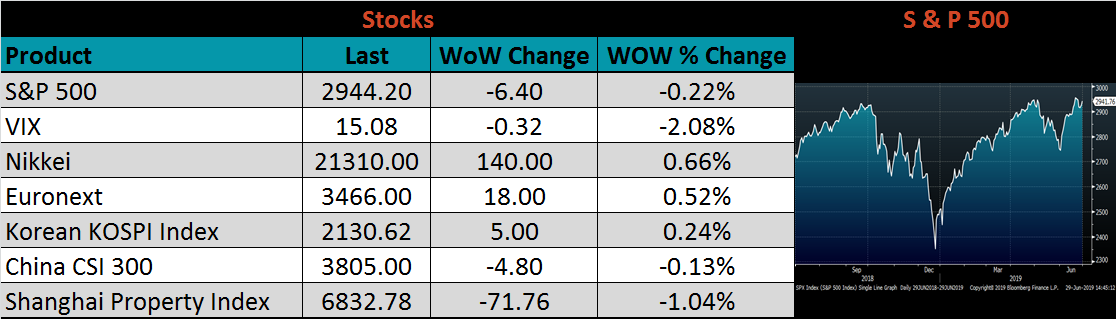

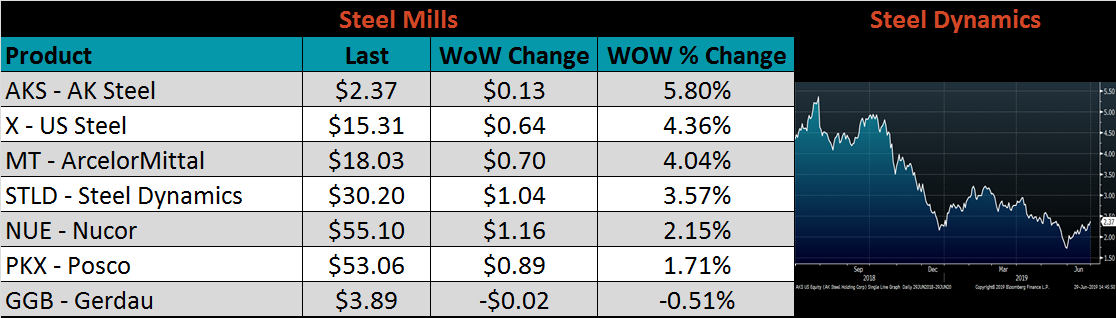

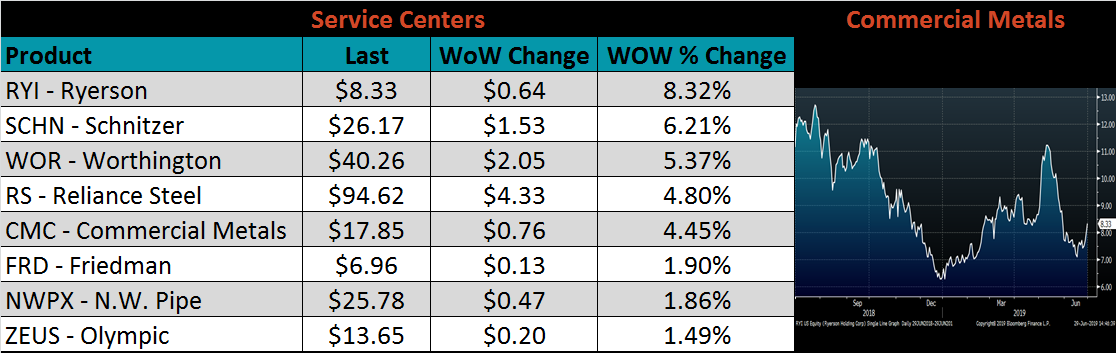

Content

-

Weekly Highlights

- Market Commentary

- Risks

Since last week’s price increase announcements, little has changed in the domestic HRC market. Both the physical market and the forward curve are still trying to digest the implications and effects of the announcements. However, prices in certain related markets saw significant price moves that will influence the direction of the HRC market in the coming weeks and months.

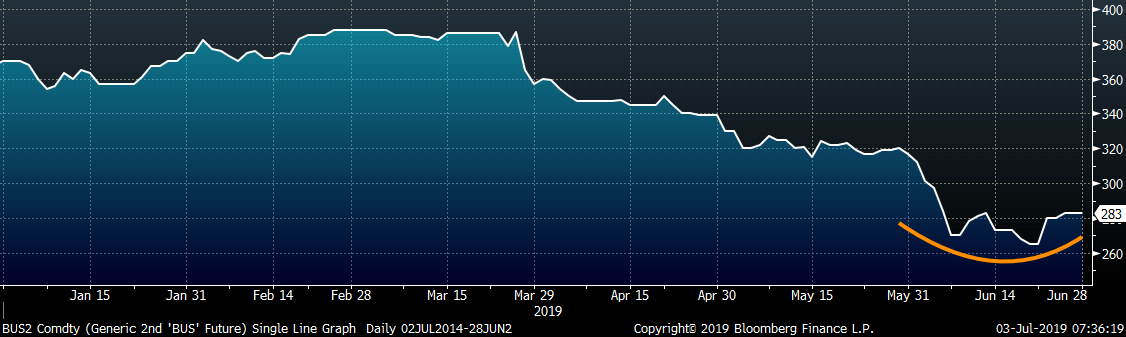

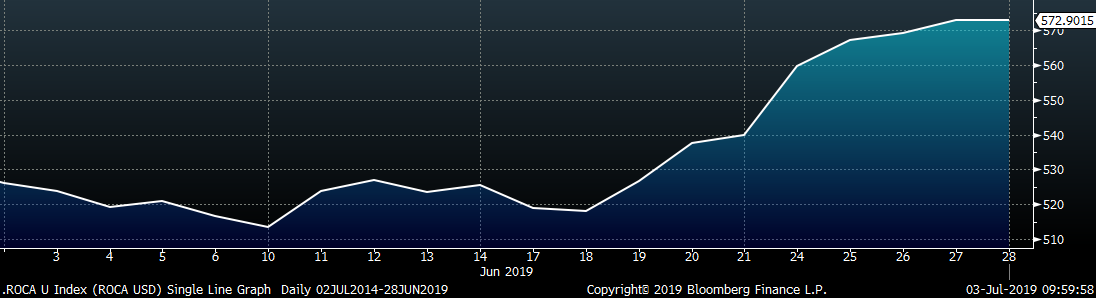

The July scrap market, which two weeks ago many projected to trade down $20 to $30, currently is looking to be down $10 to sideways. This should prevent mini mills from accepting orders at lower prices, raising the bottom of the range of transacted prices. The forward curve for busheling scrap is in contango, just like the HRC curve, implying that the market expects scrap to trade higher in the months ahead. This would support further price increase announces. The chart below shows the rolling 2nd month busheling future contract, which appears to be bottoming.

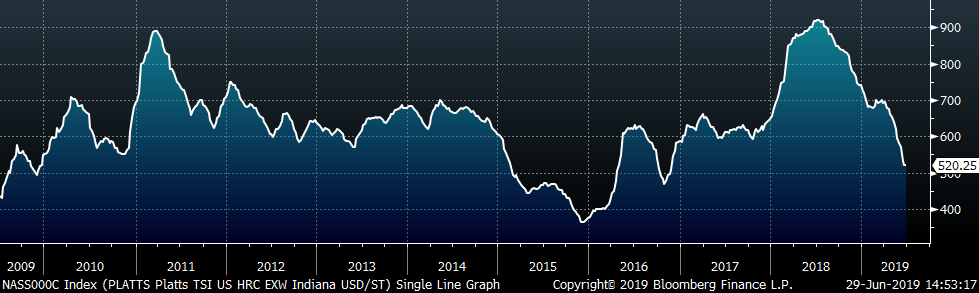

Elevated iron ore prices over the last several months have put pressure on producer profits, especially in China. However, over the last few weeks, HRC prices in China have risen, alleviating this pressure. At FGM, we have been focusing on the China export price, as a proxy for the Southeast Asia price, relative to the domestic price. These prices have been converging, and their relationship is at historically low levels. As the Chinese export price continues to increase, upside price pressure on the US domestic price should increase as well. Below is the Chinese spot HRC price, displaying its large increase during the second half of June.

With the upcoming holiday week, physical transactions will be sparse, and future market liquidity will decline, giving the market time to digest the price increase announcement. We expect the two dynamics discussed above, along with low imports and inventory levels, will support the increase, and possibly, an additional increase in the near future.

Below are the most pertinent upside and downside price risks:

Upside Risks:

Downside Risks:

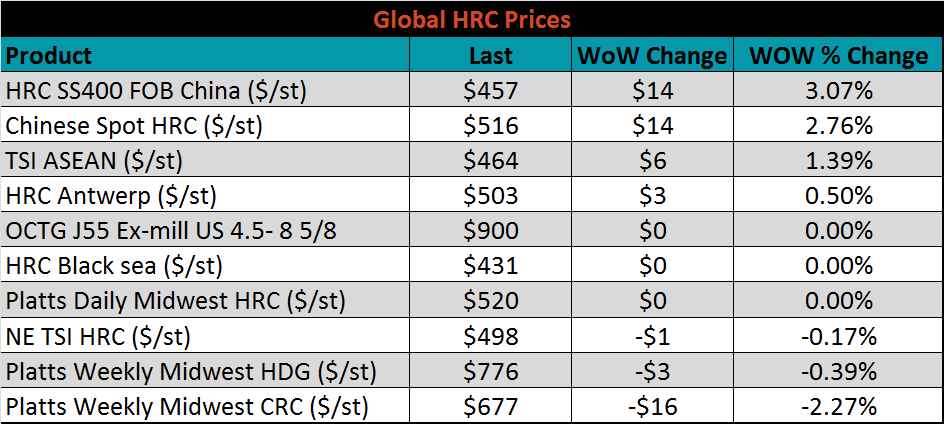

The Platts TSI Daily Midwest HRC Index was unchanged at $520.25.

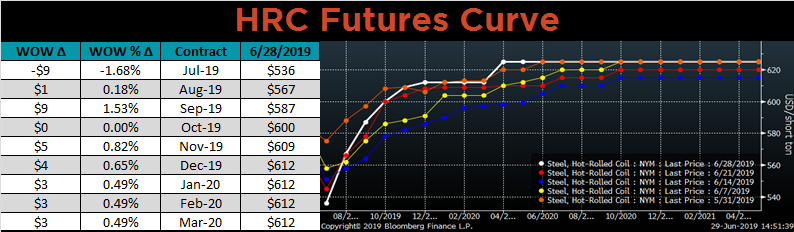

The CME Midwest HRC futures curve is shown below with last Friday’s settlements in white. The back of the curve shifted to the highest levels in the last 4 weeks.

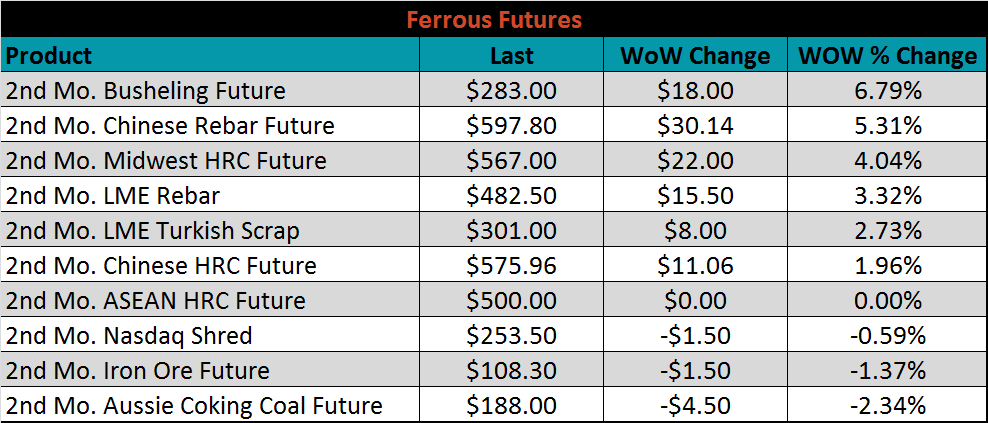

July ferrous futures were mixed. The busheling future gained 6.8%, while coking coal lost 2.3%.

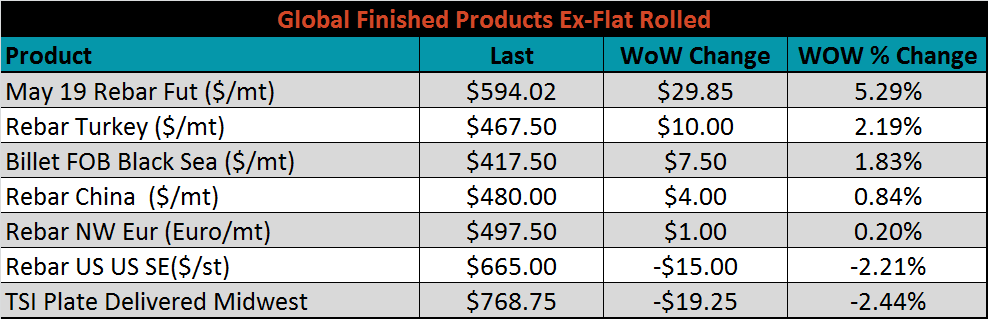

The global flat rolled indexes were mixed. Chinese export HRC was up 3.1%, while Platts Midwest CRC index was down 2.3%.

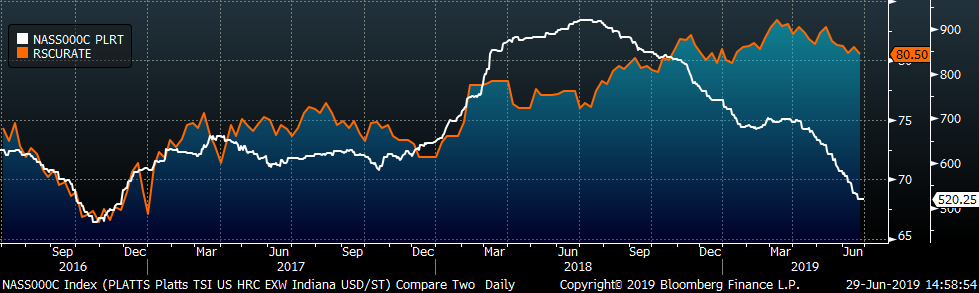

The AISI Capacity Utilization Rate was down 0.6 points to 80.5%. The Trump administration’s goal of 80% Capacity Utilization Rate that has held since October 2018, but announced production cuts should threaten this level.

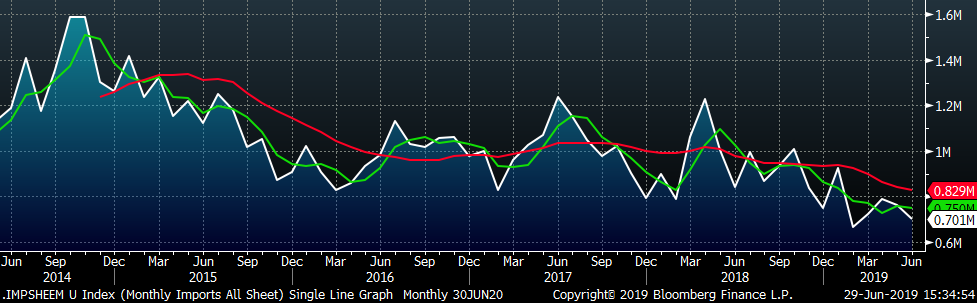

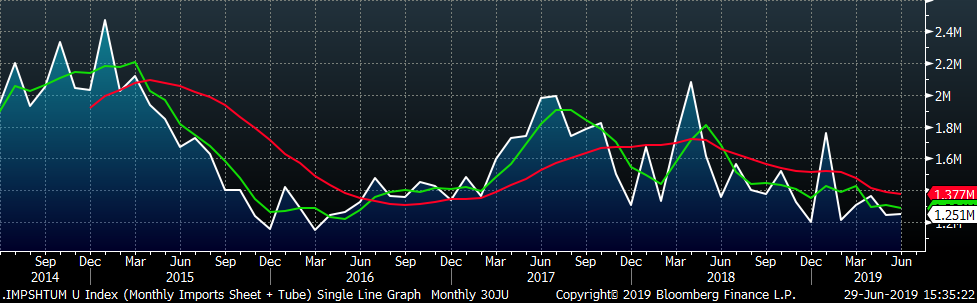

June flat rolled import license data is forecasting a decrease to 701k, down 40k MoM.

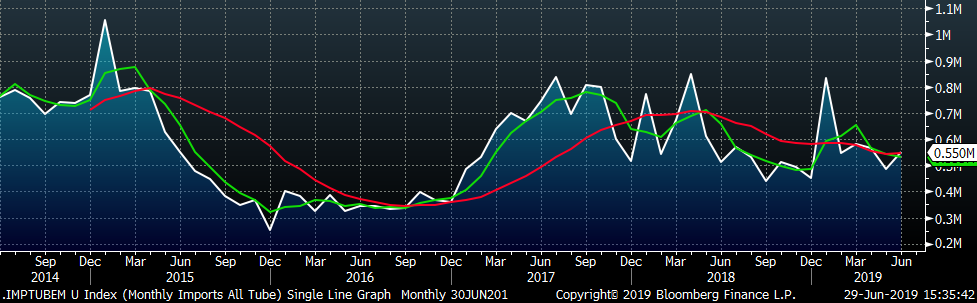

June tube import license data is forecasting a MoM increase of 54k to 550k tons.

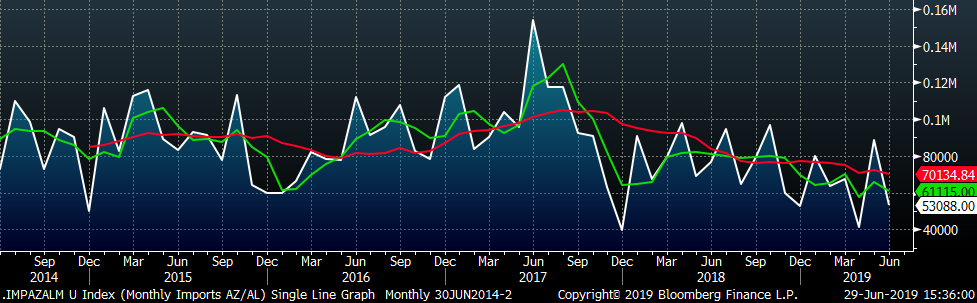

AZ/AL import licenses forecast a decrease of 26k MoM to 62k in June.

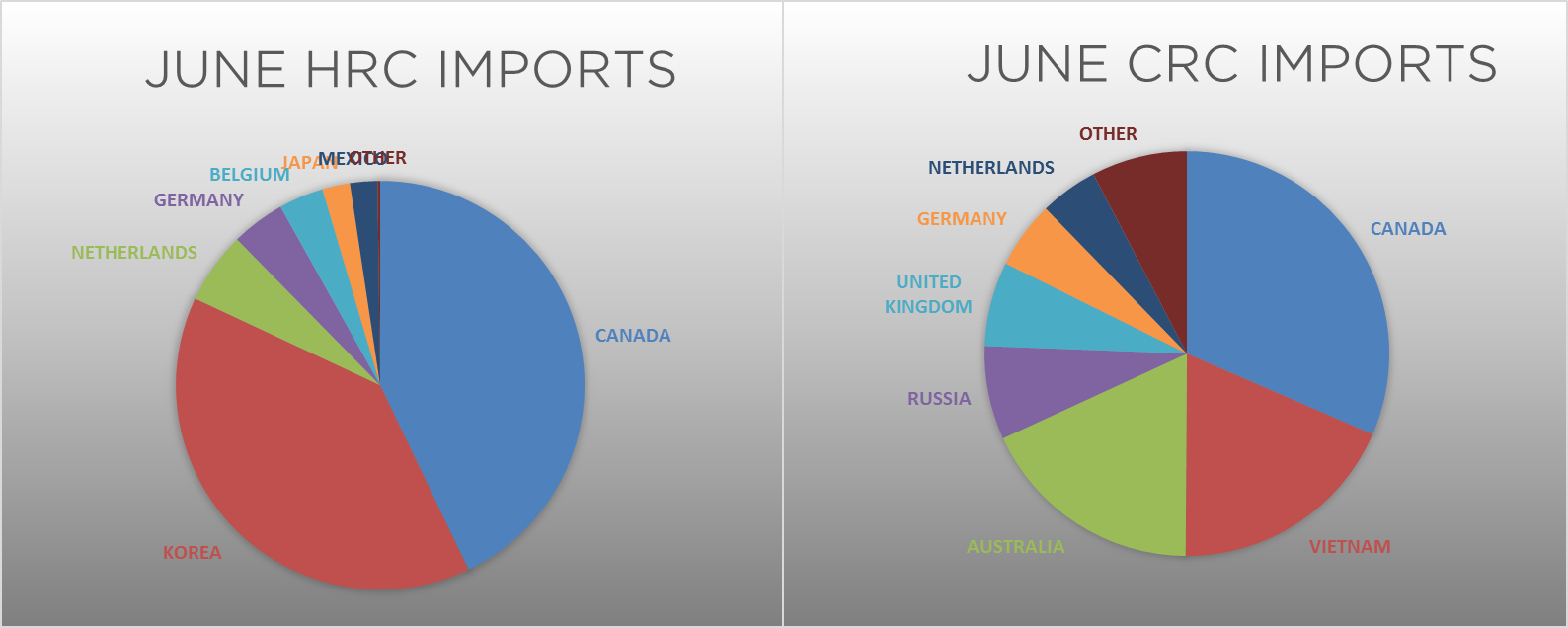

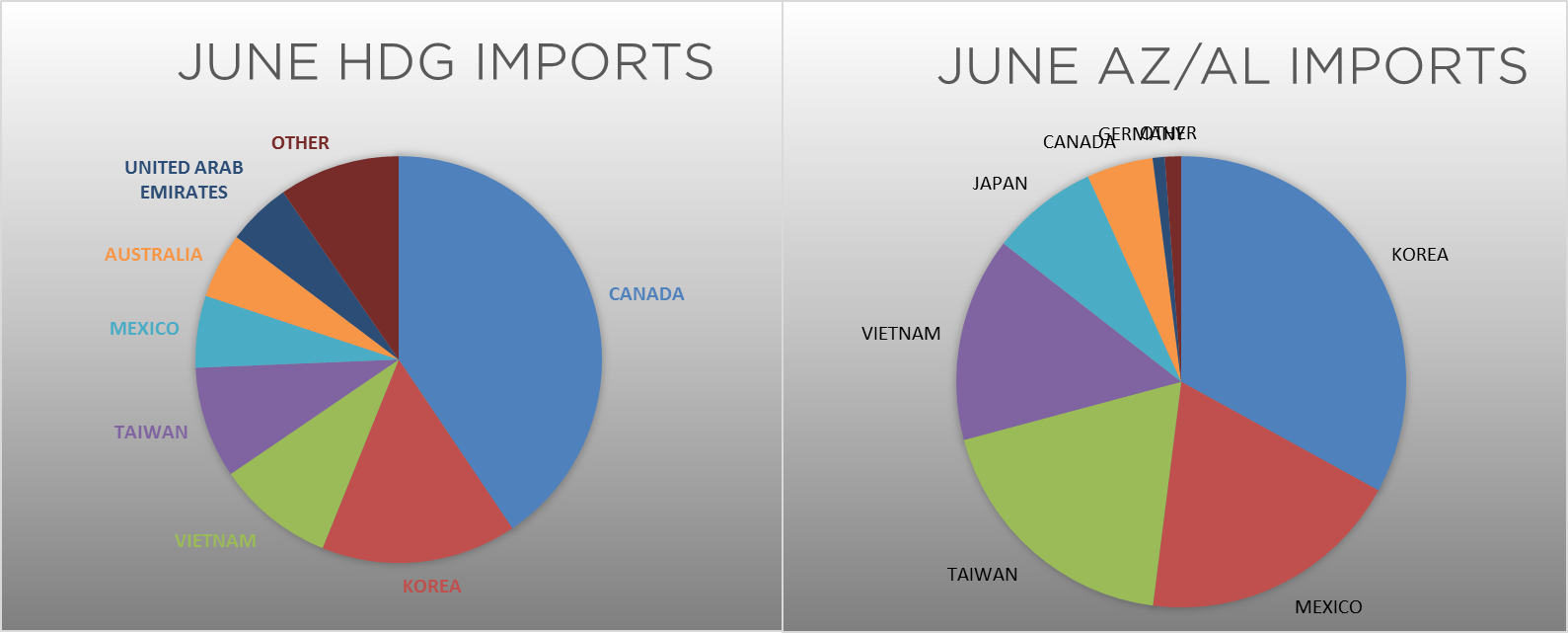

Below is June import license data through June 25, 2019.

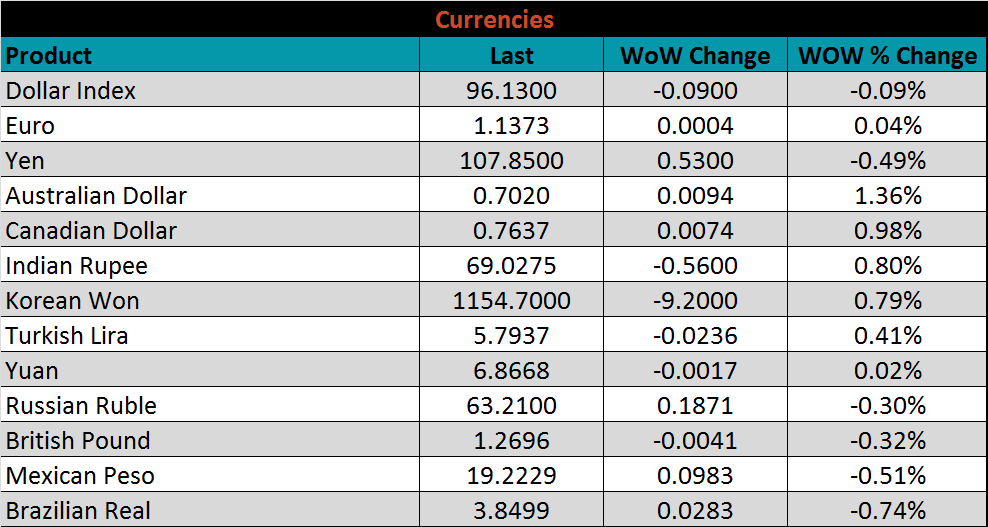

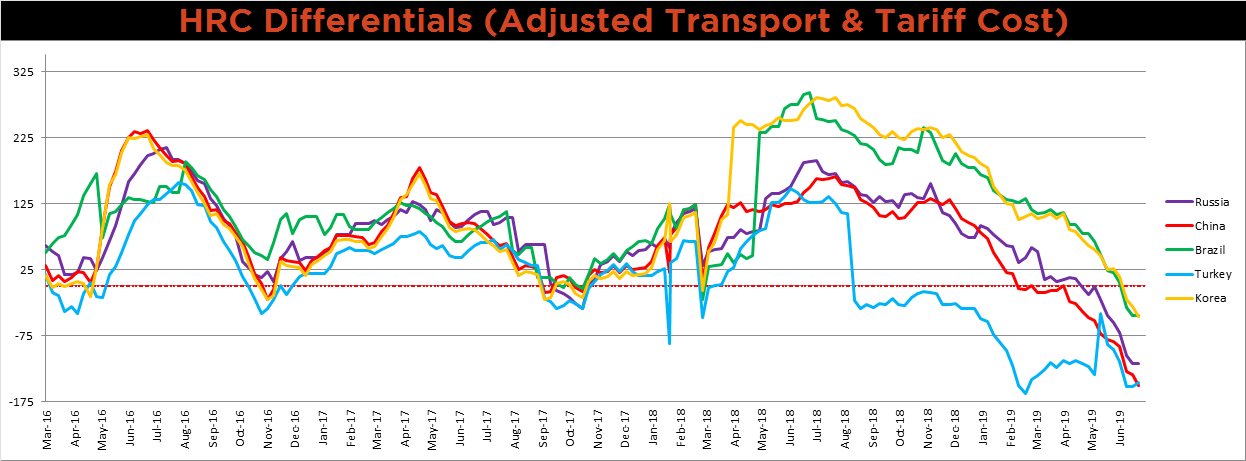

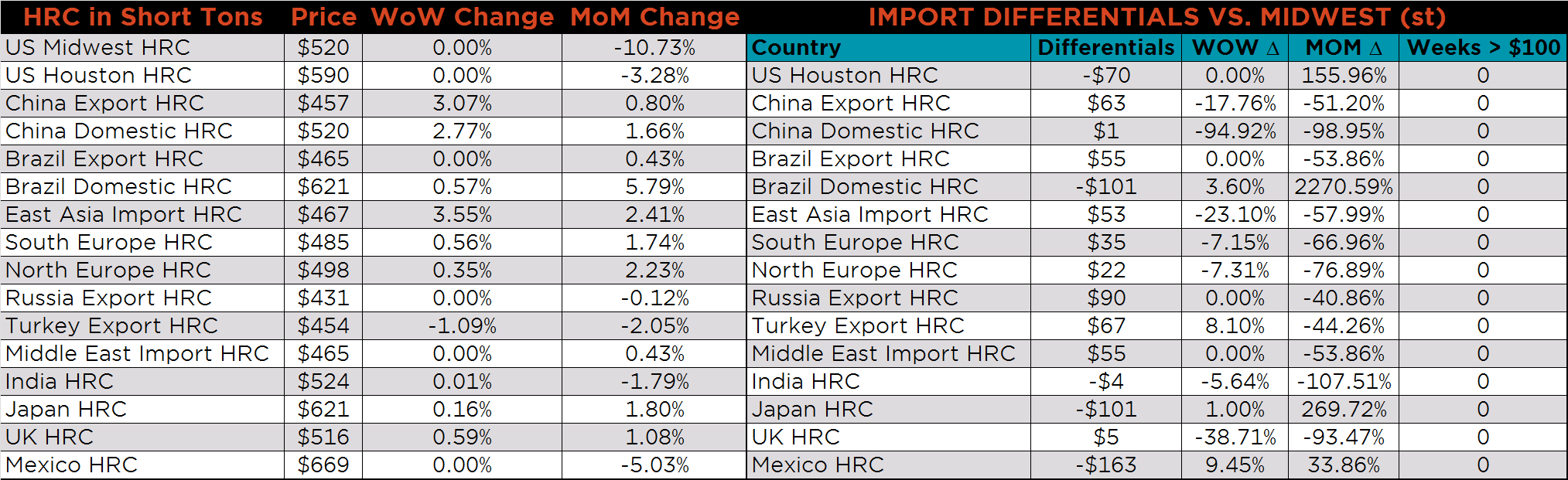

Below is HRC Midwest vs. each listed country’s export price differential using pricing from SBB Platts. We have adjusted each export price to include any tariff or transportation cost to get a comparable delivered price. The Midwest, Brazilian and Russian prices were unchanged last week, while the Chinese and Korean prices rose, and the Turkish price fell. The differentials are at the lowest levels of the last 3 years, with the exception of the Korean differential. Historically, the negative differentials do not last for extended periods.

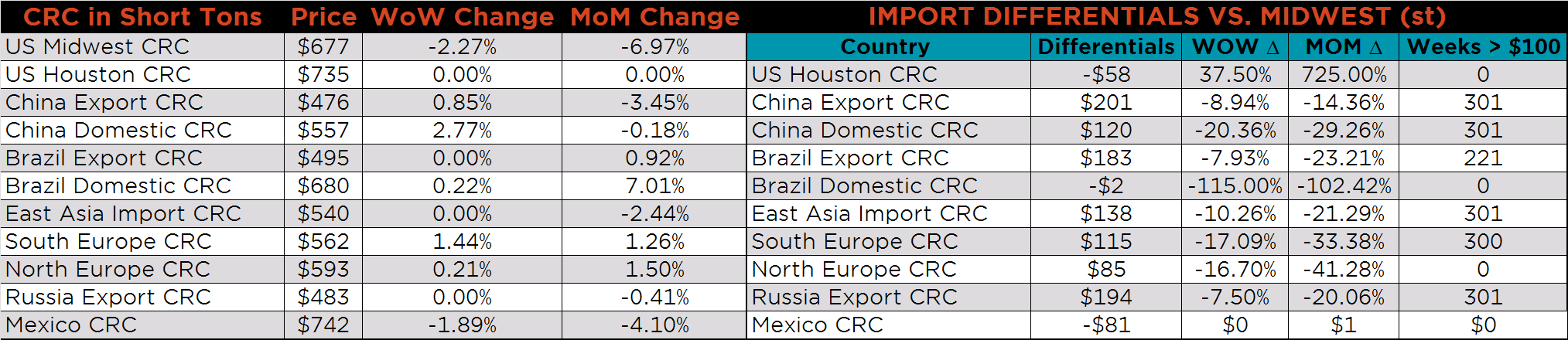

SBB Platt’s HRC, CRC and HDG pricing is below. Midwest HRC was unchanged, while CRC and HDG were lower on the week, down 2.3% and 0.4%, respectively. The Chinese HRC export price was up 3.1%, while the remainder of the major producers showed little change in prices.

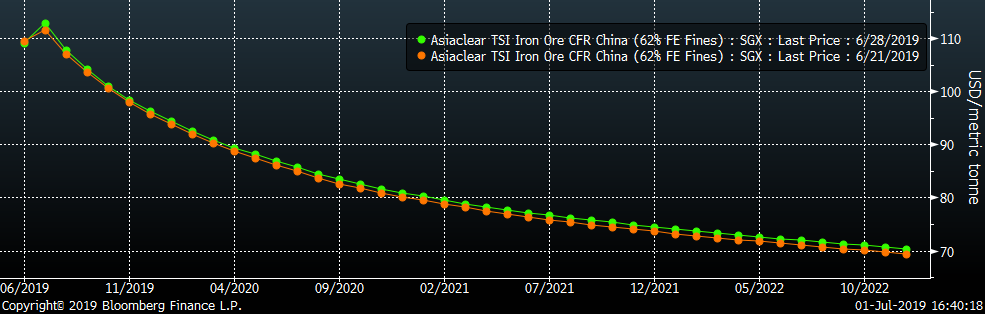

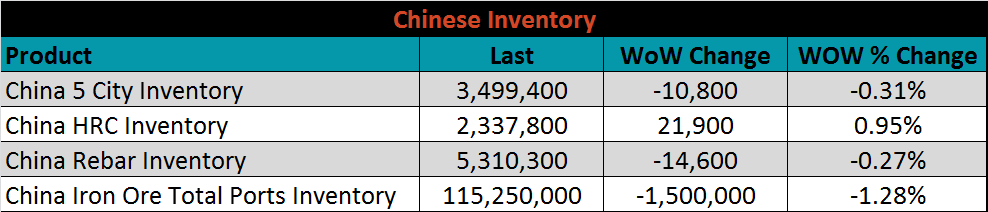

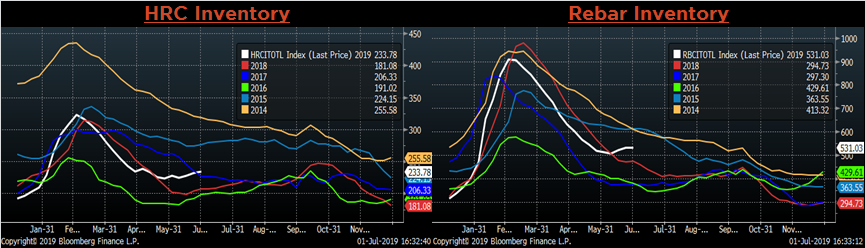

Below are inventory levels for Chinese finished steel products and iron ore. The HRC inventory level moved higher again last week, while the iron ore and rebar inventories both declined. Iron ore inventories have decreased rapidly since April and are now approaching the lowest level in 3 years. Environmental production cuts should reduce demand for iron ore moving into the end of the year.

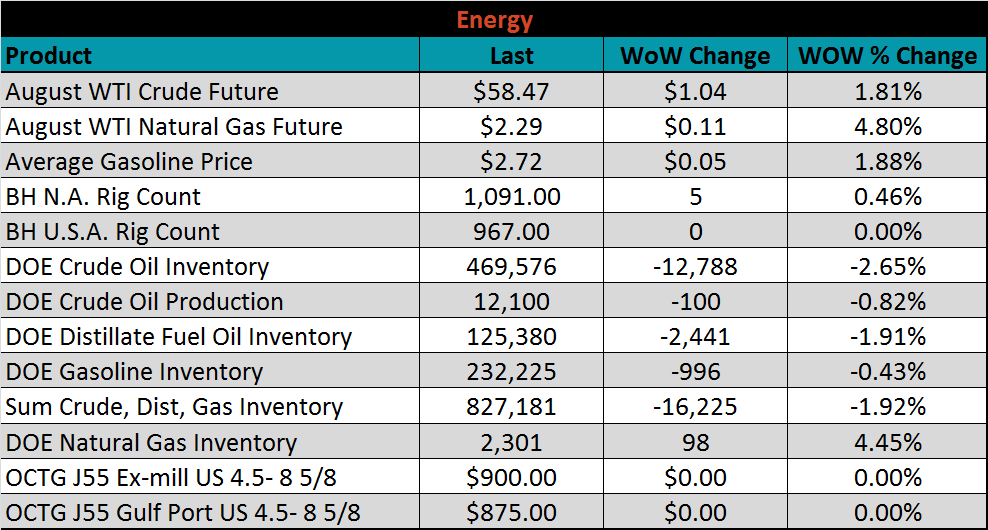

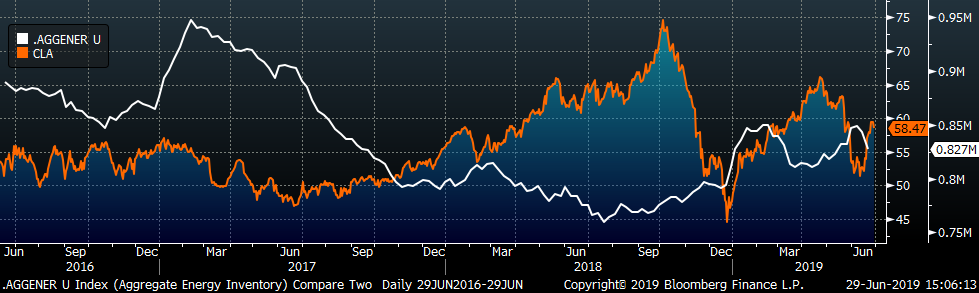

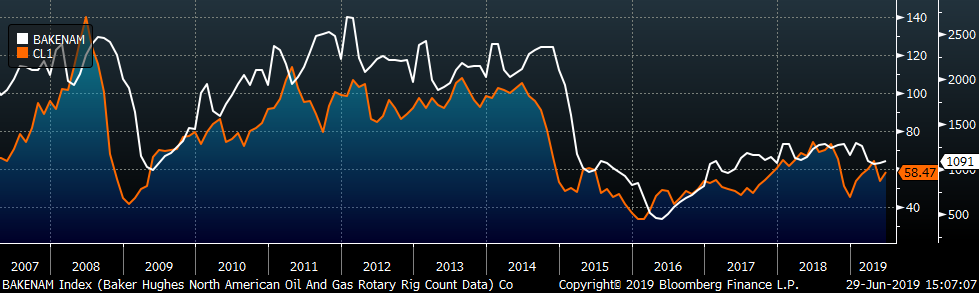

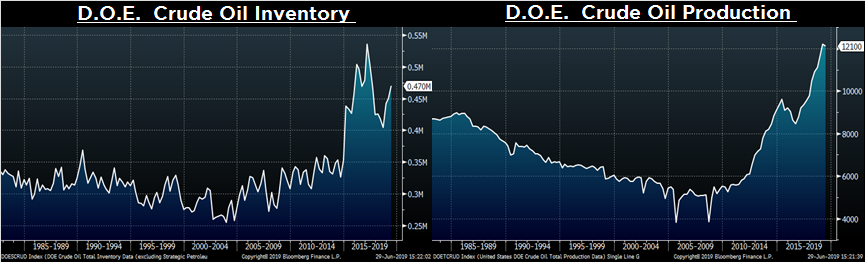

Last week, the Aug WTI crude oil future gained $1.04 or 1.8% to $58.47/bbl. The aggregate inventory level was down 1.9%, and crude oil production fell to 12.1m bbl/day. The Baker Hughes North American rig count gained five rigs while the U.S. count was unchanged.

The list below details some upside and downside risks relevant to the steel industry. The orange ones are occurring or look to be highly likely. The upside risks look to be in control.

Upside Risks:

Downside Risks: