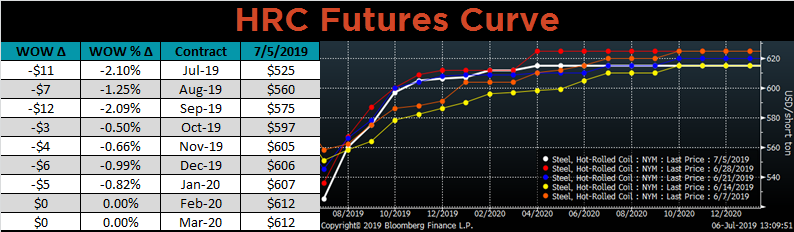

The futures curve remains in steep contango, meaning forward prices are significantly higher than current spot market prices. Therefore, the curve offers no advantage to purchasers looking to lock in tonnage for the future. The best way to get ahead of this rally and benefit from this relationship reverting to the mean is to buy spot material now.

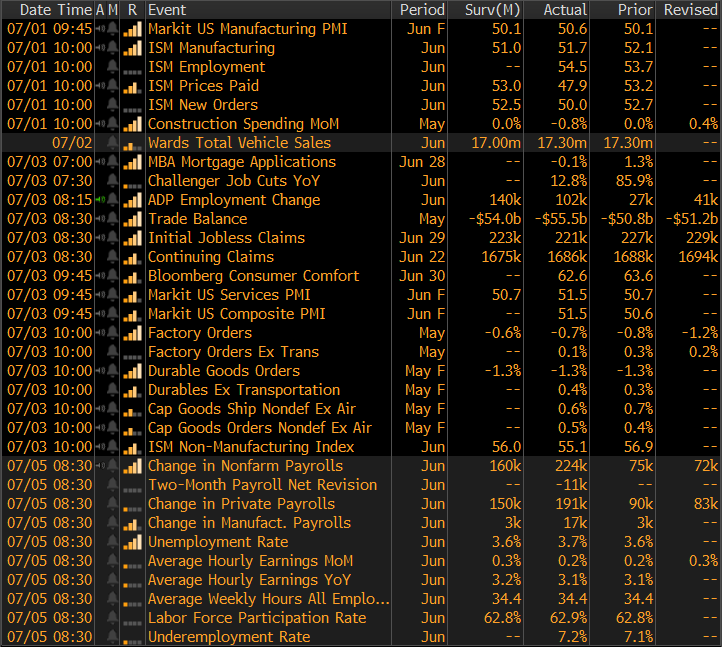

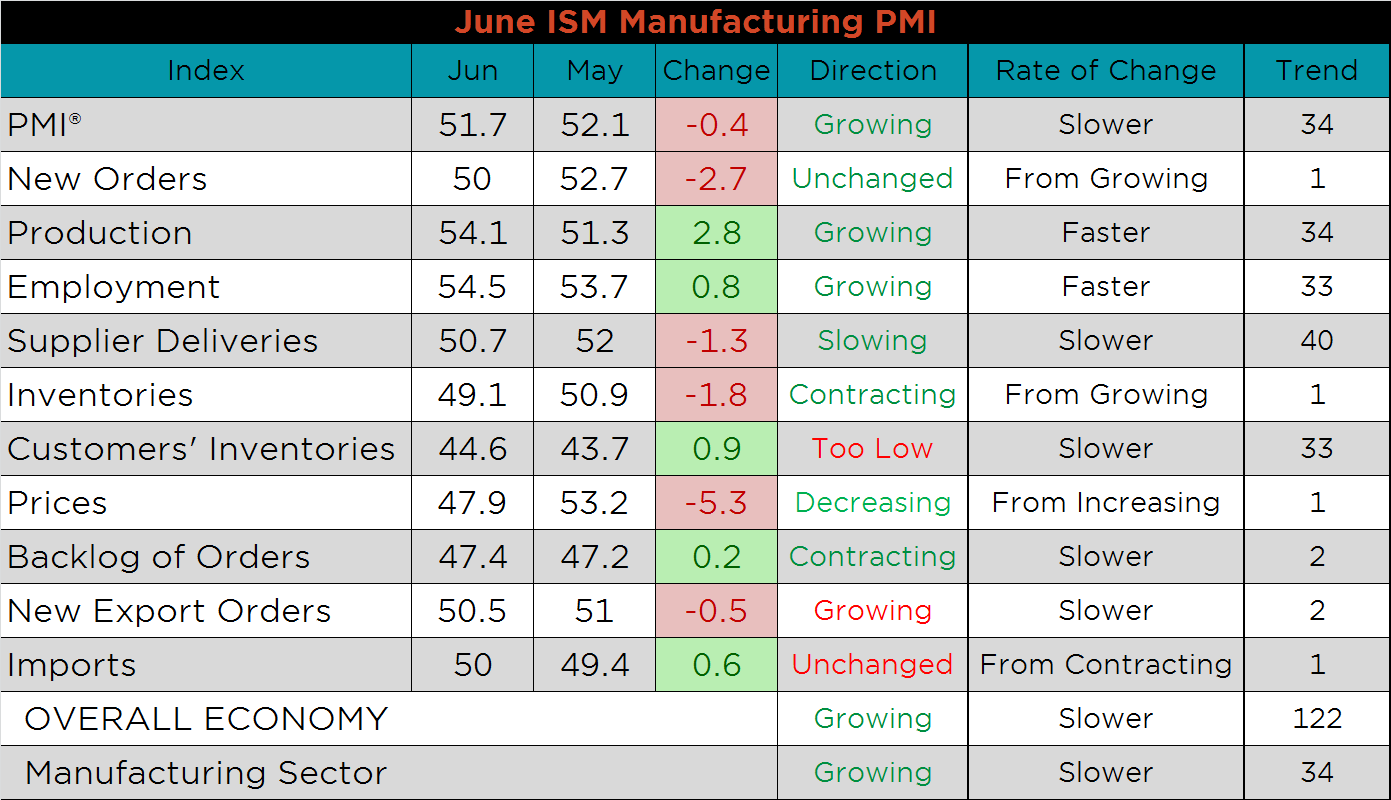

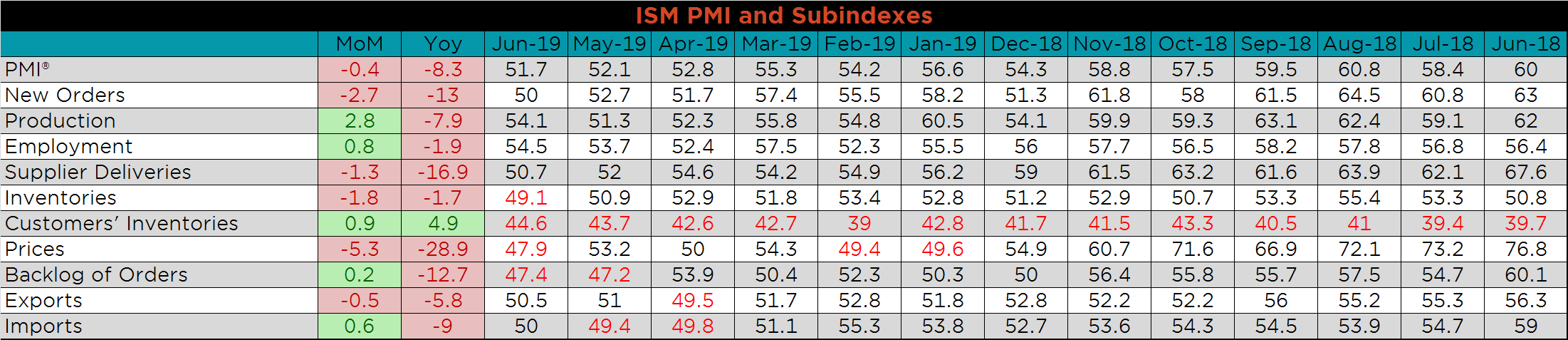

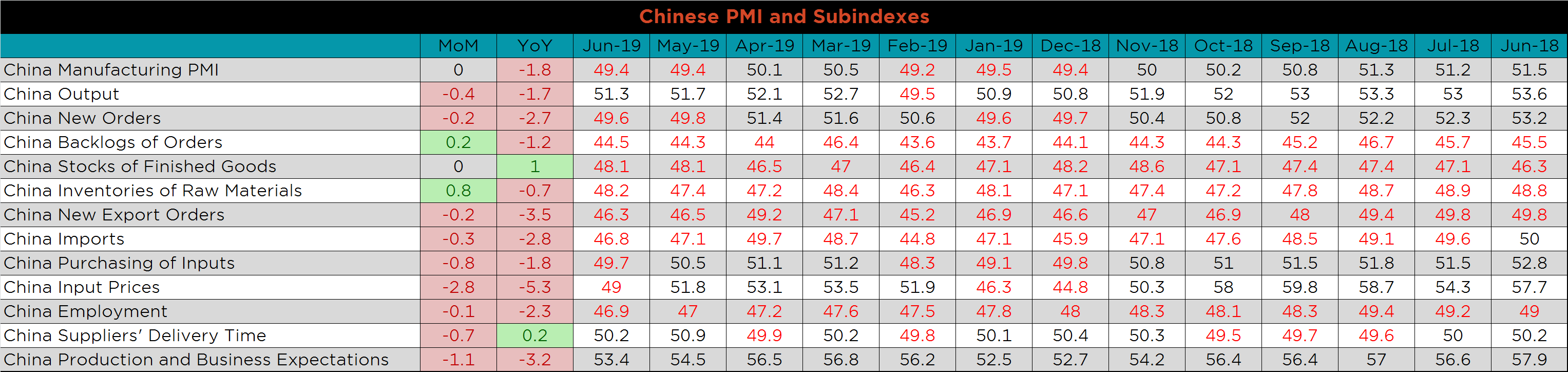

The June ISM Manufacturing PMI and subindexes are below, and it continues to show slower expansion. The new orders, supplier deliveries, inventories, prices and new export orders all decreased, while production, employment, customers’ inventories backlog of orders and imports increased from May.

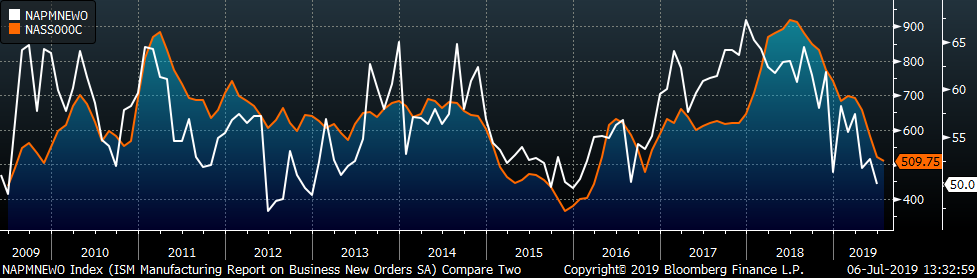

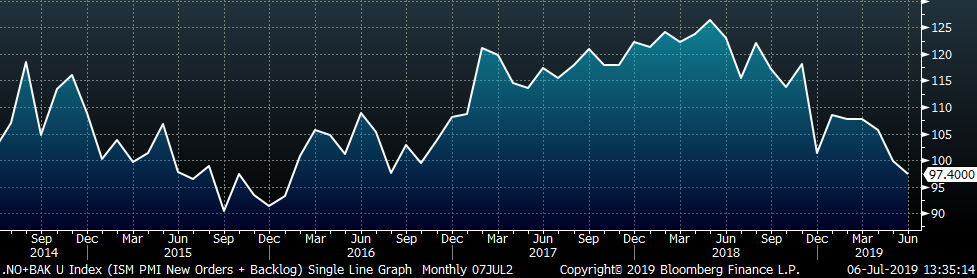

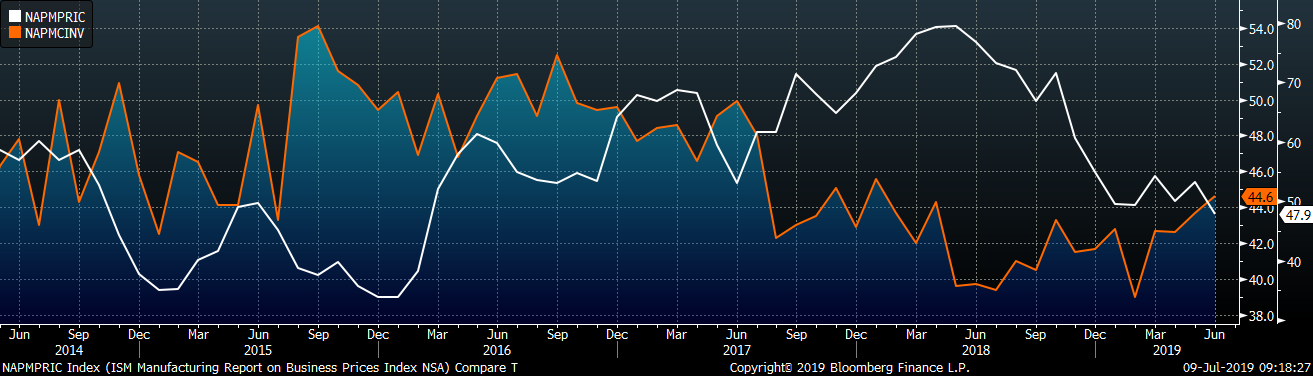

The chart below compares the ISM new orders subindex with the Platts TSI Daily Midwest HRC Index. The subindex had its lowest printing since the end of 2015. The second chart adds the new orders and backlog subindexes, showing the decline in apparent demand since last summer. The third chart shows the prices subindex and the customer inventories. Low prices alongside extremely low producer and customer inventory levels should encourage restocking across the manufacturing sector.

The below tables show the monthly ISM PMI, subindexes and regional reports back to June 2018, providing an expanded view of the manufacturing industry. June printings were weak across the board compared to exceptionally high printings from 2018.

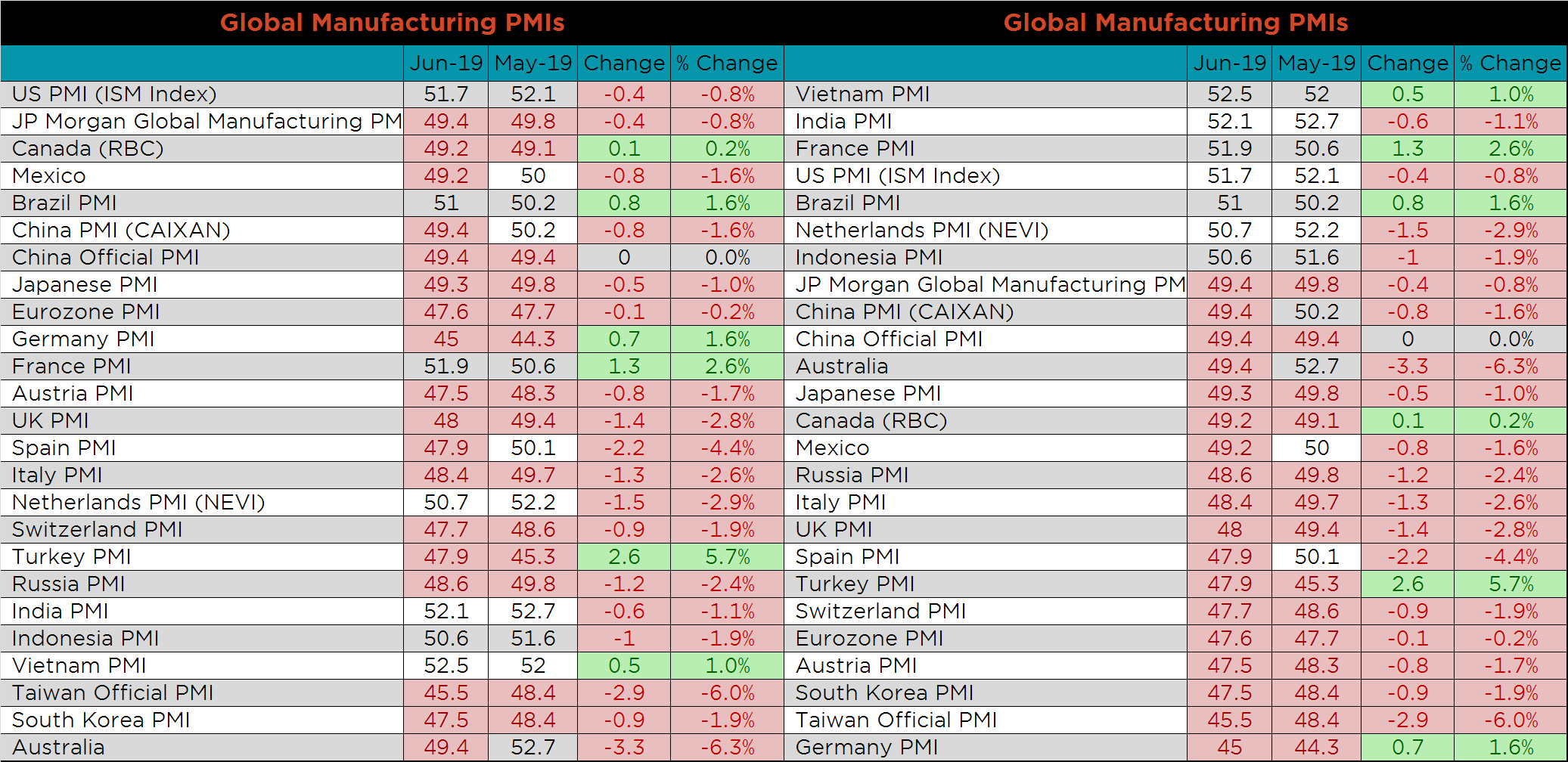

The U.S. manufacturing PMI remains among the strongest in the world, only printing behind Vietnam, India and France, while the Chinese Caixan, Australian, Mexican and Spanish PMI’s fell into contraction. France is now the only European country remaining in expansionary territory, and Germany continues with lowest PMI globally at 45. The PMIs of Europe, Japan and the U.S. all moved lower, while China’s official PMI did not change. Eighteen of the global PMI’s below are currently in contraction.

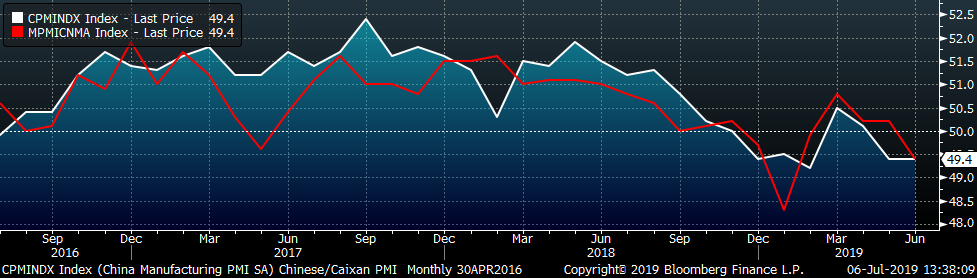

China’s official PMI and Caixan Manufacturing PMIs both printed at 49.4.

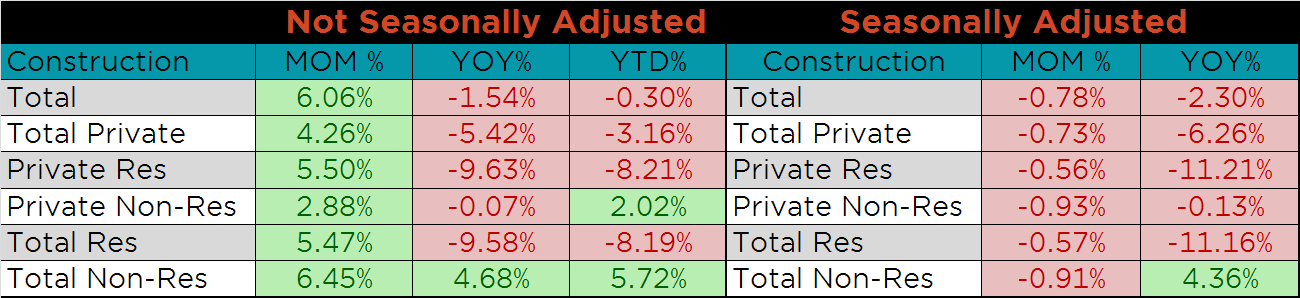

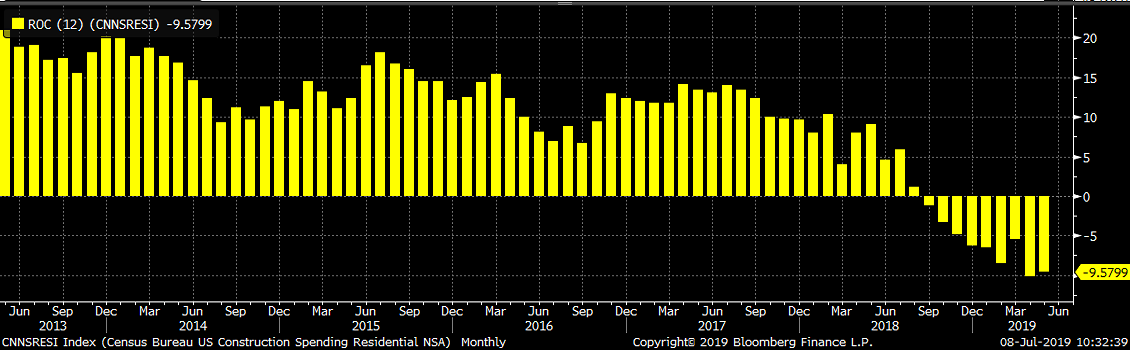

Seasonally adjusted May U.S. construction spending was down MoM and YoY, 0.8% and 2.3%, respectively. Overall weakness in construction spending was primarily driven by weakness in residential construction, down 11.2% compared to May of 2018. Seasonally adjusted non-residential spending was up 4.4% YoY, due to increased public infrastructure spending.

Seasonally adjusted May U.S. construction spending was down MoM and YoY, 0.8% and 2.3%, respectively. Overall weakness in construction spending was primarily driven by weakness in residential construction, down 11.2% compared to May of 2018. Seasonally adjusted non-residential spending was up 4.4% YoY, due to increased public infrastructure spending.

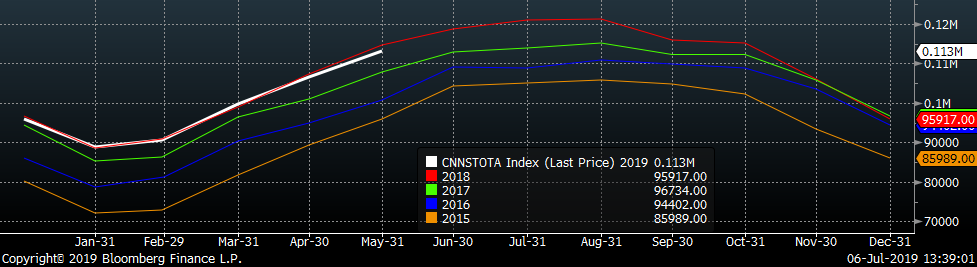

The white line in the chart below represents construction spending in each month of 2019 and compares it to the spending of the previous 4 years.

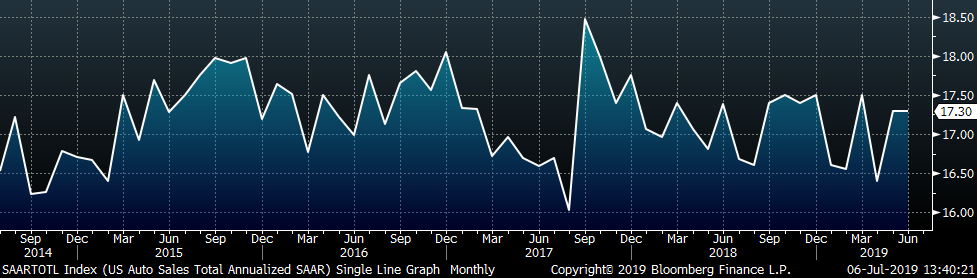

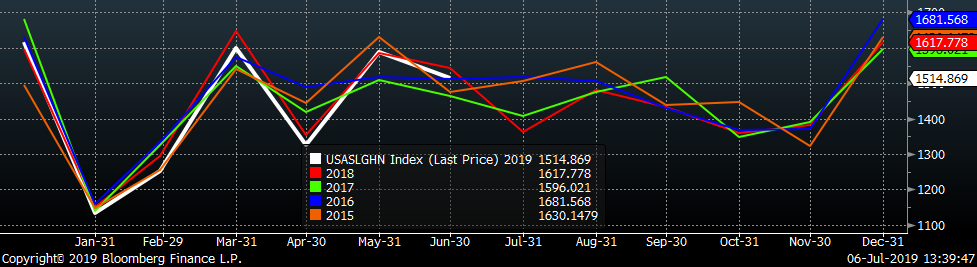

June U.S. light vehicle sales remain at a 17.3m seasonally adjusted annualized rate (S.A.A.R).

The white line in the chart below compares auto sales for the first 6 months of 2019 to the sales of the previous 4 years.

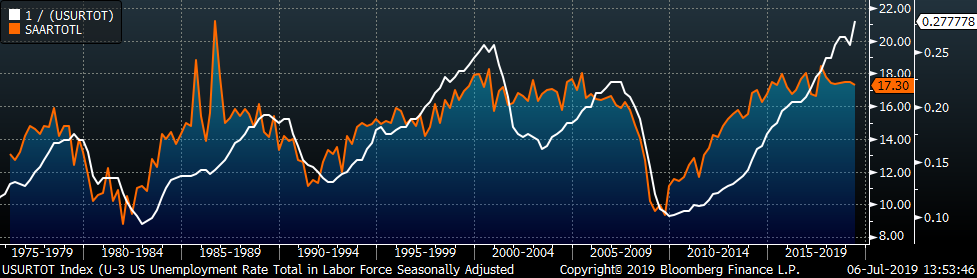

June annualized auto sales continued lower while the U.S. unemployment rate fell to 3.6%. Here the unemployment rate is inverted to show the historical relationship of unemployment auto sales. Annualized auto sales appear to have a plateaued around 18 million, while unemployment is at historically low levels.

Below are the most pertinent upside and downside price risks:

Upside Risks:

Downside Risks:

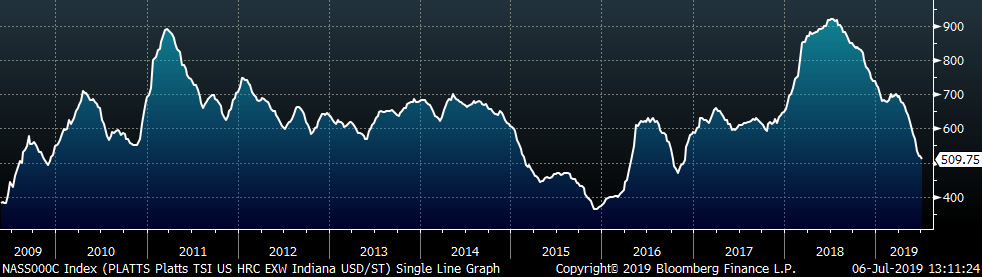

The Platts TSI Daily Midwest HRC Index was down $10.50 to $509.75.

The CME Midwest HRC futures curve is shown below with last Friday’s settlements in white. The curve moved slightly lower in the front.

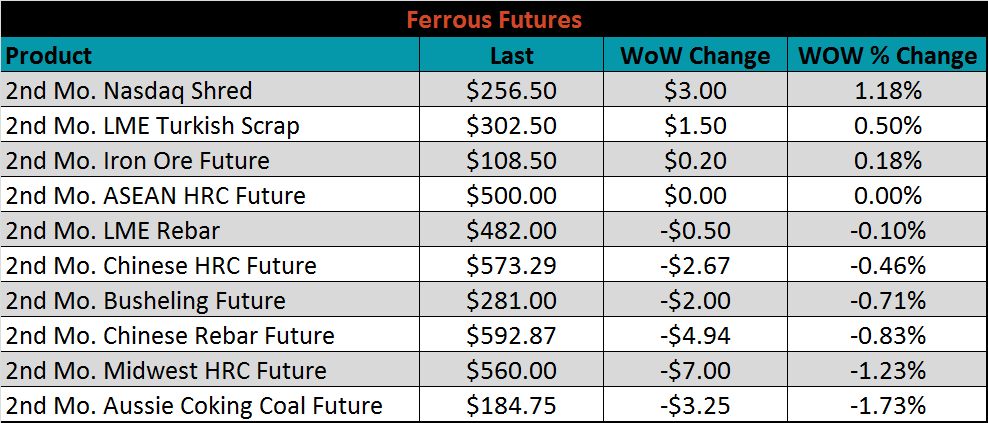

July ferrous futures were mixed. The Nasdaq shred future gained 1.2%, while coking coal lost 1.7%.

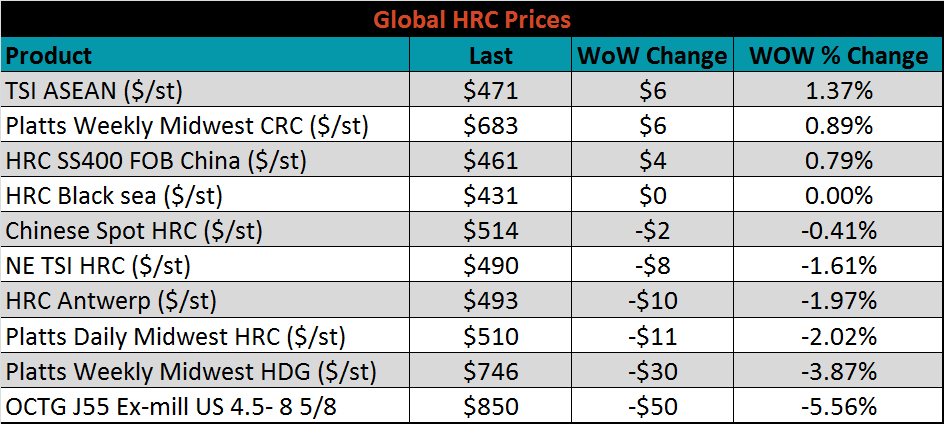

The global flat rolled indexes were mixed. Chinese export HRC was up 0.8%, while Platts Midwest HDG index was down 3.9%.

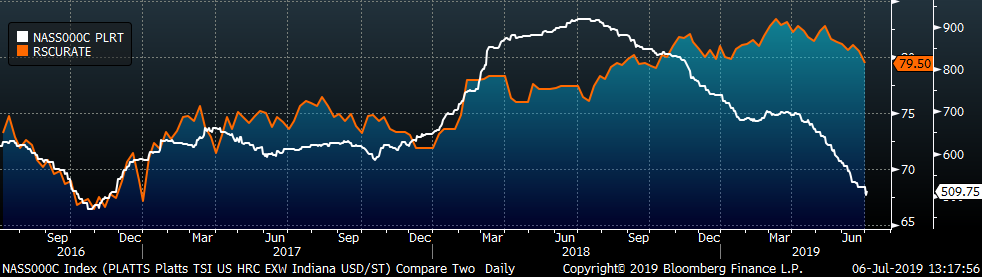

The AISI Capacity Utilization Rate was down 10 points to 79.5%. This is the first time the Capacity Utilization Rate set by the Trump administration has not held since October 2018.

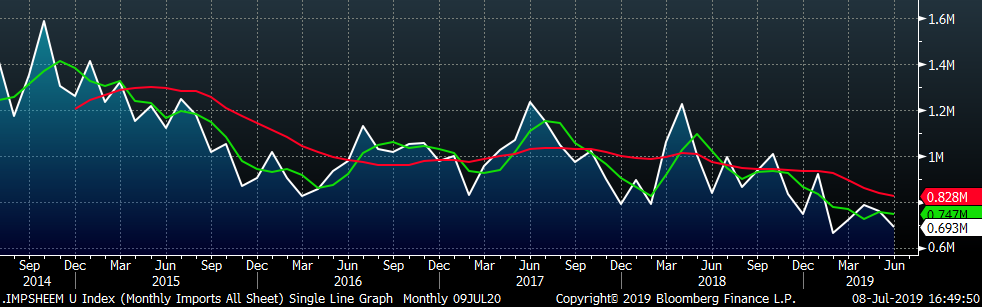

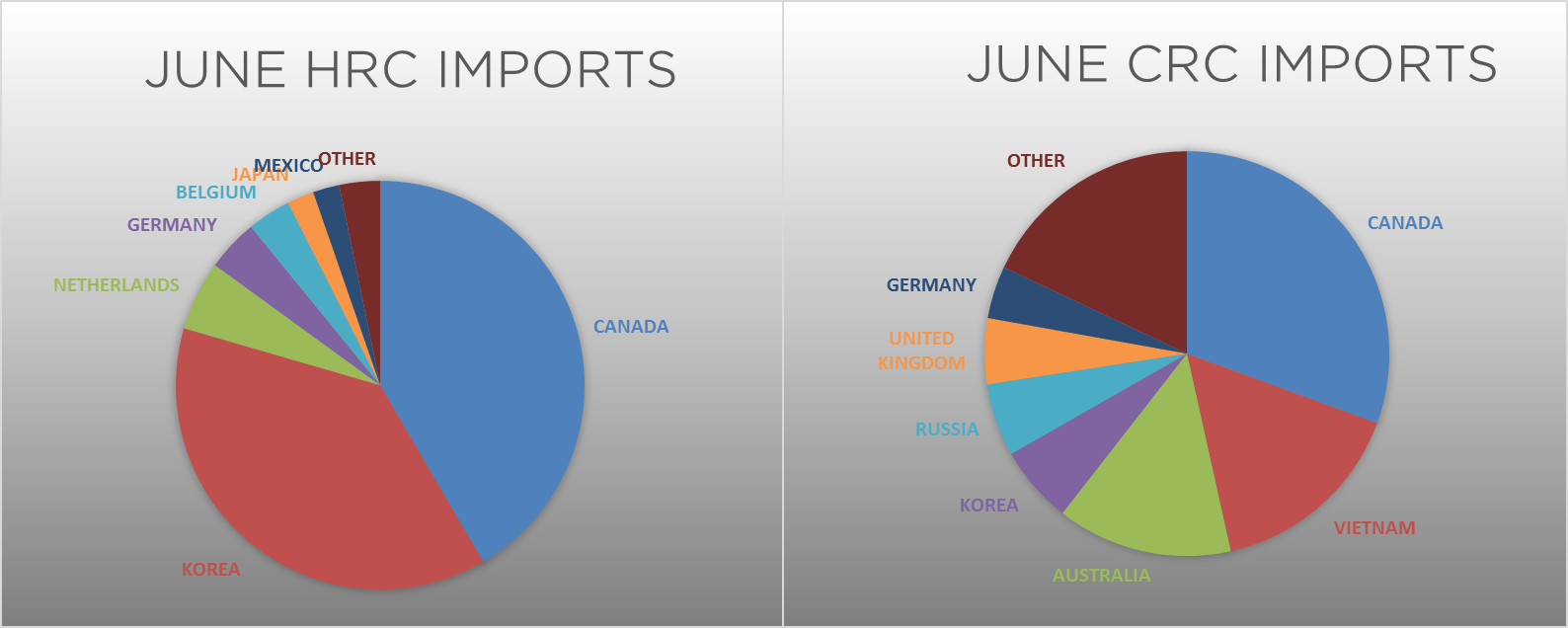

June flat rolled import license data is forecasting a decrease to 793k, down 49k MoM.

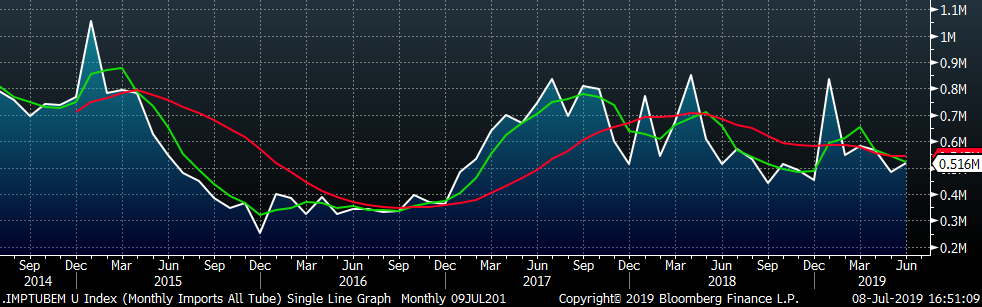

June tube import license data is forecasting a MoM increase of 21k to 516k tons.

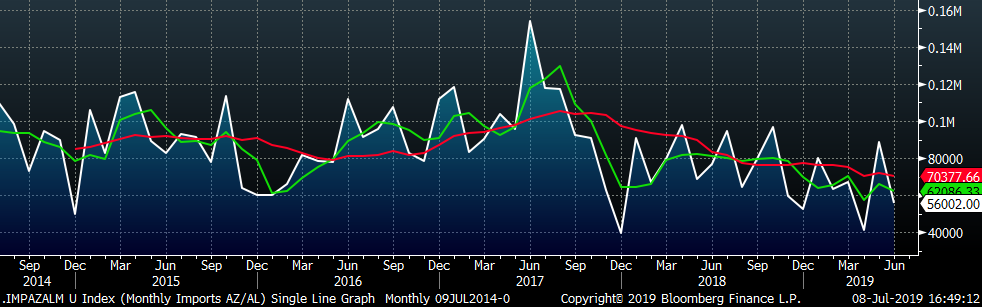

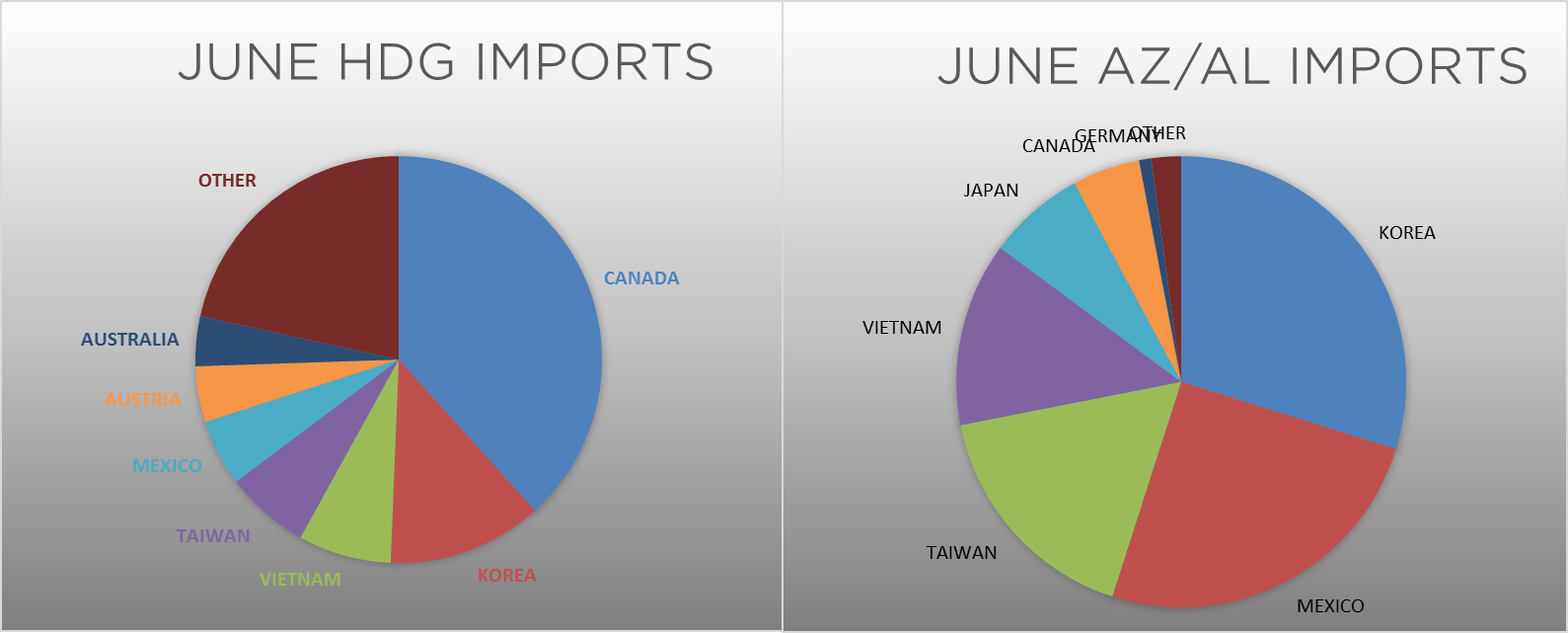

AZ/AL import licenses forecast a decrease of 27k MoM to 56k in June.

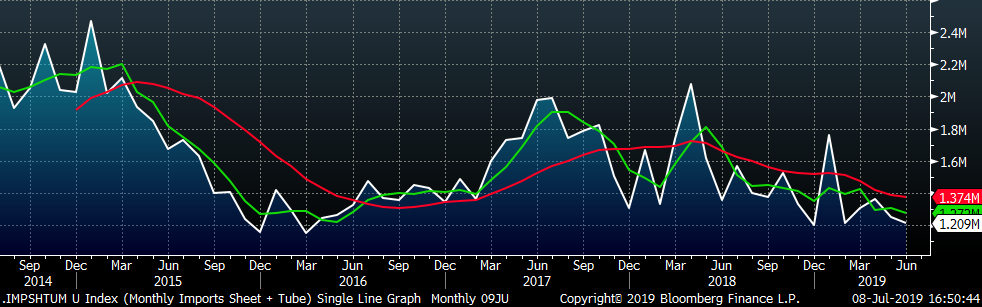

Below is June import license data through July 2, 2019.

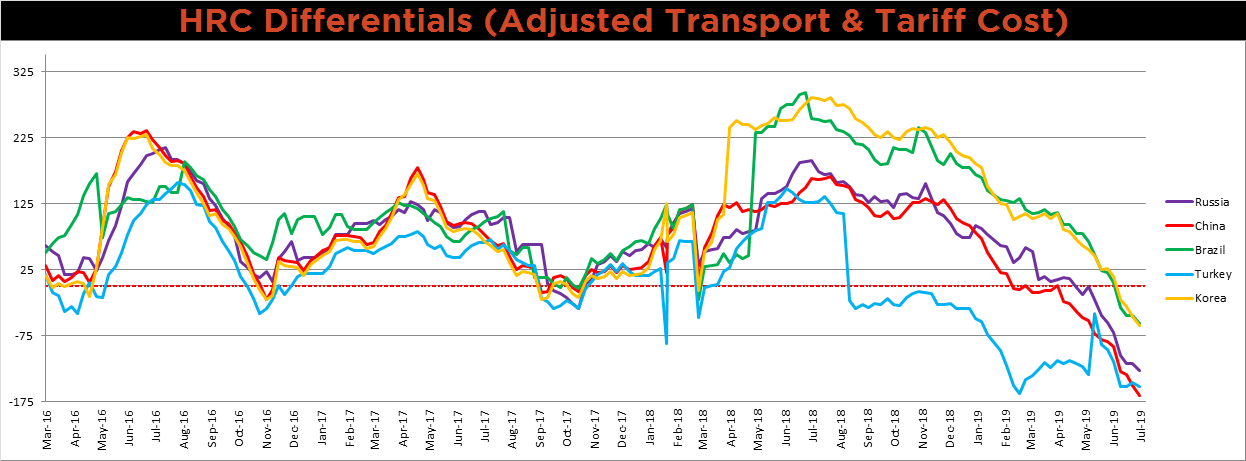

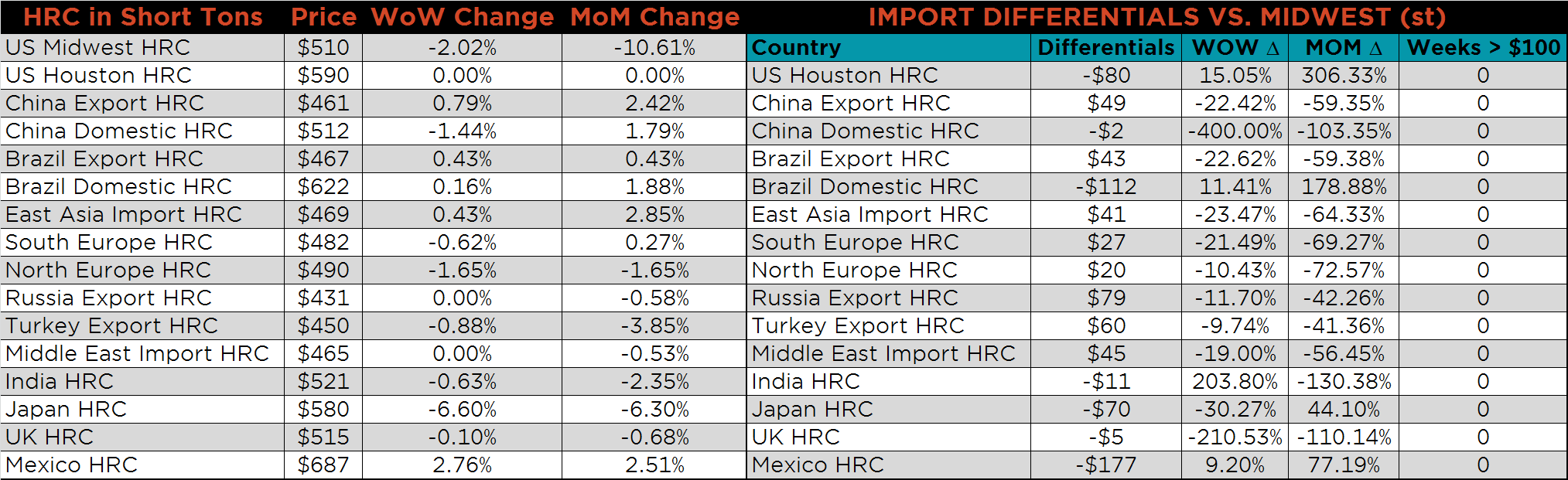

Below is HRC Midwest vs. each listed country’s export price differential using pricing from SBB Platts. We have adjusted each export price to include any tariff or transportation cost to get a comparable delivered price. The differentials were all lower on the week and are at the lowest levels of the last 3 years. Historical data clearly shows that current levels are not sustainable for an extended period, and domestic prices should rise relative to the global price.

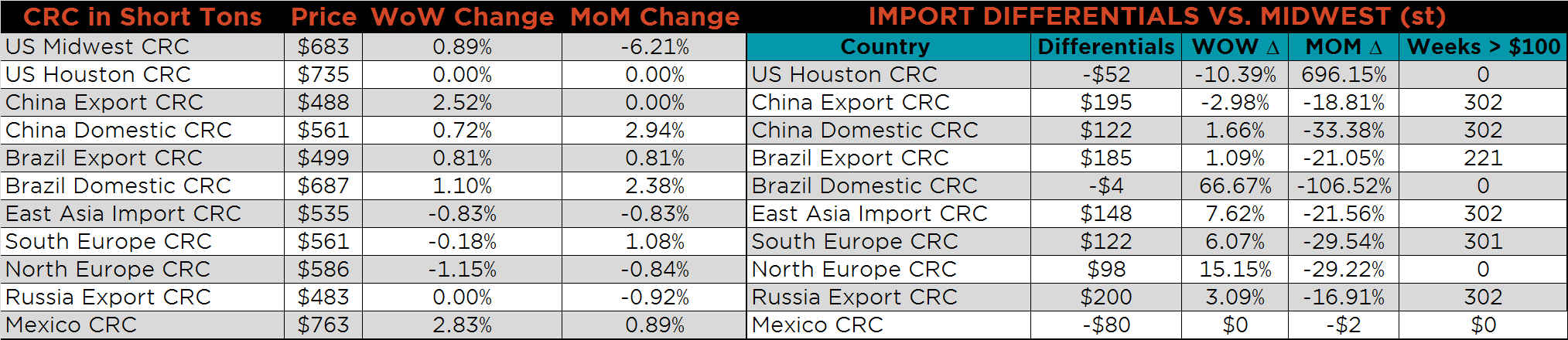

SBB Platt’s HRC, CRC and HDG pricing is below. Midwest CRC was up 0.9%, while HDG and HRC were lower on the week, down 3.9% and 2%, respectively. The Chinese HDG and CRC export prices were up 2.6%, and 2.5%, respectively, while Northern European HRC prices were down 1.7%

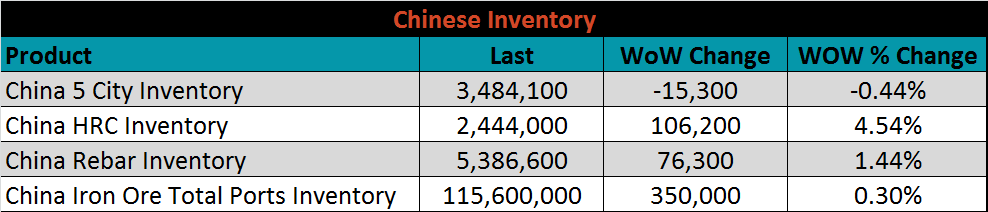

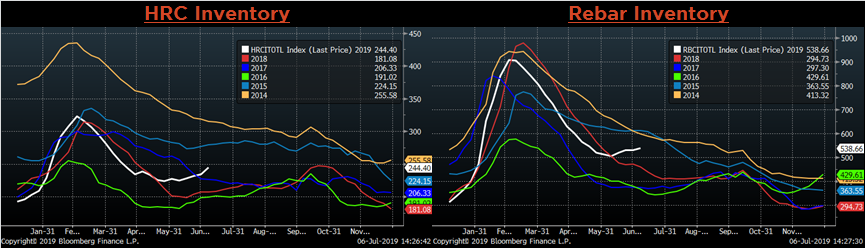

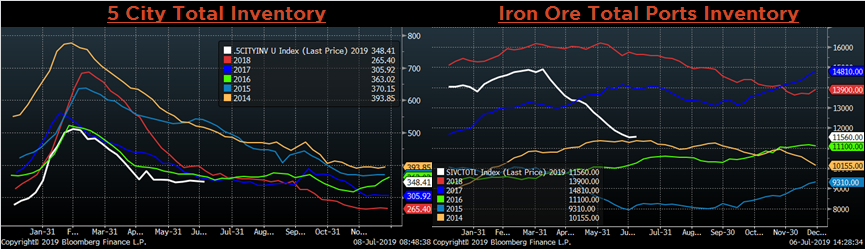

Below are inventory levels for Chinese finished steel products and iron ore. The 5-city inventory decreased on the week, while HRC, rebar and iron ore ports inventory all increased. HRC and rebar inventories have increased over the last few weeks, but prices have remained elevated.

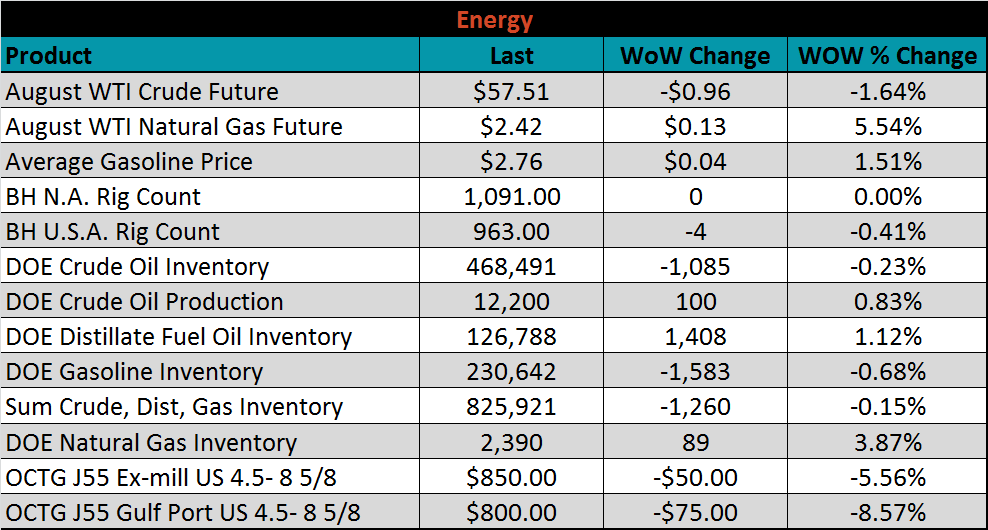

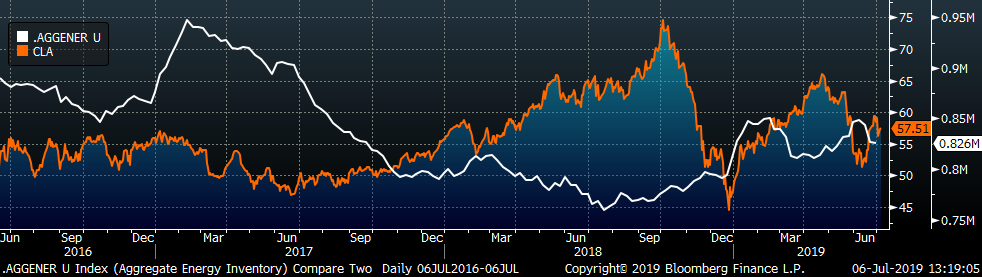

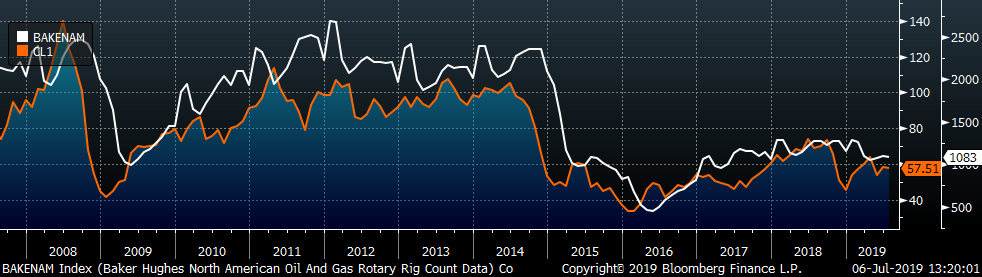

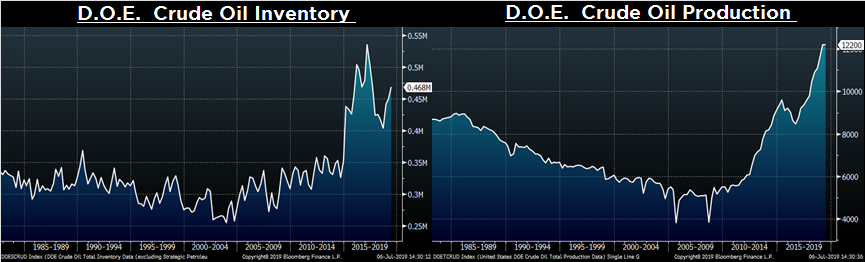

Last week, the Aug WTI crude oil future lost $0.96 or 1.6% to $57.51/bbl. The aggregate inventory level was down 0.2%, and crude oil production rose to 12.2m bbl/day. The Baker Hughes North American rig count gained was unchanged, while the U.S. count lost four rigs.

The list below details some upside and downside risks relevant to the steel industry. The orange ones are occurring or look to be highly likely. The upside risks look to be in control.

Upside Risks:

Downside Risks: