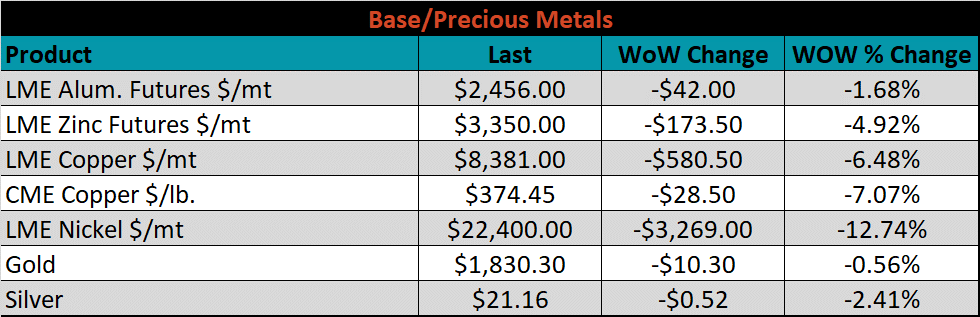

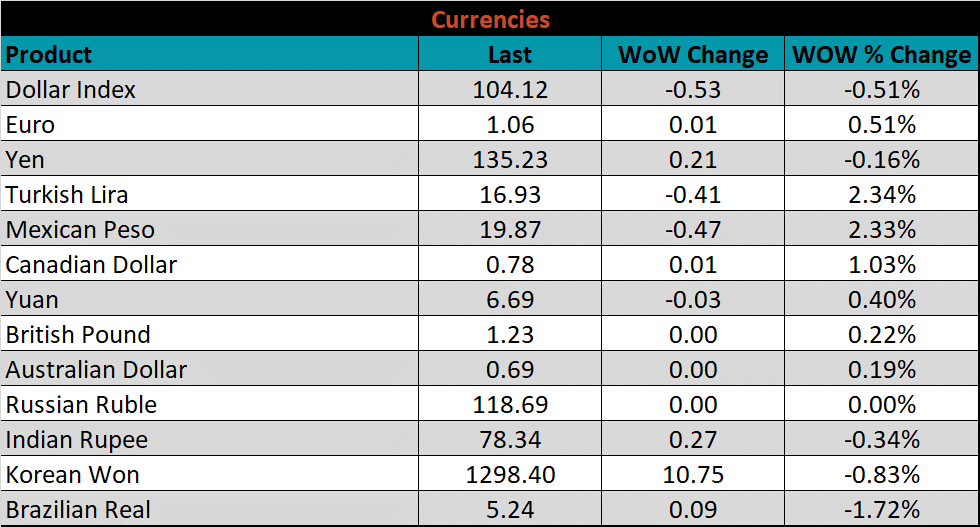

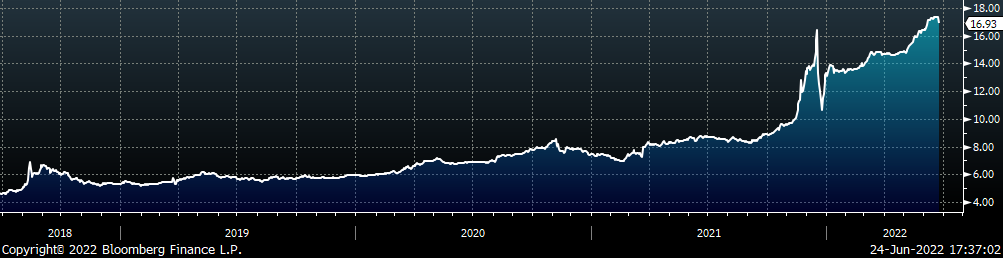

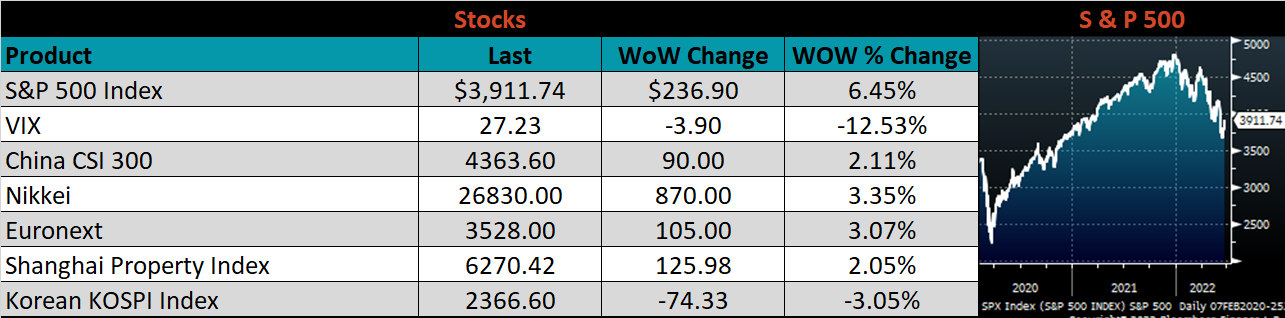

Content

-

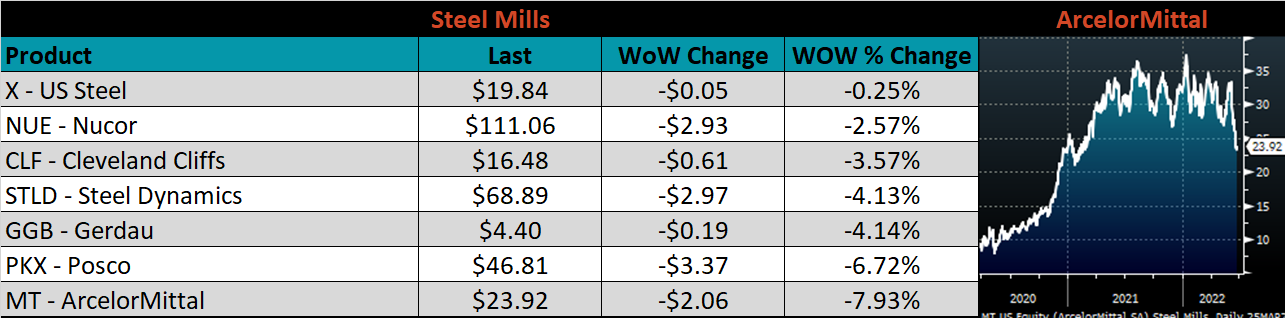

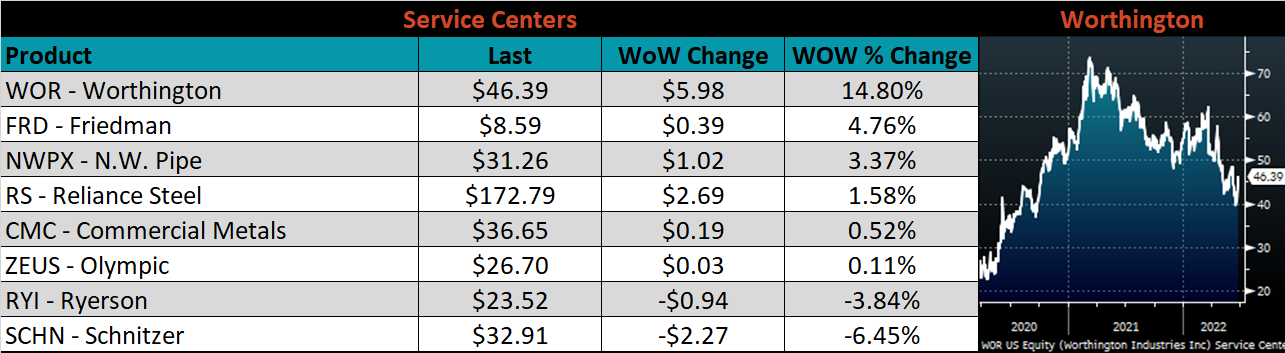

Weekly Highlights

- Market Commentary

- Upside & Downside Risks

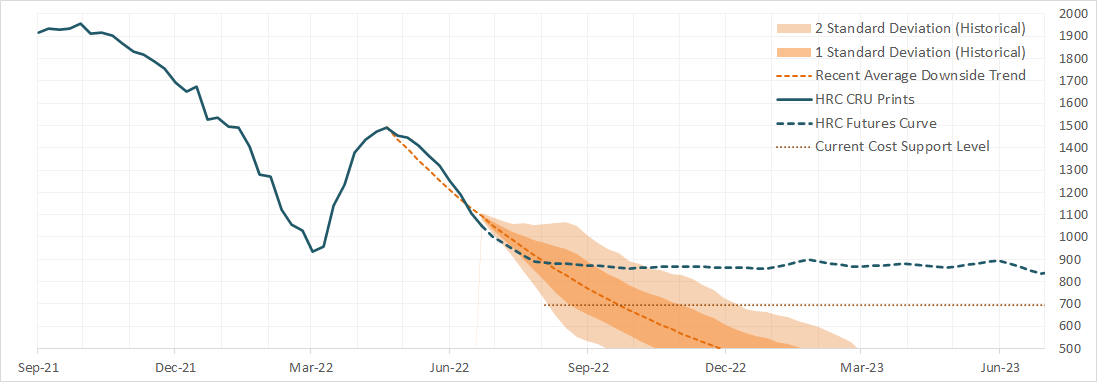

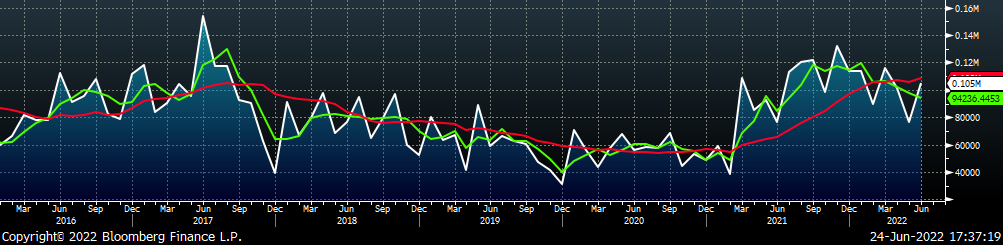

The chart below displays the results of FGM’s statistic backtest study of the recent price trend of US Hot-Rolled Coil. Below are the key takeaways:

Below are the most pertinent upside and downside price risks:

Upside Risks:

Downside Risks:

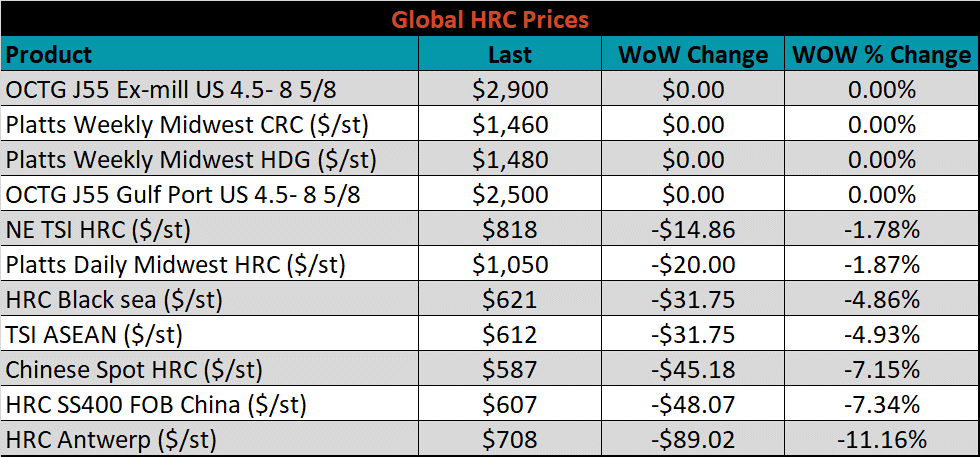

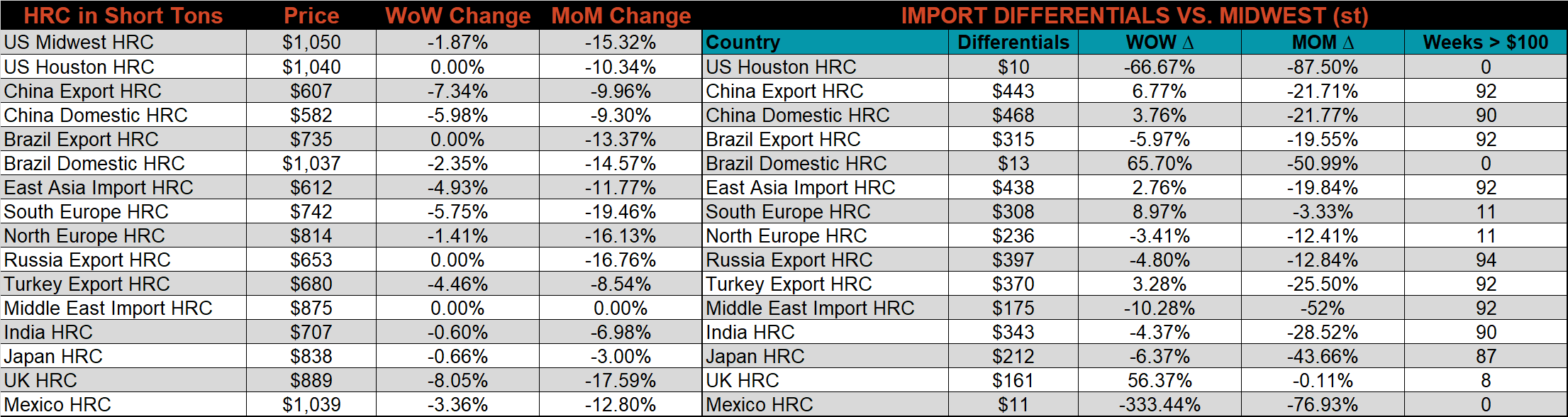

The Platts TSI Daily Midwest HRC Index was down $20 to $1,050.

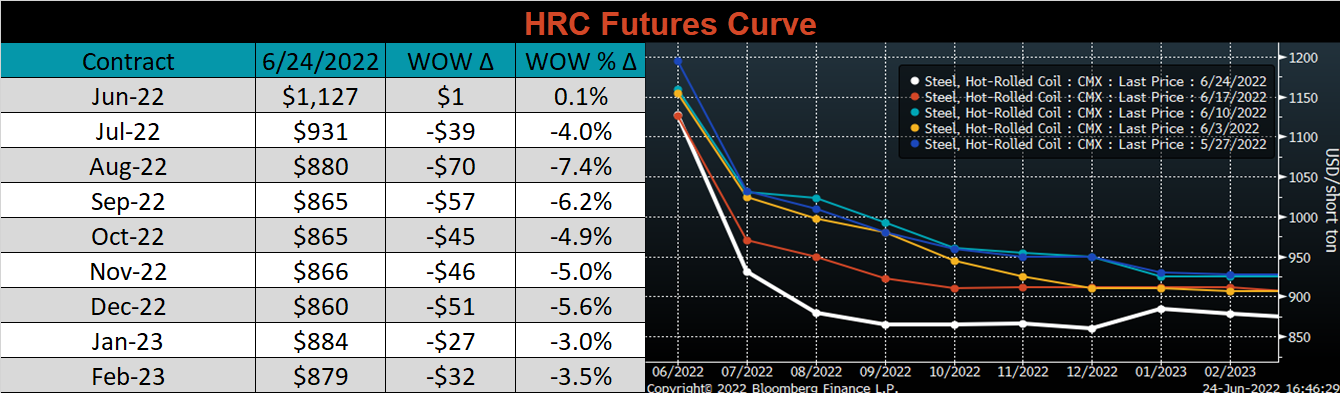

The CME Midwest HRC futures curve is below with last Friday’s settlements in white. The entire curve shifted lower except for the front month, Jun-22 contract. The largest shift down can be observed in the midsection of the curve with a $70 decrease in Aug-22.

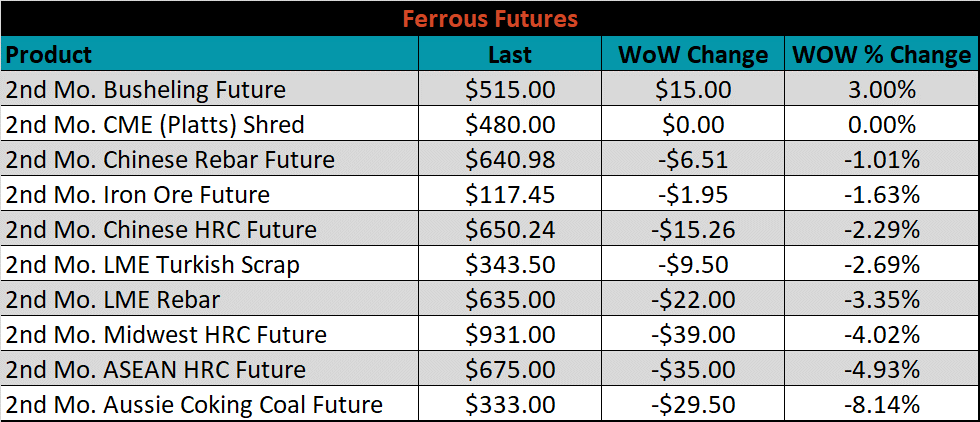

The 2nd month ferrous futures were primarily lower this week. Busheling futures rebounded slightly, up 3.0%, while Aussie Coking Coal fell 8.1%.

Global flat rolled indexes moved lower once again, led by HRC Antwerp, down 11.2%.

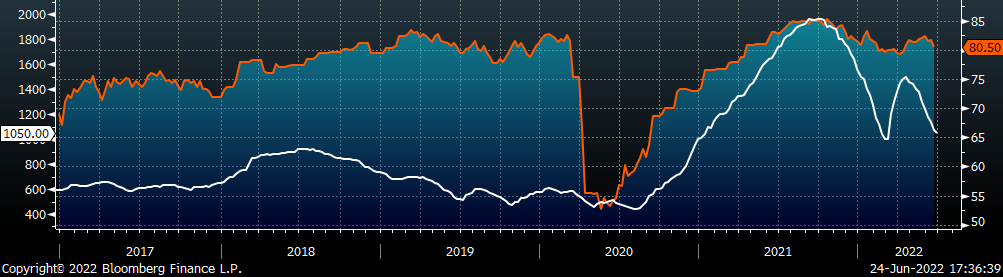

The AISI Capacity Utilization was down 1.2% to 80.5%.

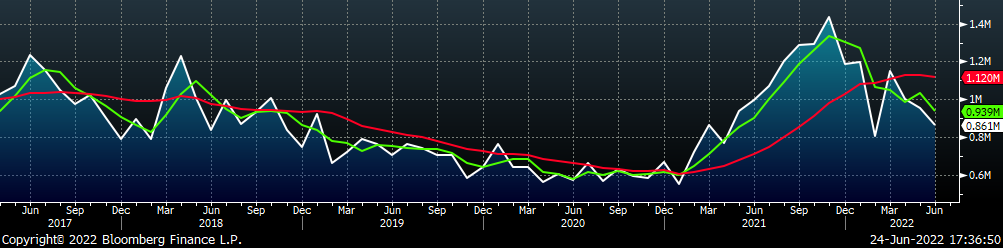

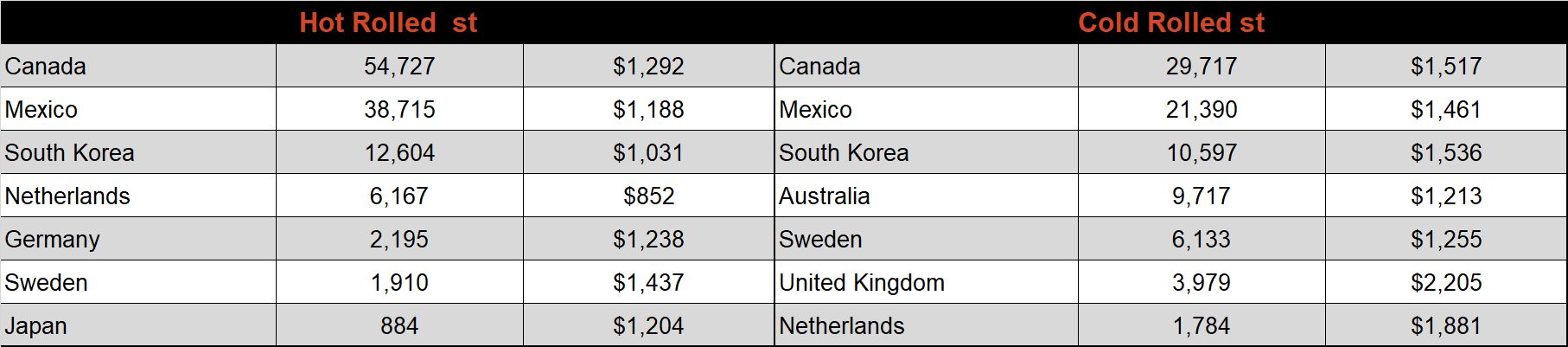

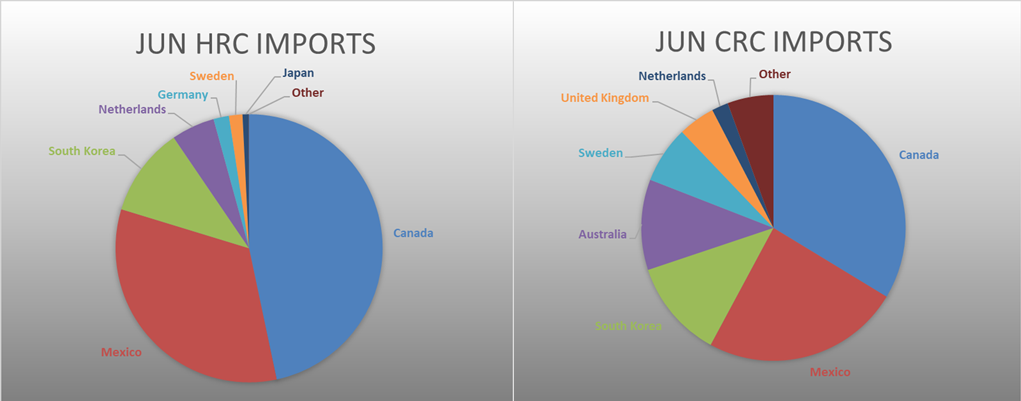

June flat rolled import license data is forecasting a decrease of 35k to 861k MoM.

Tube imports license data is forecasting a decrease of 23k to 541k in June.

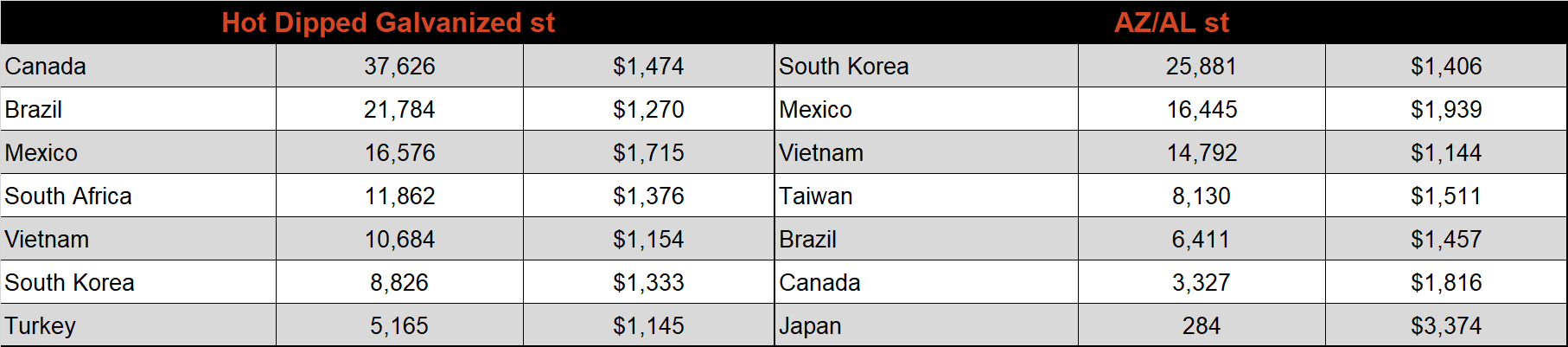

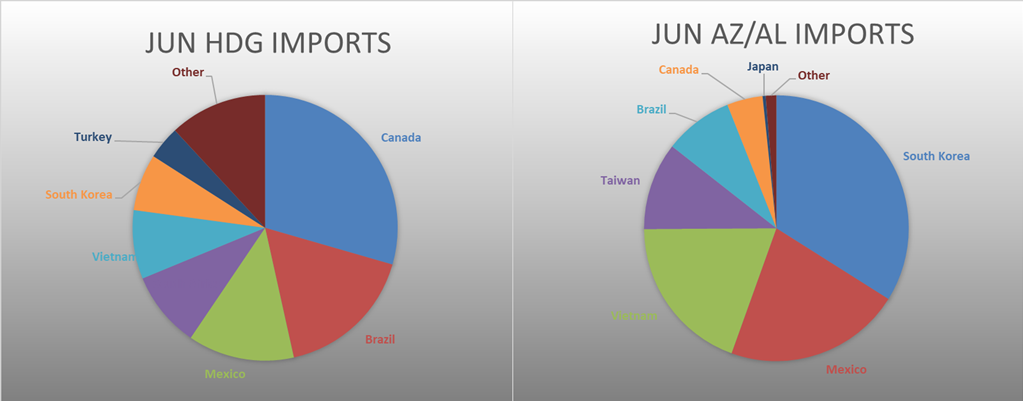

June AZ/AL import license data is forecasting a decrease of 15k to 105k.

Below is June import license data through June 20th, 2022.

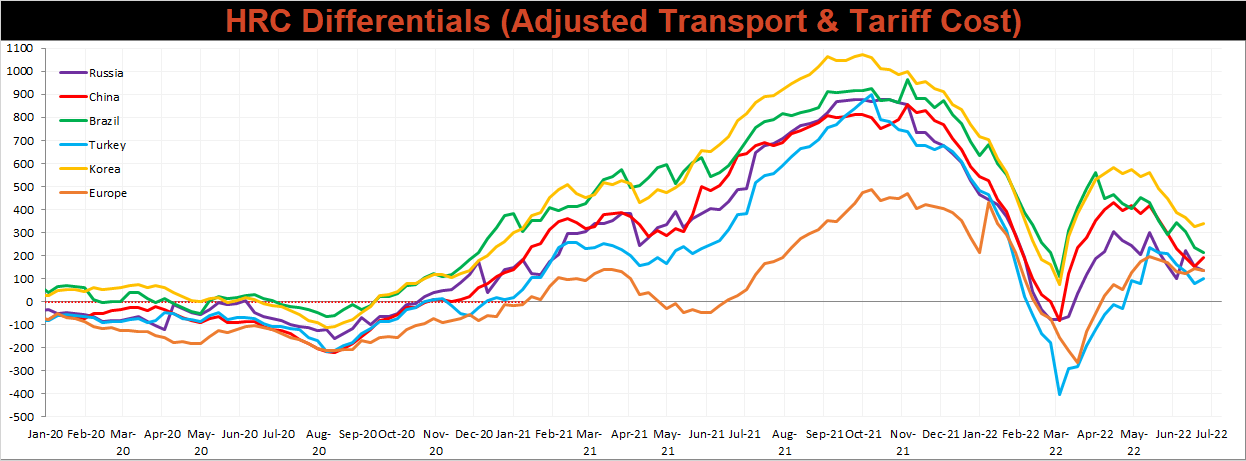

Below is the Midwest HRC price vs. each listed country’s export price using pricing from SBB Platts. We have adjusted each export price to include any tariff or transportation cost to get a comparable delivered price. Differential data was mixed across the board with China increasing 6.77% and Brazil falling 5.97%.

SBB Platt’s HRC, CRC and HDG pricing is below. The Midwest HRC prices were down 1.87%, while CRC and HDG prices were flat. China export HRC price was down the most, falling 7.34% WoW.

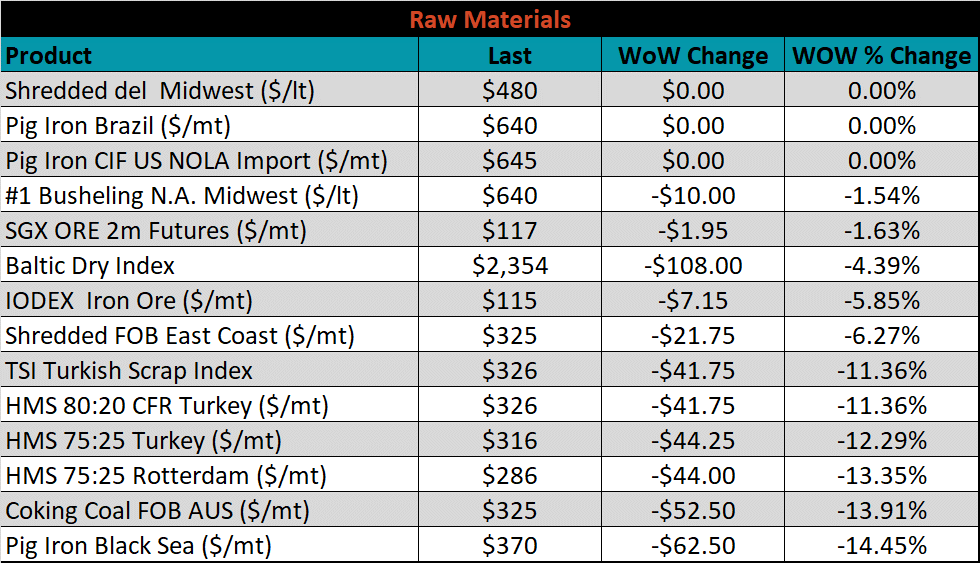

Raw material prices were all lower this week, led by Pig Iron Black Sea, down 14.5%.

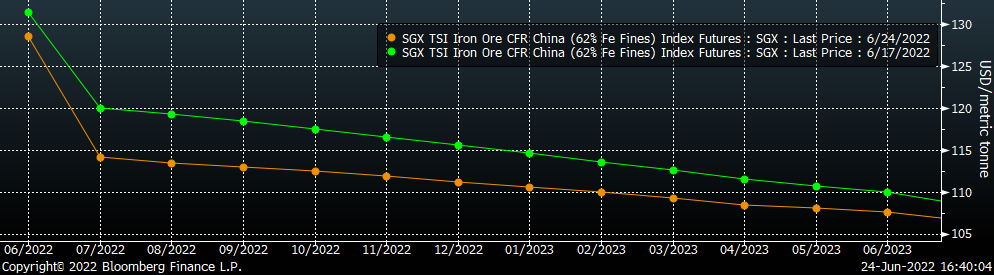

Below is the iron ore future curve with Friday’s settlements in orange, and the prior week’s settlements in green. Last week, the entre curve shifted slightly lower once again.

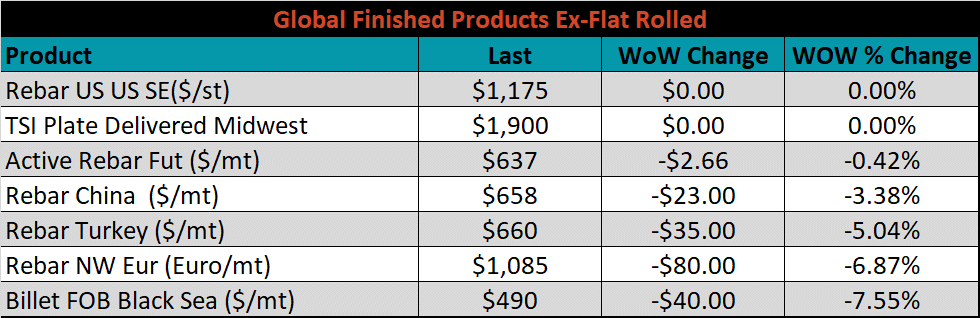

The ex-flat rolled prices are listed below.

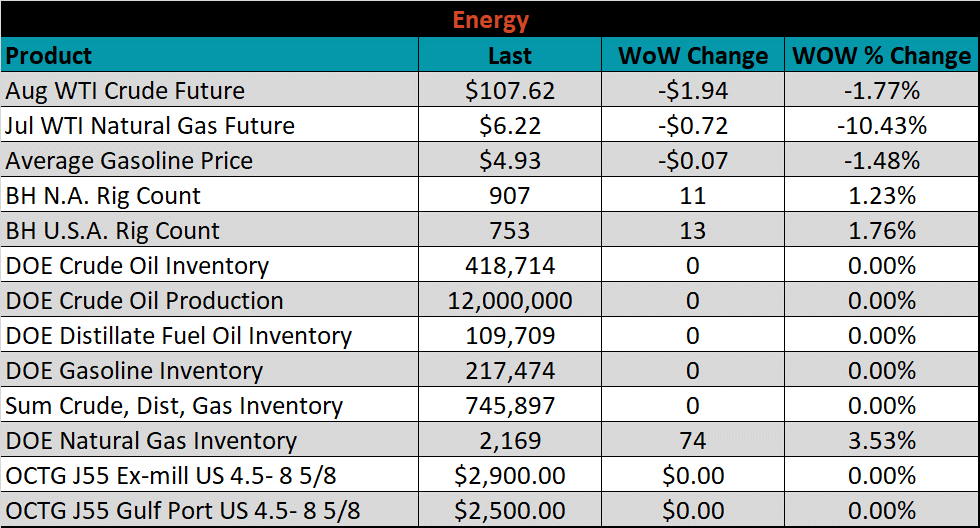

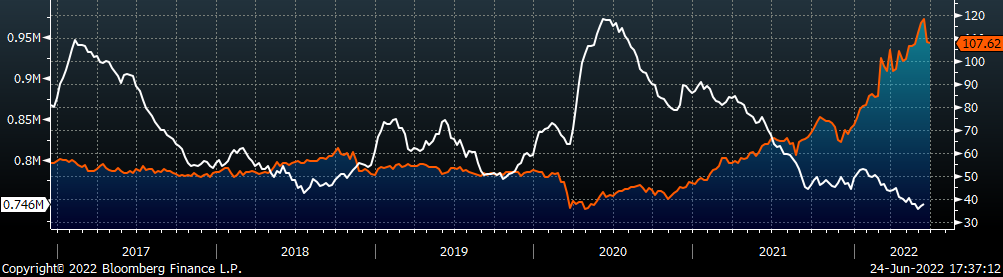

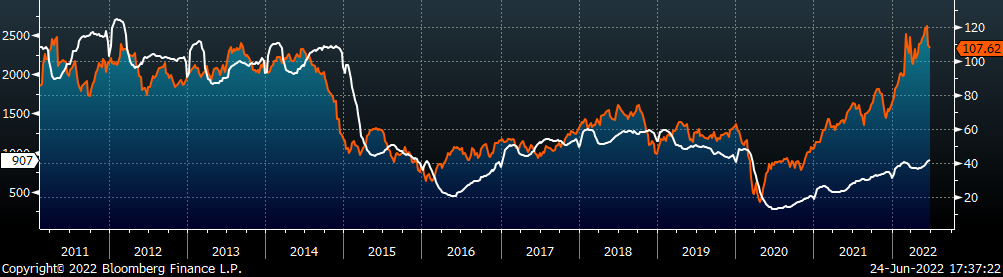

Last week, the August WTI crude oil future lost $1.94 or 1.77% to $107.62/bbl. The aggregate inventory level remained unchanged. The Baker Hughes North American rig count was up 11 rigs, and the U.S. rig count was up 13.

The list below details some upside and downside risks relevant to the steel industry. The bolded ones are occurring or highly likely.

Upside Risks:

Downside Risks: