Content

-

Weekly Highlights

- Market Commentary

- Risks

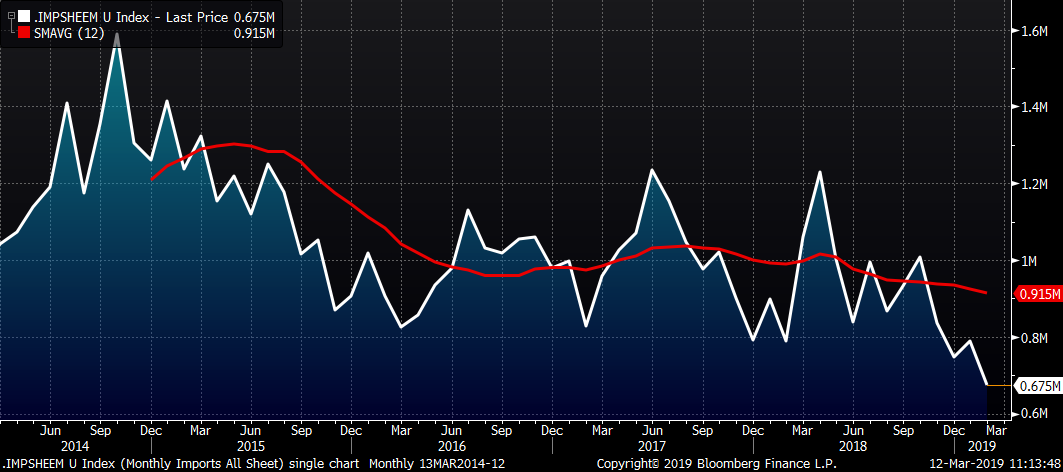

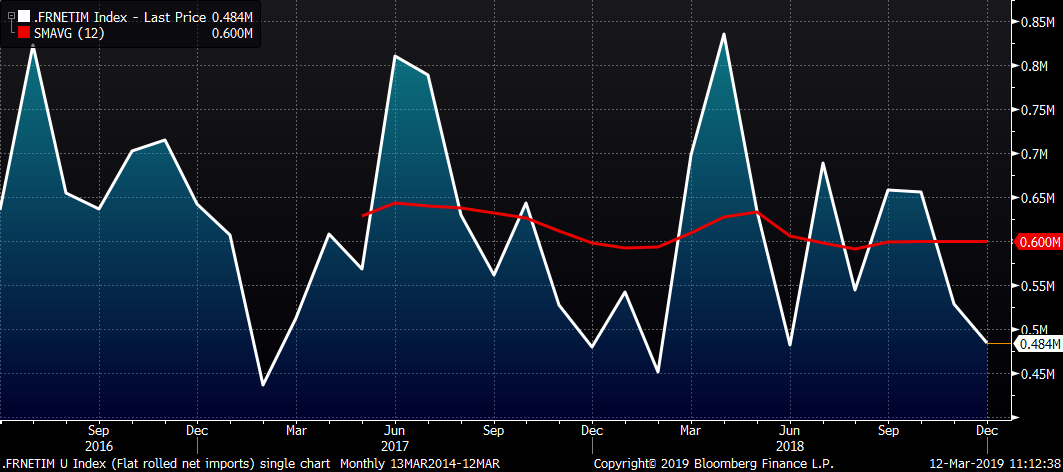

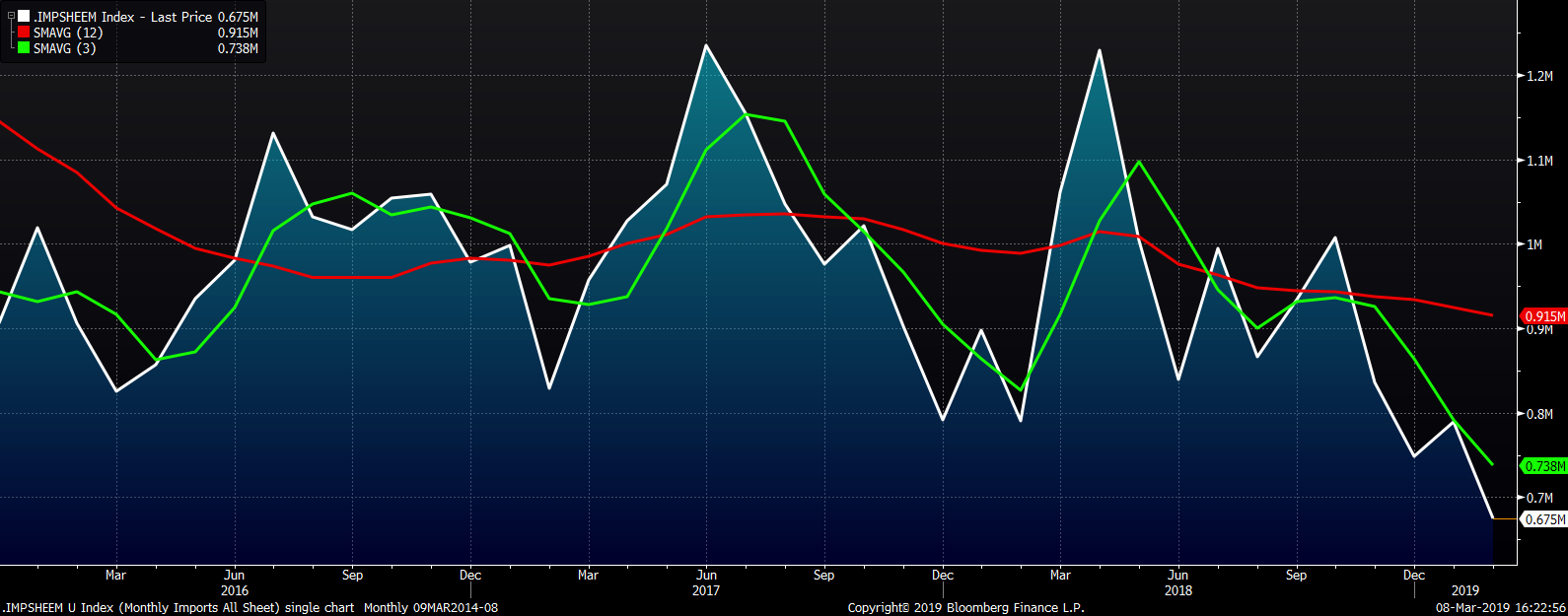

Flat rolled imports have fallen dramatically since last October with the last three months of imports tracking below the lowest monthly import level since early this decade.

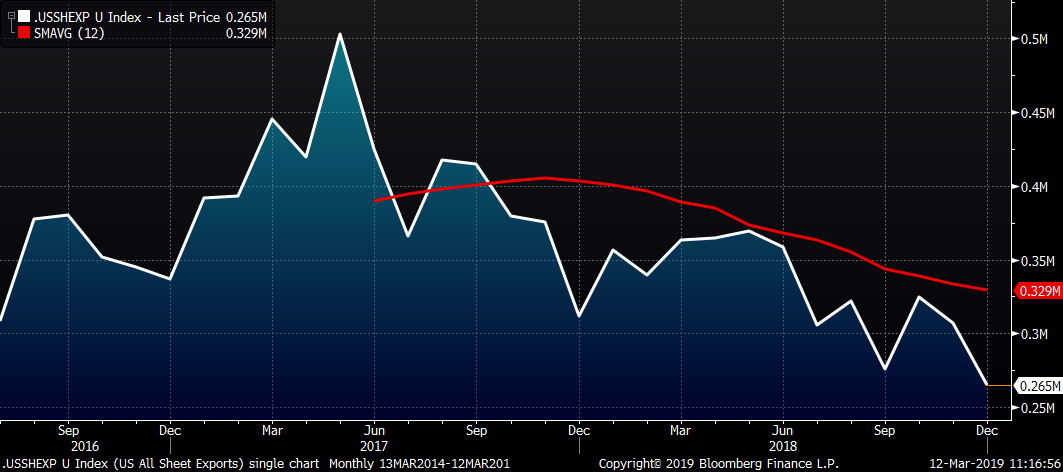

Flat rolled exports have also fallen abruptly starting shortly after the U.S. applied 25% steel tariffs.

Net import data through December shows a steady twelve-month average of 600k st/m with November and December falling below the average.

Annual U.S. flat rolled net imports actually increased by 32k tons YoY to 7.2m in 2018 vs. 7.17m in 2017. However, digging deeper into the data, there was an increase of almost 800k hot rolled tons, while CR, HDG and galvalume (AZAL) imports fell significantly. Tube imports fell 13% or almost 930k tons YoY.

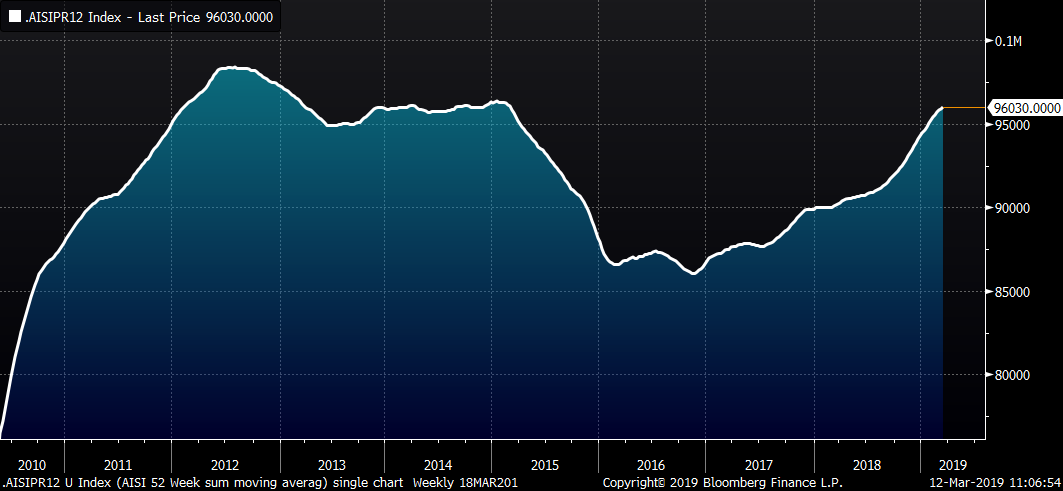

While the tariffs have yet to materially change flat rolled net imports, production has grown significantly as evidenced by this 52-week moving sum of the AISI’s weekly crude steel production.

With the reopening of U.S. Steel’s Granite City, new entrant JSW steel and the AISI steel capacity utilization remaining above 80% since mid-October 2018, the sum of the previous 52 weeks has grown to 96 million annualized tons, the highest level since March 2015.

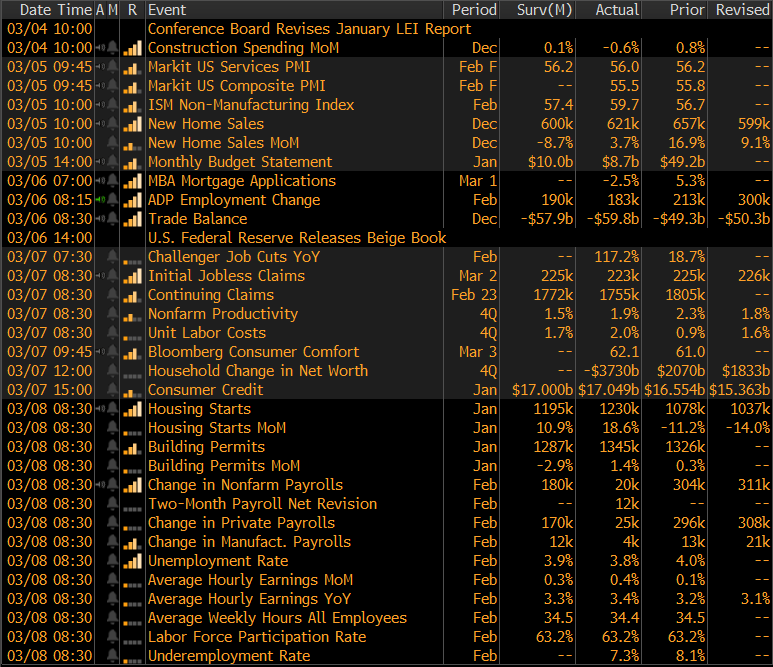

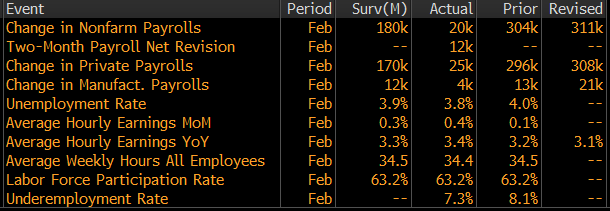

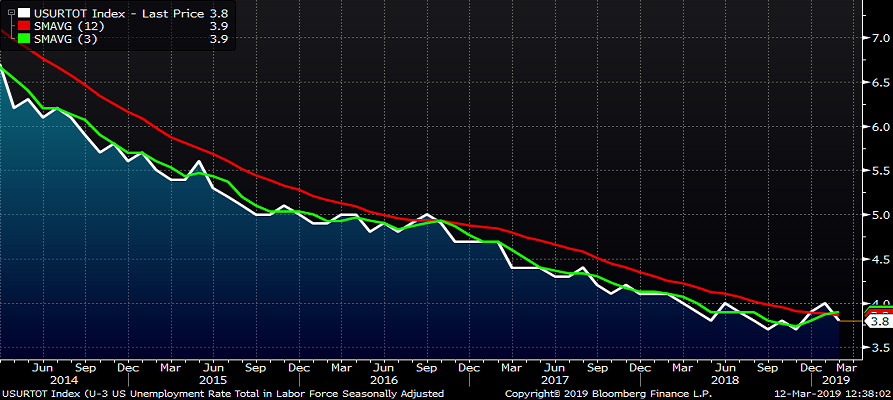

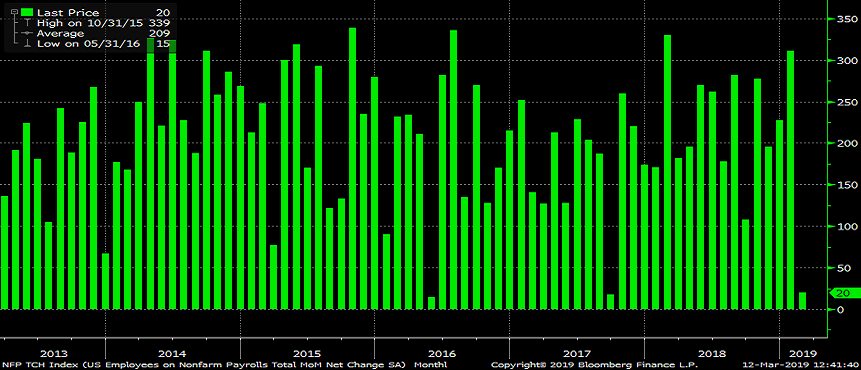

Last week’s U.S. employment report was a massive disappointment with a change of 20k new jobs vs. expectations of a 180k job gain. The manufacturing industry added 4k jobs versus expectations of 12k, but January’s 13k job gain was revised higher to 21k. The unemployment rate fell to 3.8%, better than expected despite the Labor Force Participation Rate remaining unchanged at 63.2%. This report raises a big question of whether this was an anomaly or indicative of continued weakness.

The unemployment rate saw its three-month moving average cross above its twelve-week moving average.

The chart below shows MoM net change in nonfarm payrolls. A significant drop in MoM nonfarm payrolls occurred once in 2016 and 2017, both of which saw a significant rebound the next month.

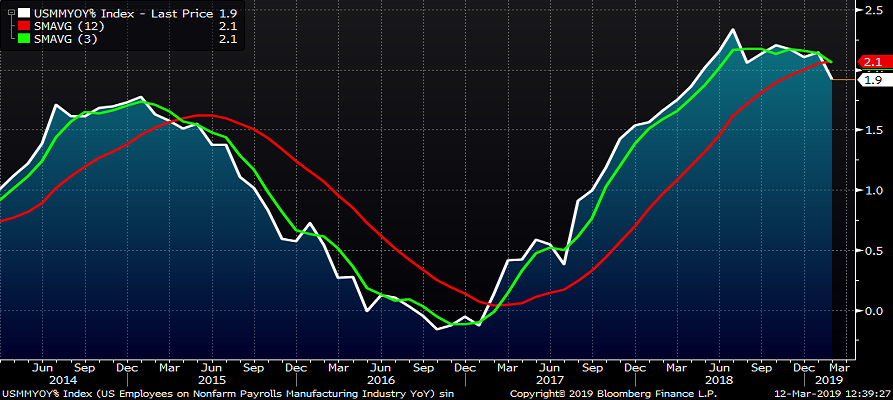

The chart below shows the YoY percentage change in nonfarm payrolls rolling over.

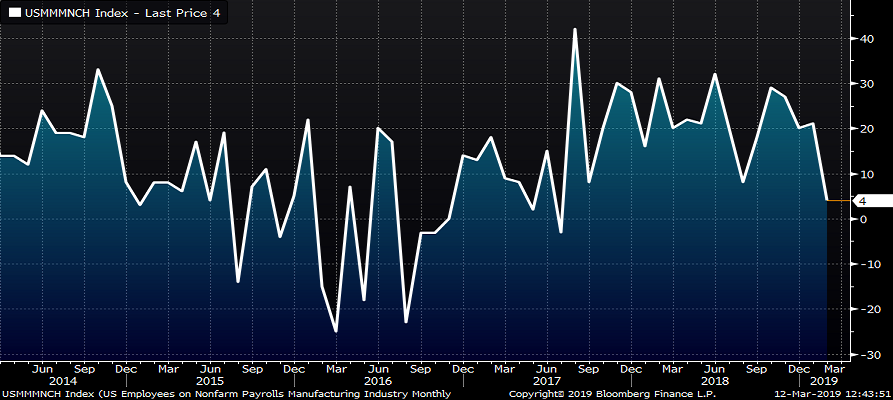

The manufacturing industry added four thousand jobs in February, the lowest net change since July 2017.

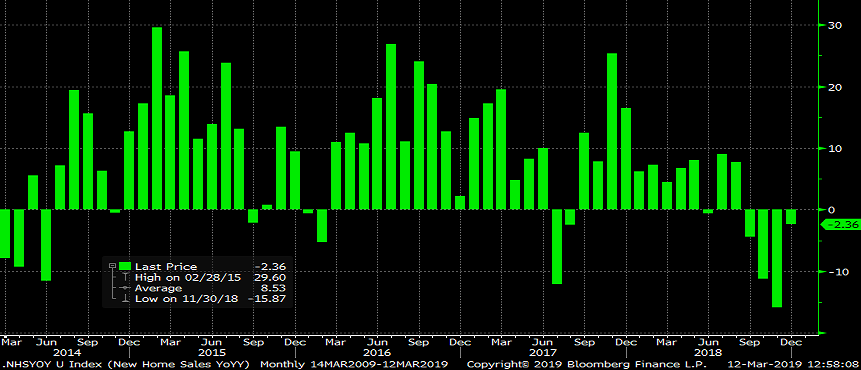

December new home sales of 621k annualized units beat expectations of 600k, but November’s rate was revised lower to 599k from 657k. The chart below shows four consecutive months of YoY contraction in new home sales.

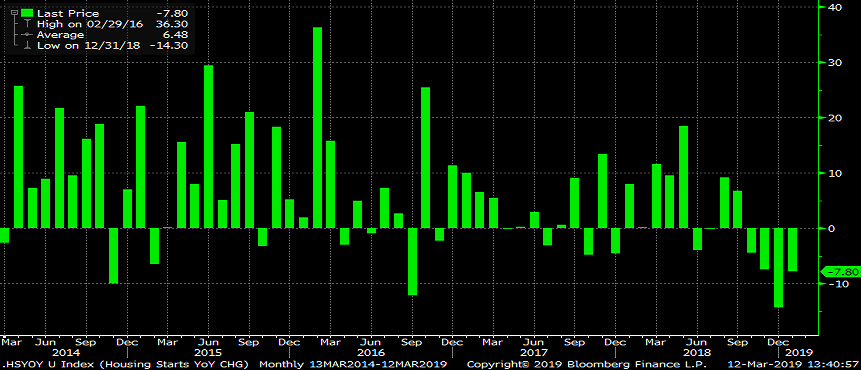

U.S. housing starts of 1.23m annualized units were better than expected, but December’s rate of 1.08m units was revised lower to 1.04m. Similar to new home sales, housing starts have seen four straight months with negative YoY growth.

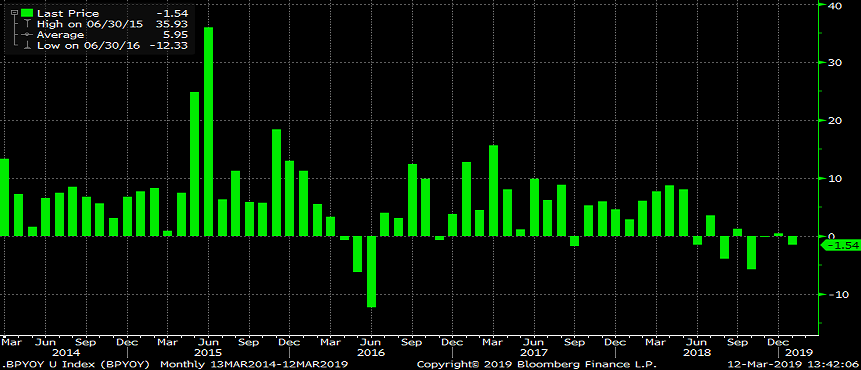

January U.S. annualized building permits rose to 1.35m from 1.33m in December and beat expectations. YoY growth rates have been negative or barely positive for the past six months.

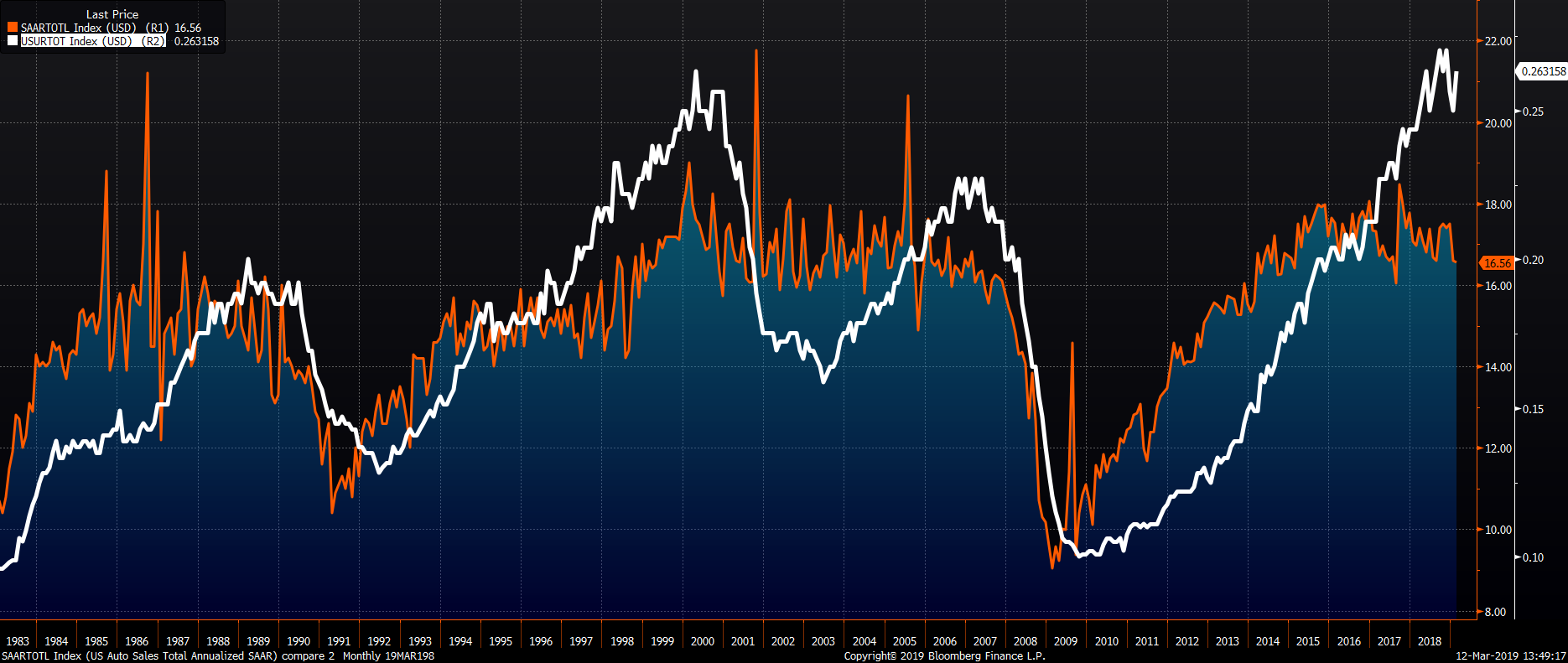

Last week provided another swath of diverse data indicating a slowing U.S. economy. This chart shows an inverted U.S. employment rate, annualized U.S. auto sales and how correlated the two are over time. Employment is typically a lagging indicator. Does the downtrend in auto sales indicate a weakening job market to follow?

As 2019 moves forward, the health of the economy will become apparent. Perhaps the economy reverses course in the coming months, but right now, the steel industry is seeing weakening demand, increased supply at steel mills, increased steel production and a wounded service center group with potential for the removal of steel tariffs to boot. Continue to proceed with caution.

Upside Risks:

Downside Risks:

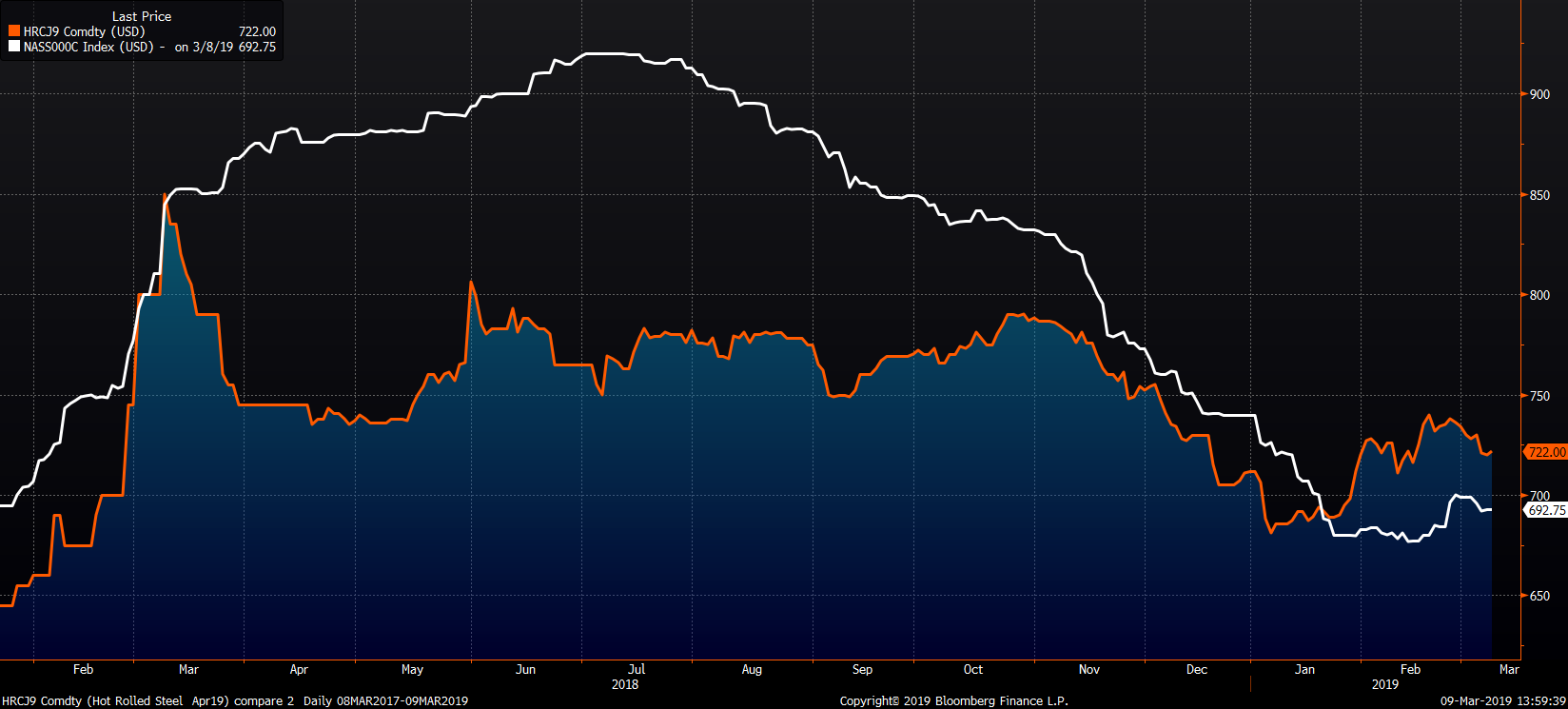

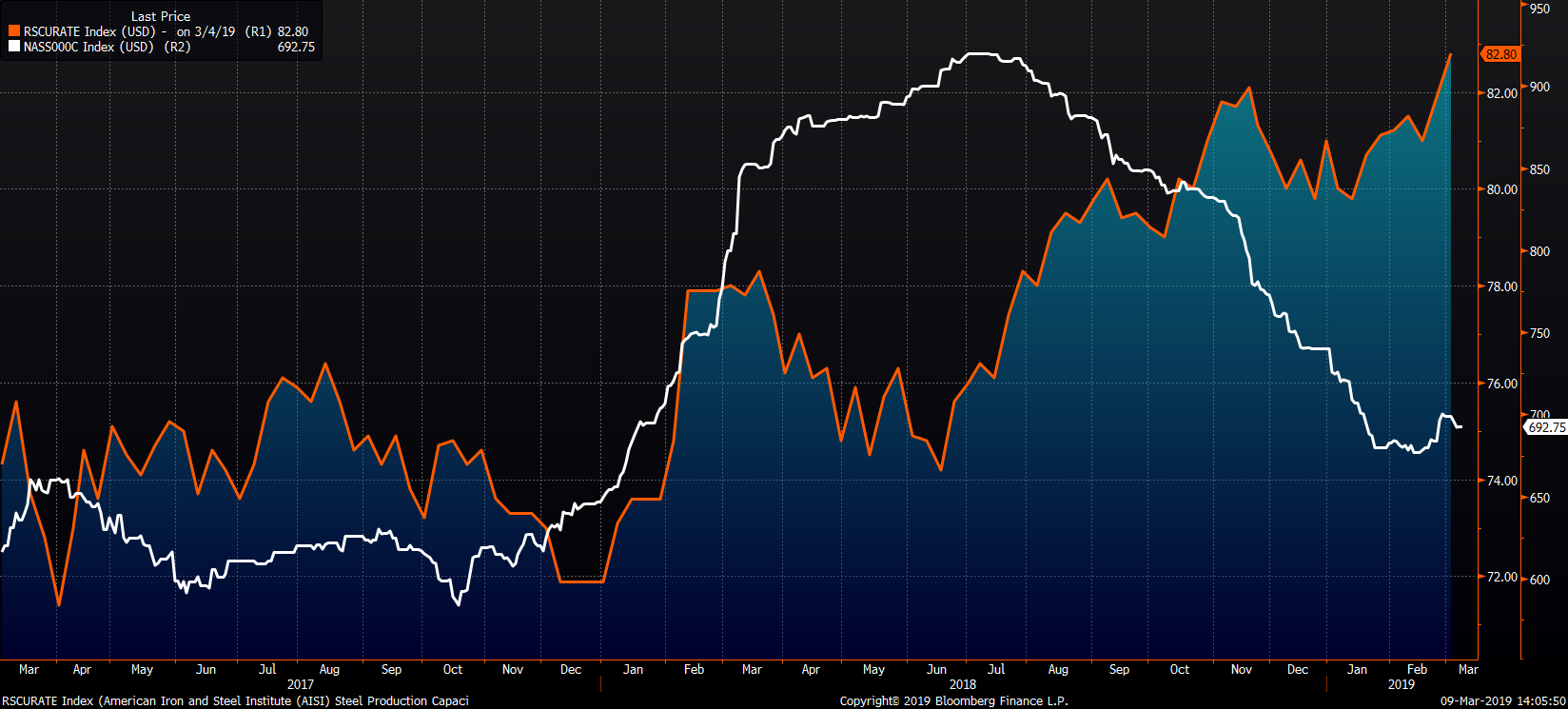

Week over week, the April CME Midwest HRC future lost $8 to $722 while the Platts TSI Daily Midwest HRC Index was down $6.50 to $692.75.

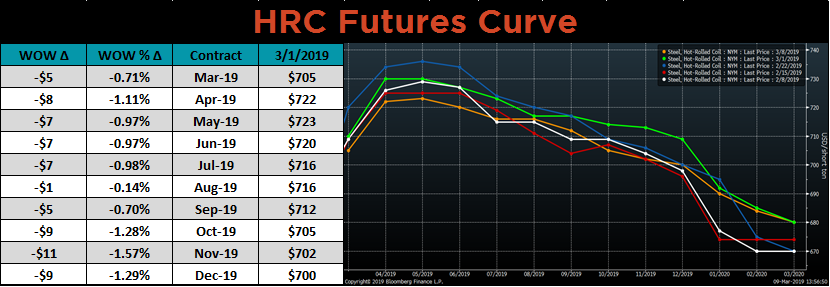

The CME Midwest HRC futures curve shown below with last Friday’s settlements in orange.

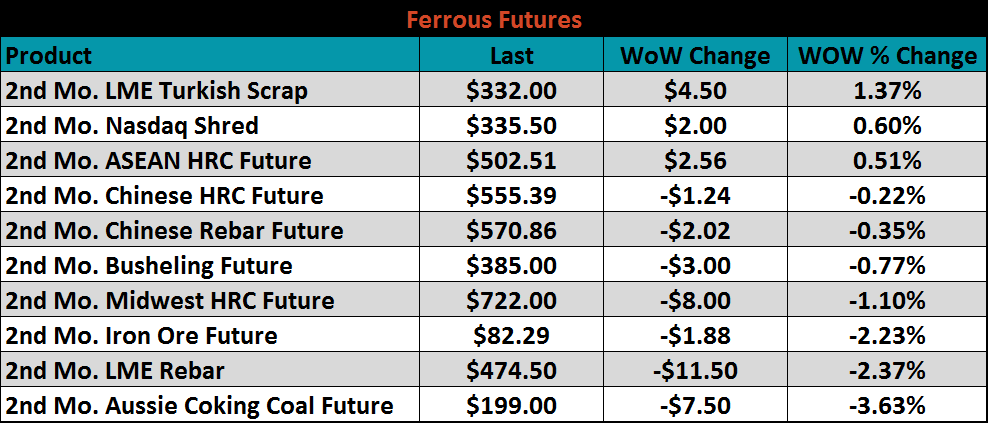

April ferrous futures were mixed, but saw broad based weakness with coal, ore, rebar and US HRC falling.

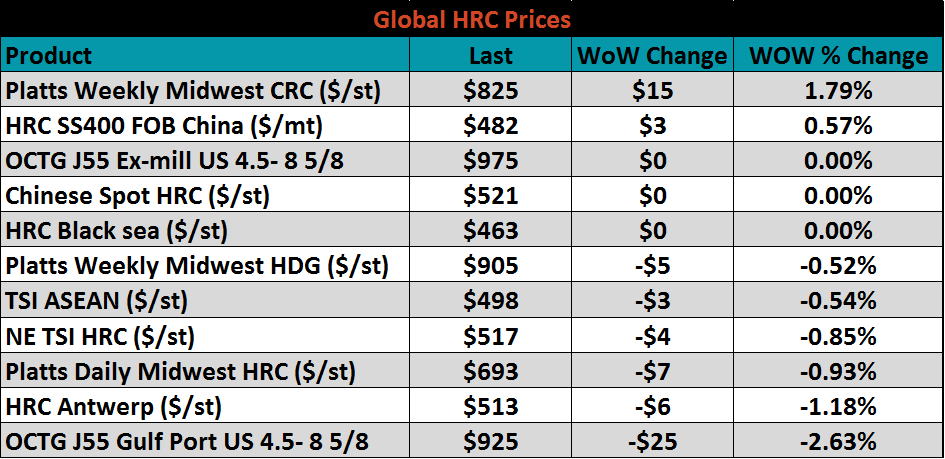

Flat rolled indexes were mixed.

The AISI Capacity Utilization Rate held at 81.9%.

February flat rolled import licenses are forecast to fall 115k tons MoM to 675k while January flat rolled import licenses are forecast to increase 41k tons MoM to 789k.

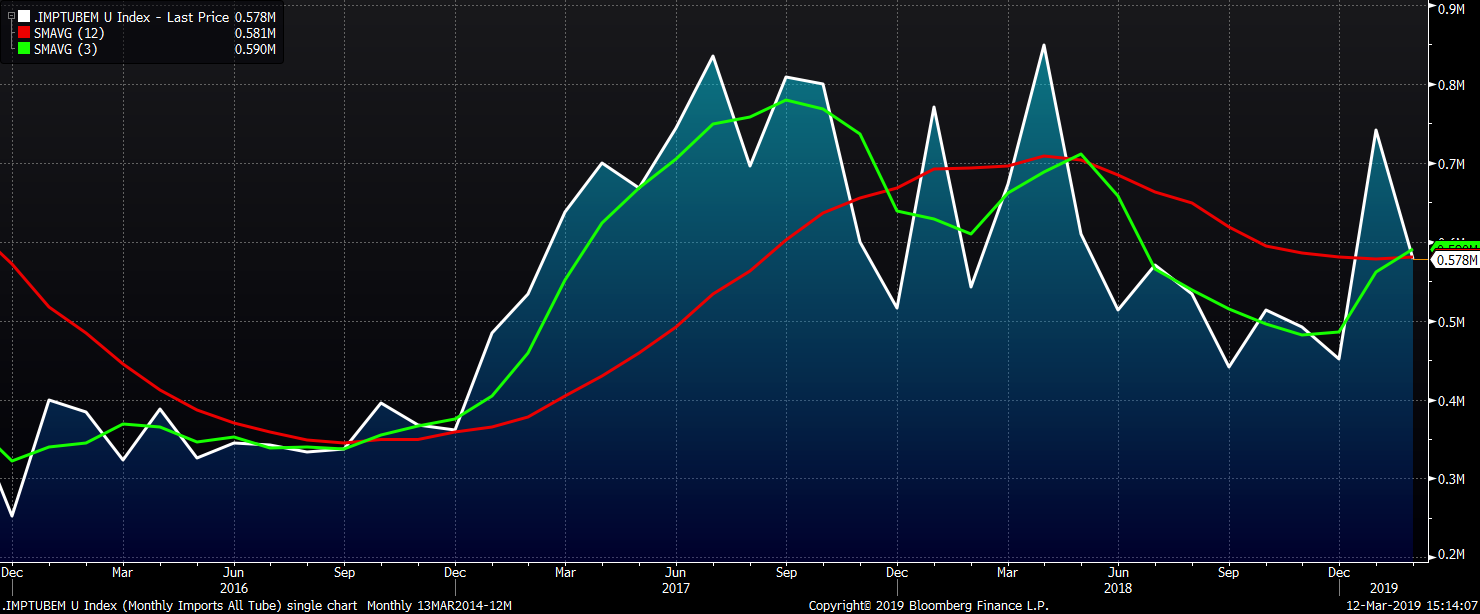

February tube import license data is forecasted to fall 164k to 578k tons MoM after a sharp rise in January.

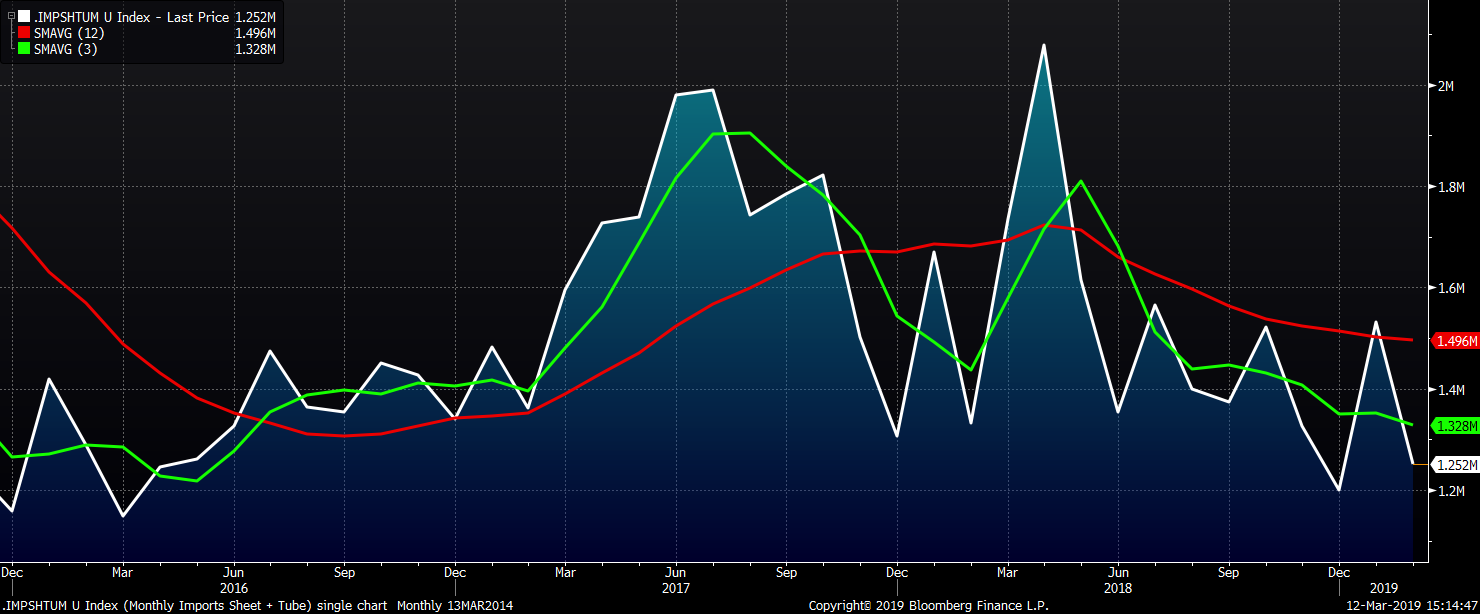

The combined flat and tube import license forecast looks to fall 279k tons in February after a 331k MoM increase forecast in January.

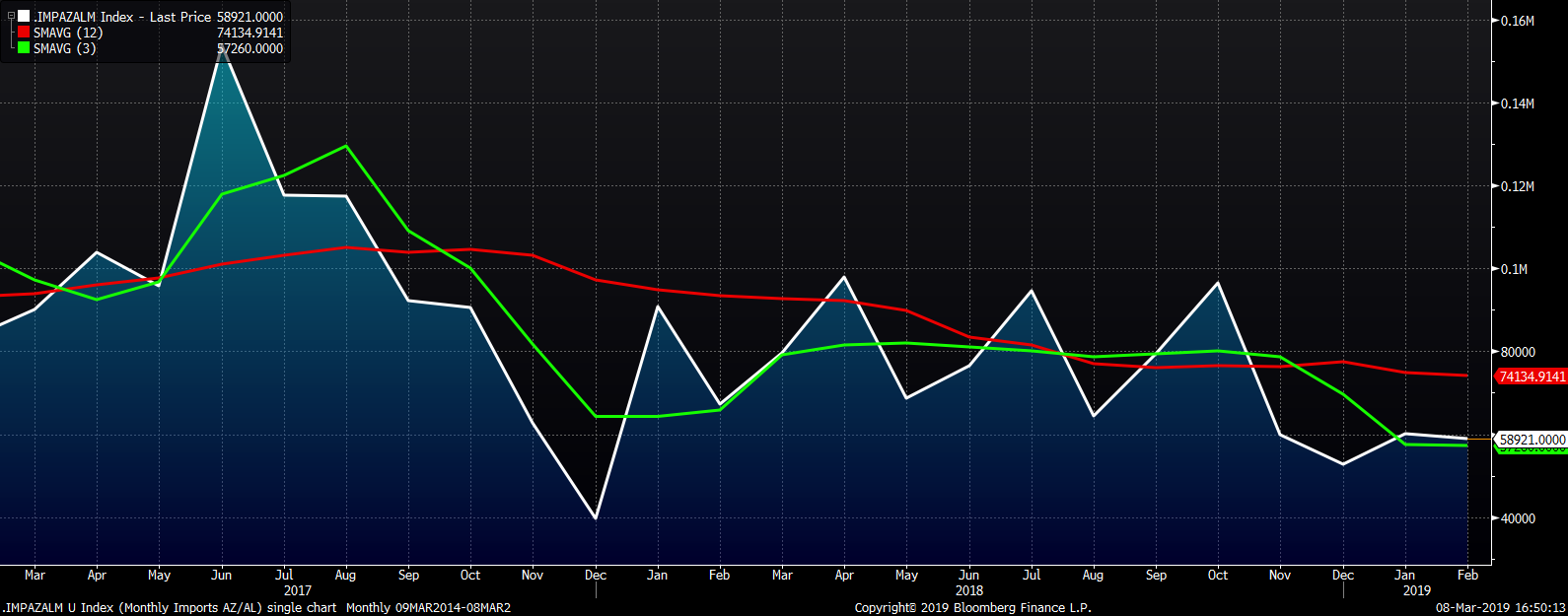

AZ/AL import licenses remained in the 50-60k range since November with February licenses forecast at 59k.

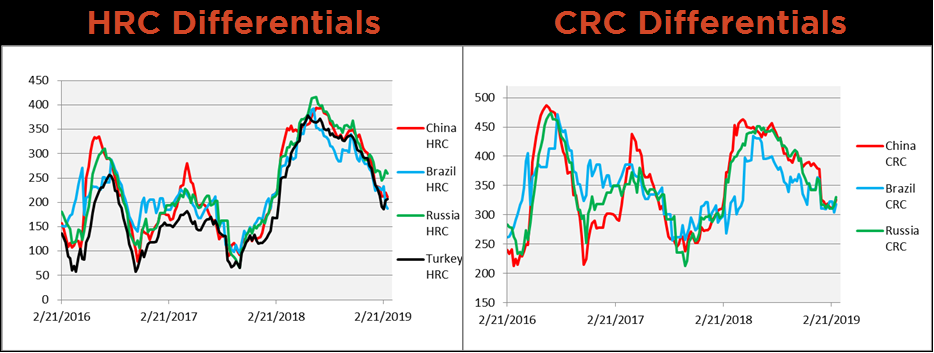

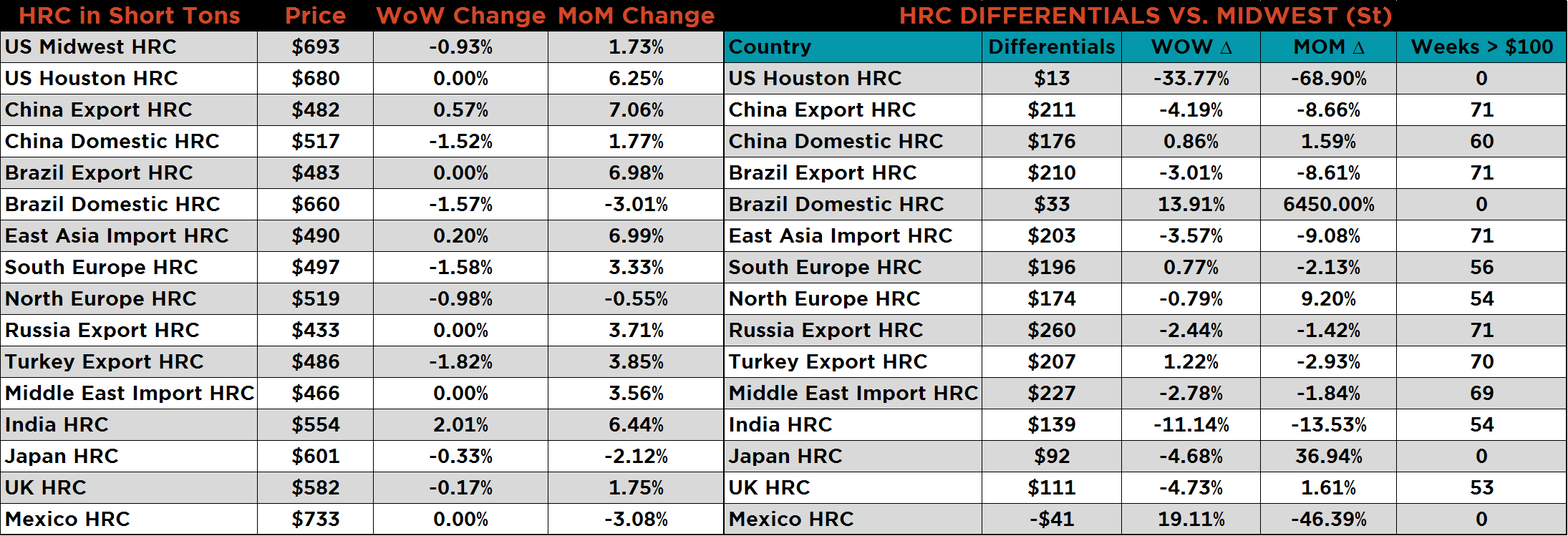

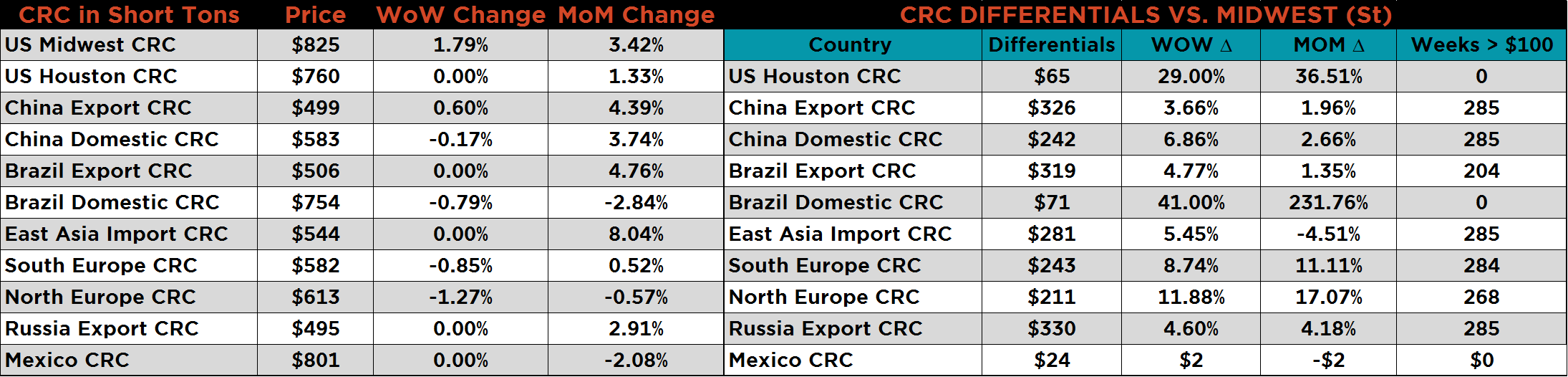

Below are HRC and CRC Midwest vs. each country’s export price differentials using pricing from SBB Platts. The Chinese, Brazilian and Russian HR differentials all fell, while the Turkish HR differential rose. The Chinese, Brazilian and Russian CR differentials all rose as U.S. CR prices continue to rise.

SBB Platt’s HRC, CRC and HDG WoW pricing is below. The Midwest HRC and HDG prices fell 1% and 0.5%, respectively, while CRC gained 1.8%. The Chinese and Brazilian domestic, and Southern European HRC prices fell 1.5%, while the Indian HRC prices rose 2%.

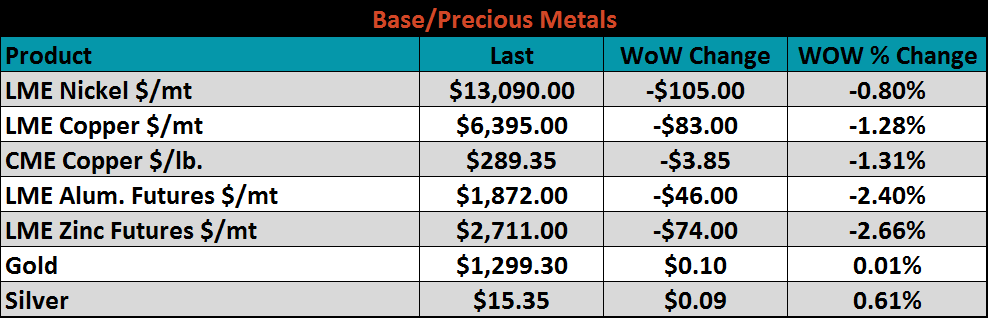

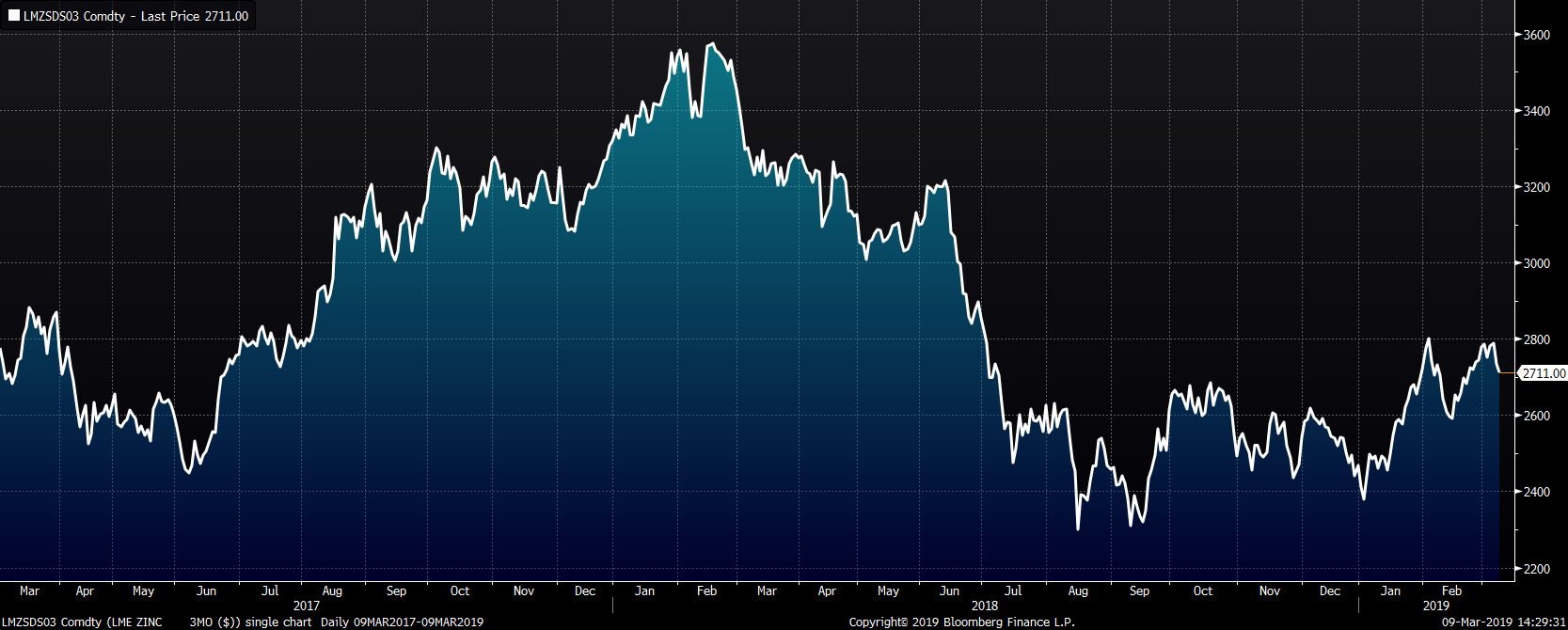

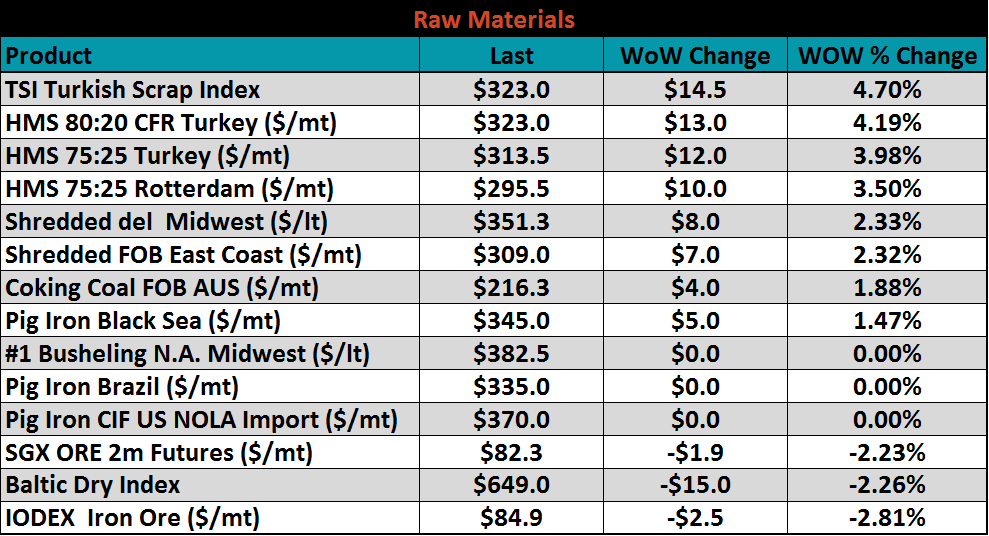

Scrap prices were mostly higher. Iron ore futures and spot prices fell over 2%.

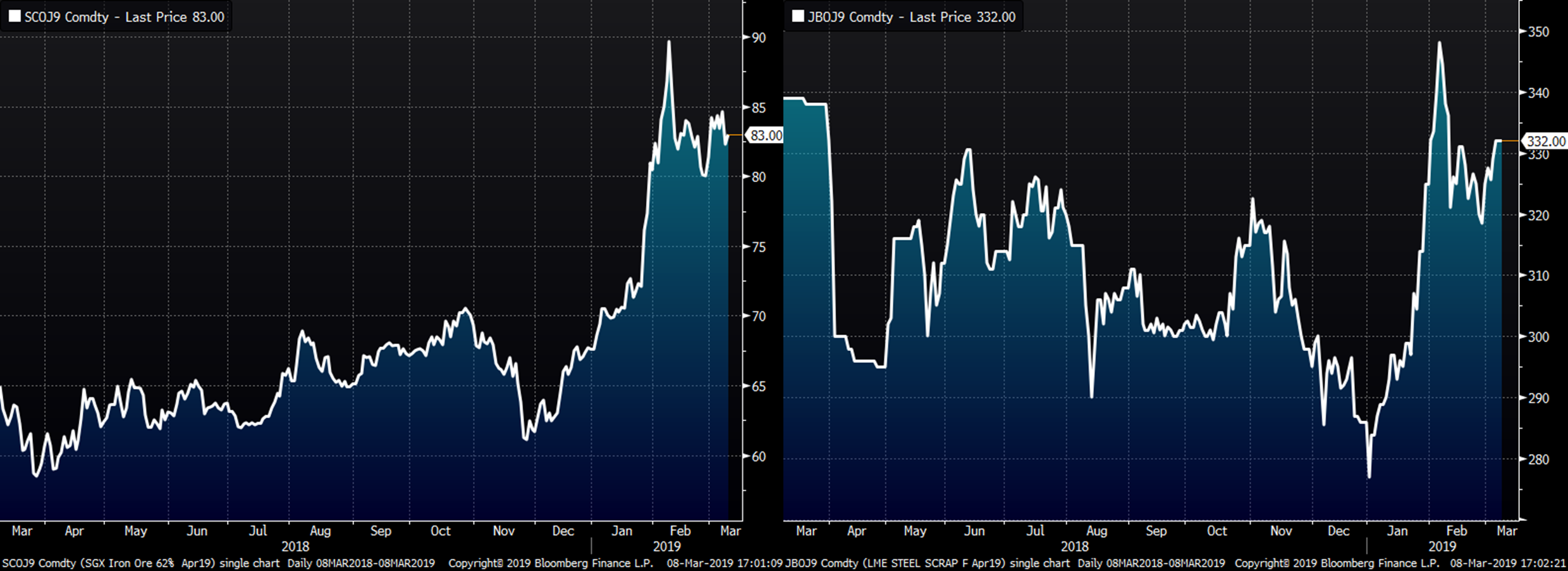

The April SGX iron ore future lost $1.17 to $83 and the April Turkish scrap future added $4.50 to $332.

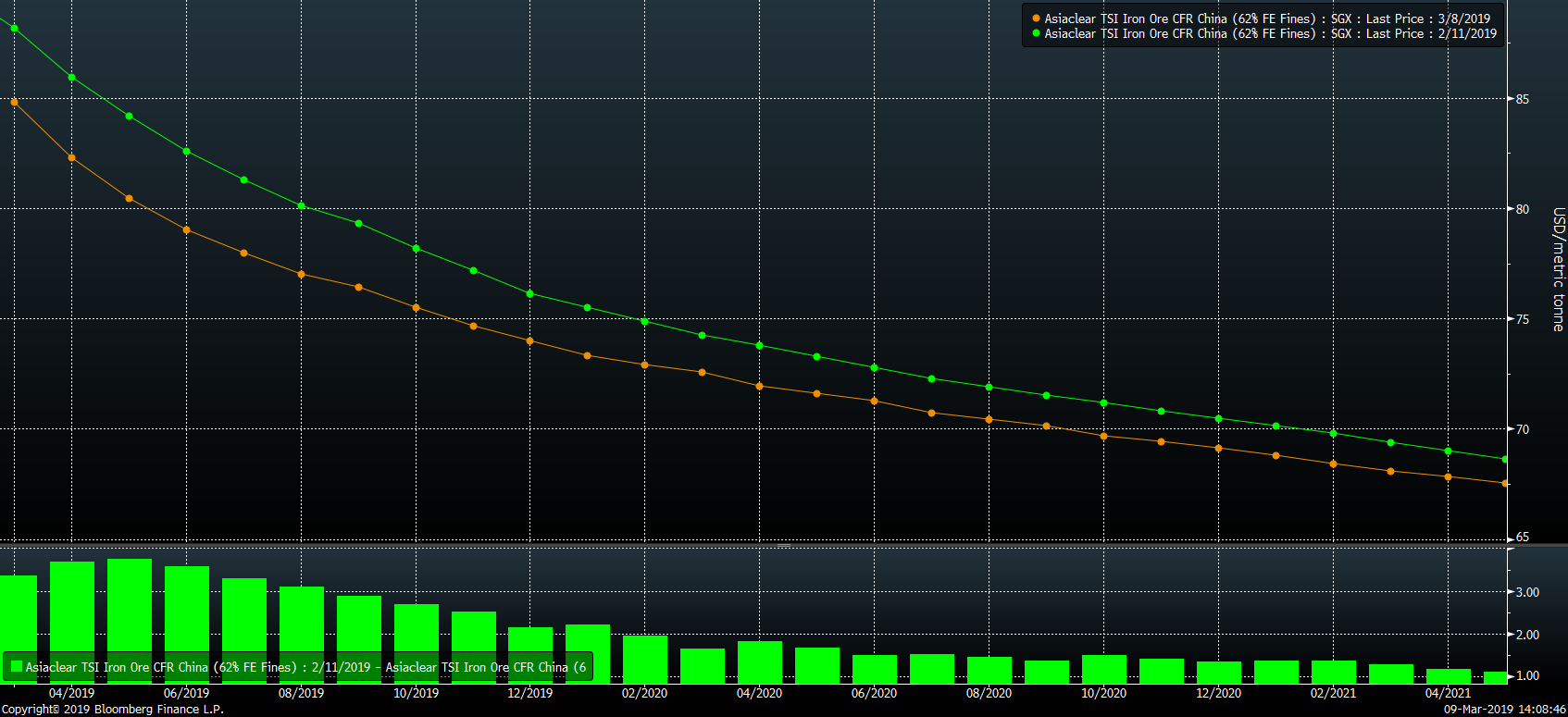

The SGX iron ore futures curve fell below last month while flattening in later months.

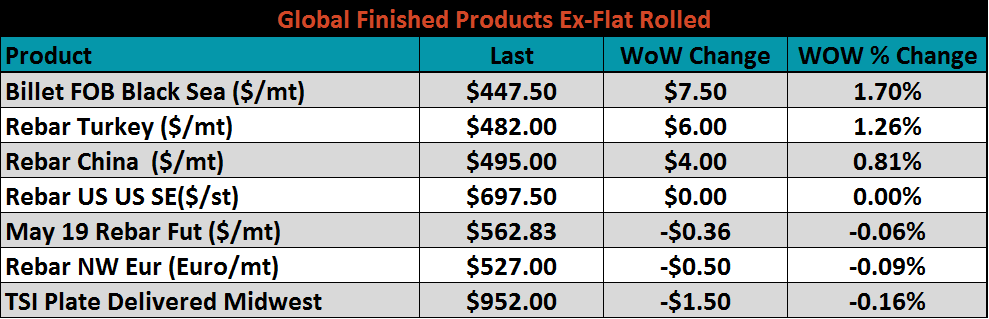

Ex-flat rolled prices saw Black Sea billet and Turkish rebar gain 1.7% and 1.3%, respectively.

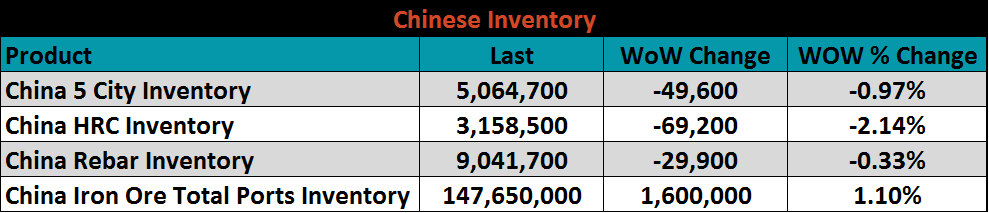

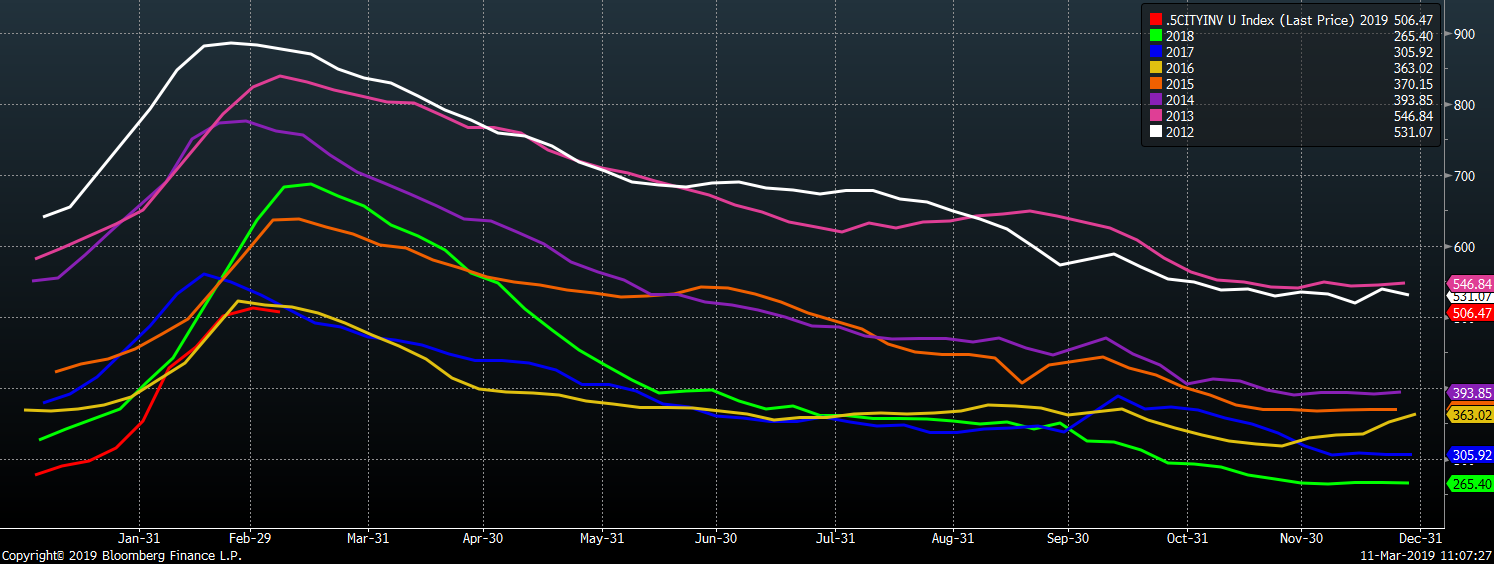

Below are inventory levels for Chinese finished steel products and iron ore. Iron ore inventory continues to rise up 1.1%. Finished steel inventory levels may have reached their seasonal peaks.

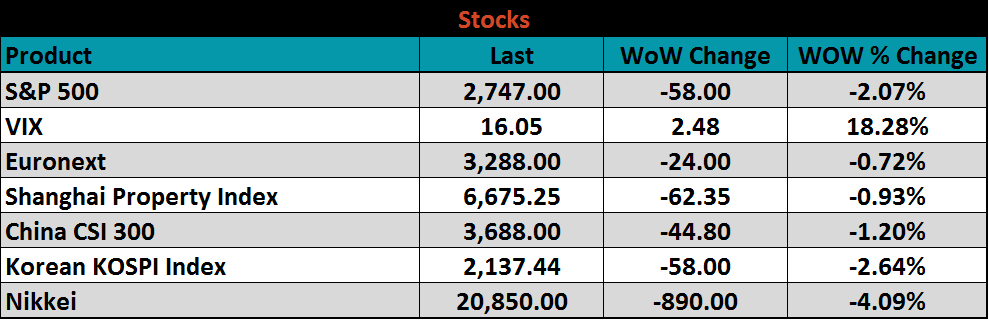

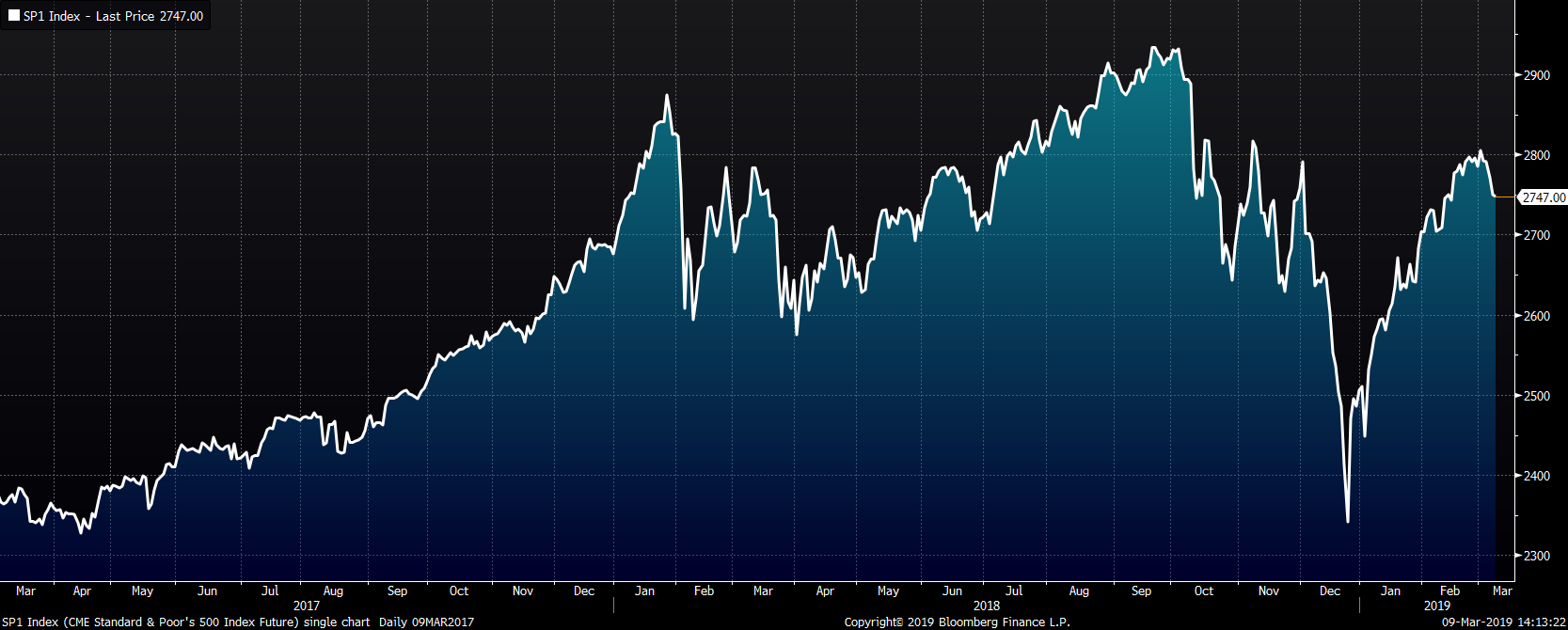

The S&P 500 was down 2.1%, while volatility climbed. Global markets were lower with the Nikkei falling 4.1%.

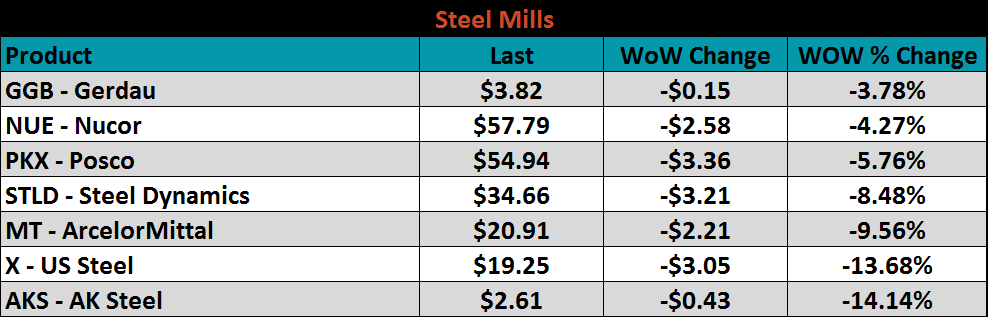

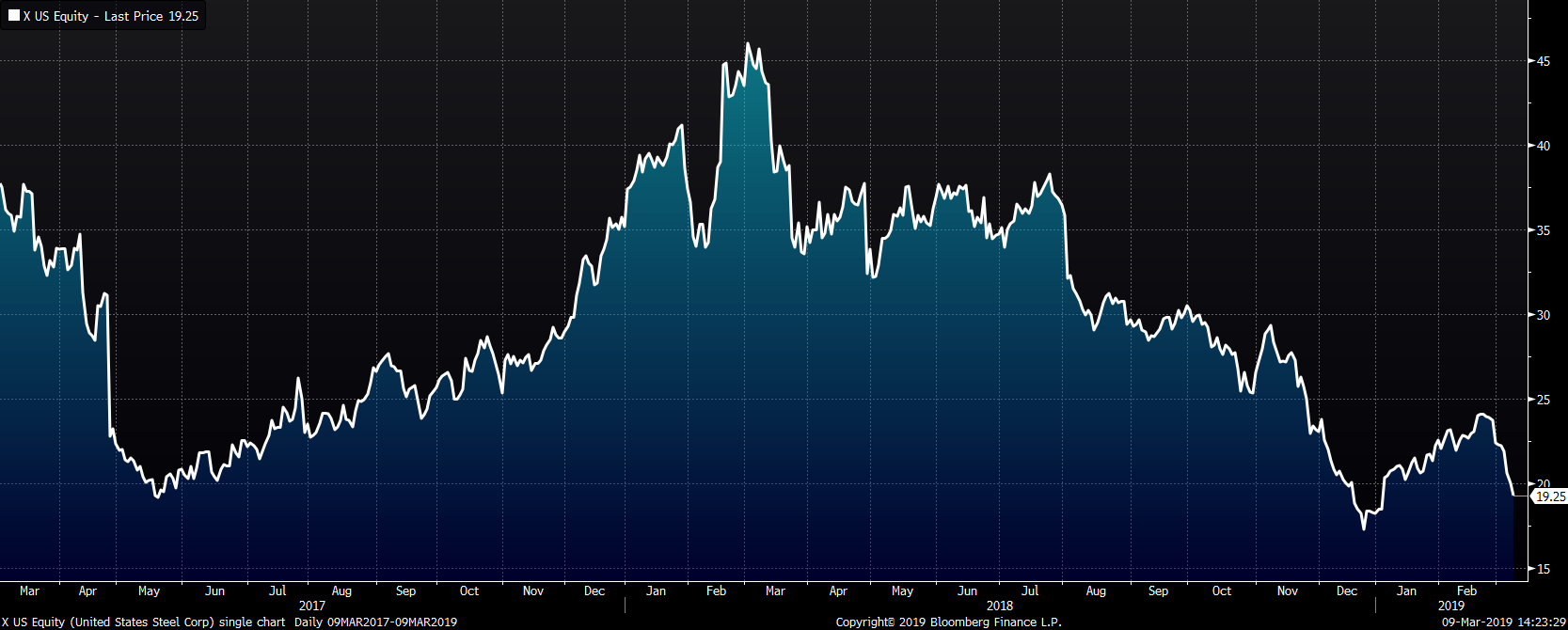

Steel mill stocks were all lower last week, led by AK Steel and US Steel down 14.1% and 13.7%, respectively.

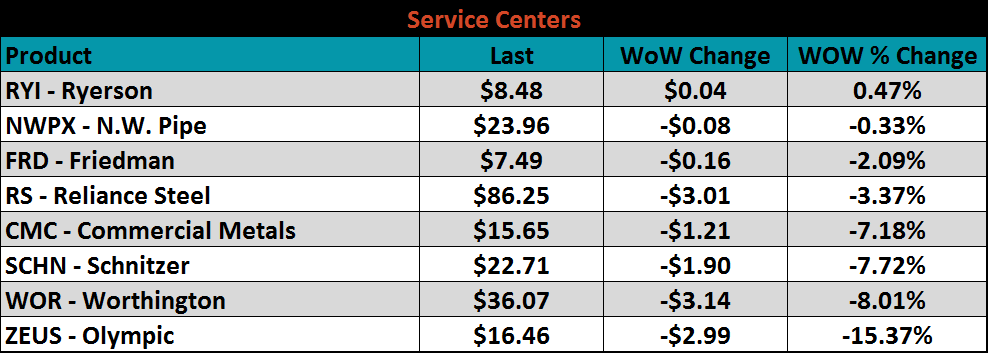

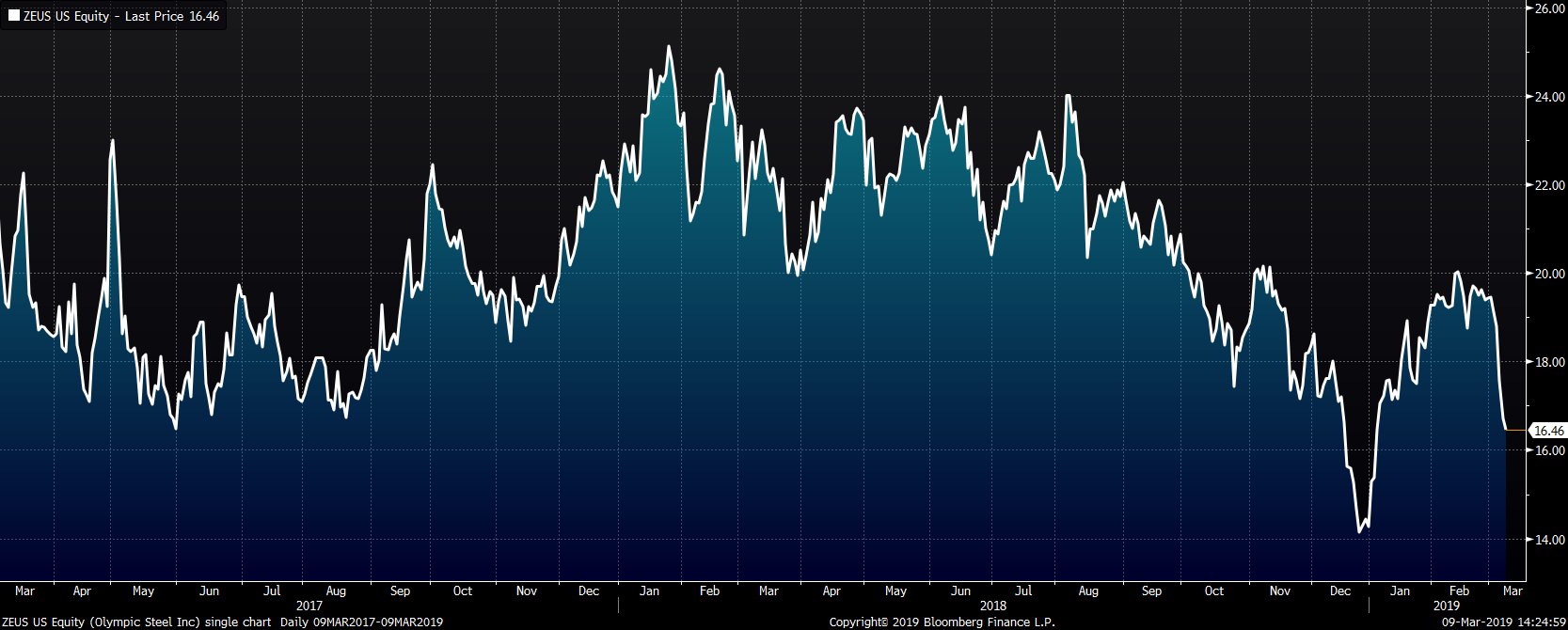

Service center stocks were mostly lower. Olympic was down 15.4%.

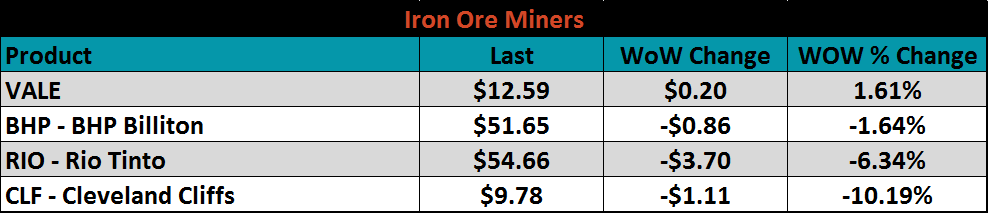

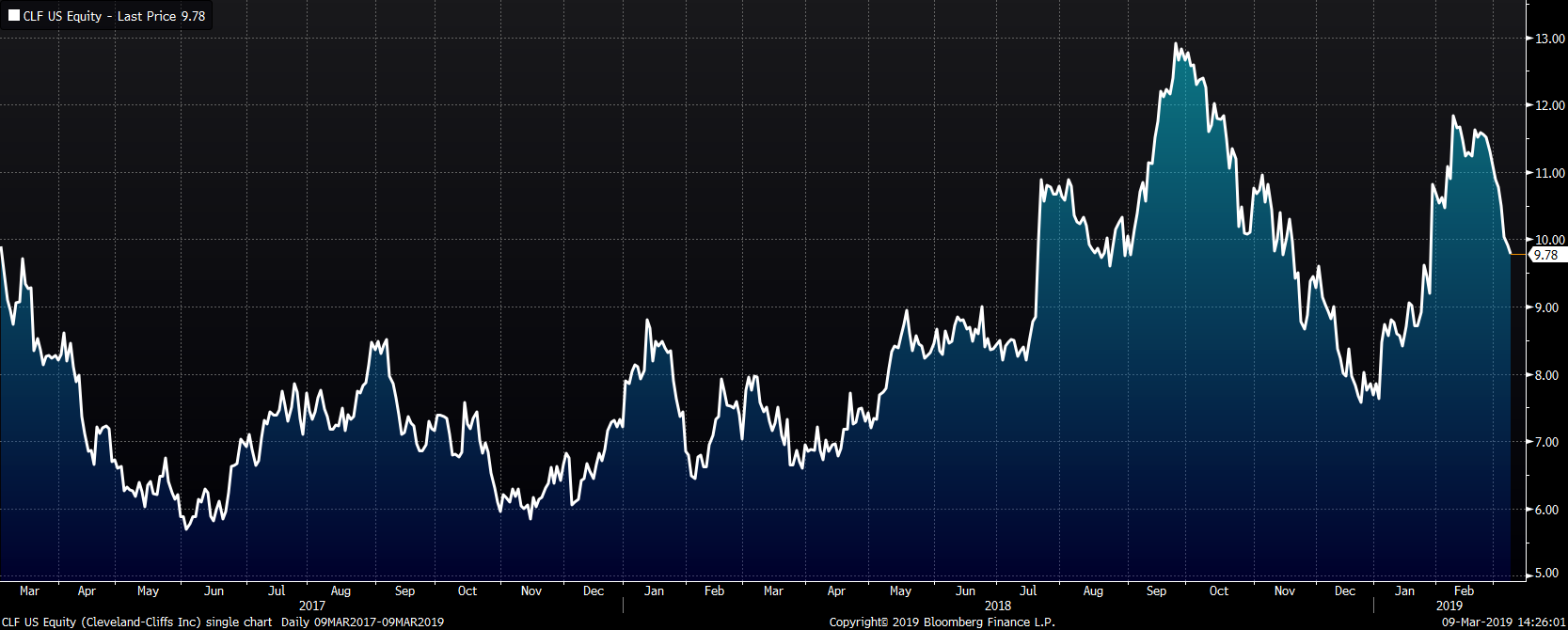

Mining’s stocks listed below were mostly lower. Cleveland Cliffs continued to fall, down 10.2% WoW.

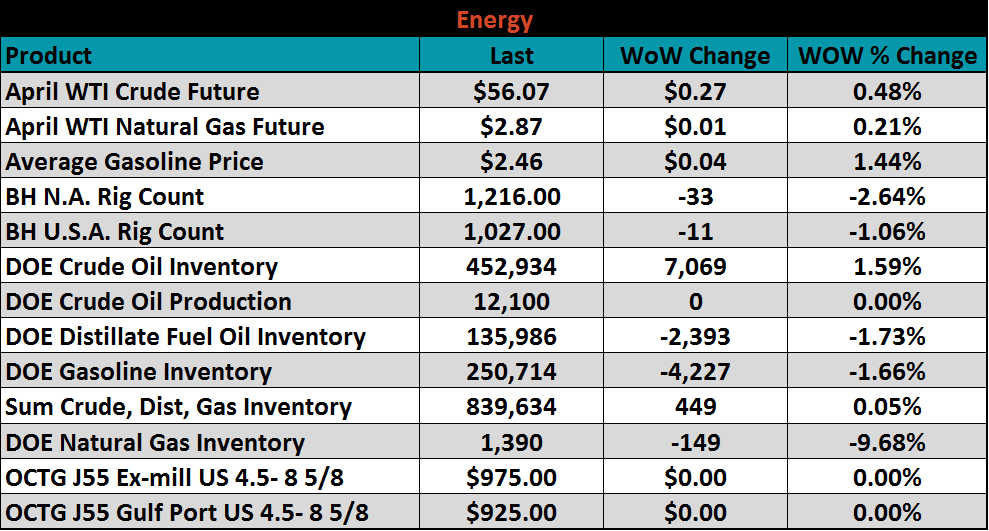

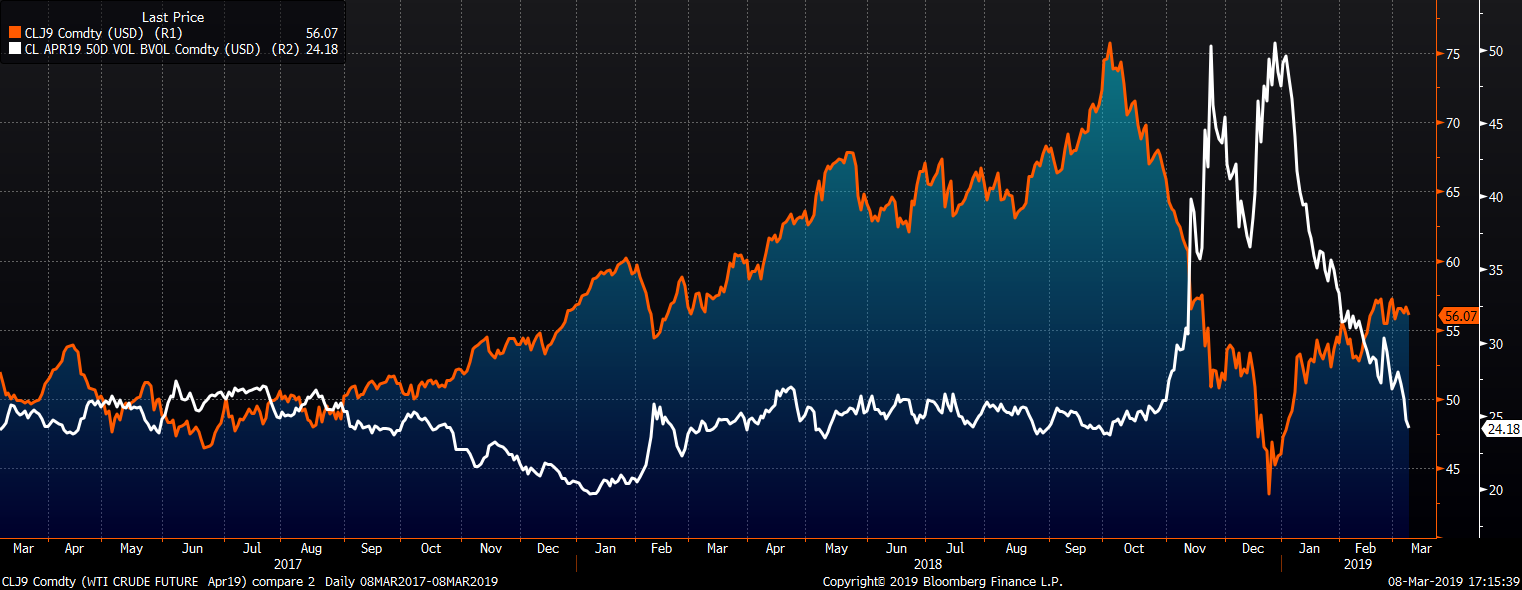

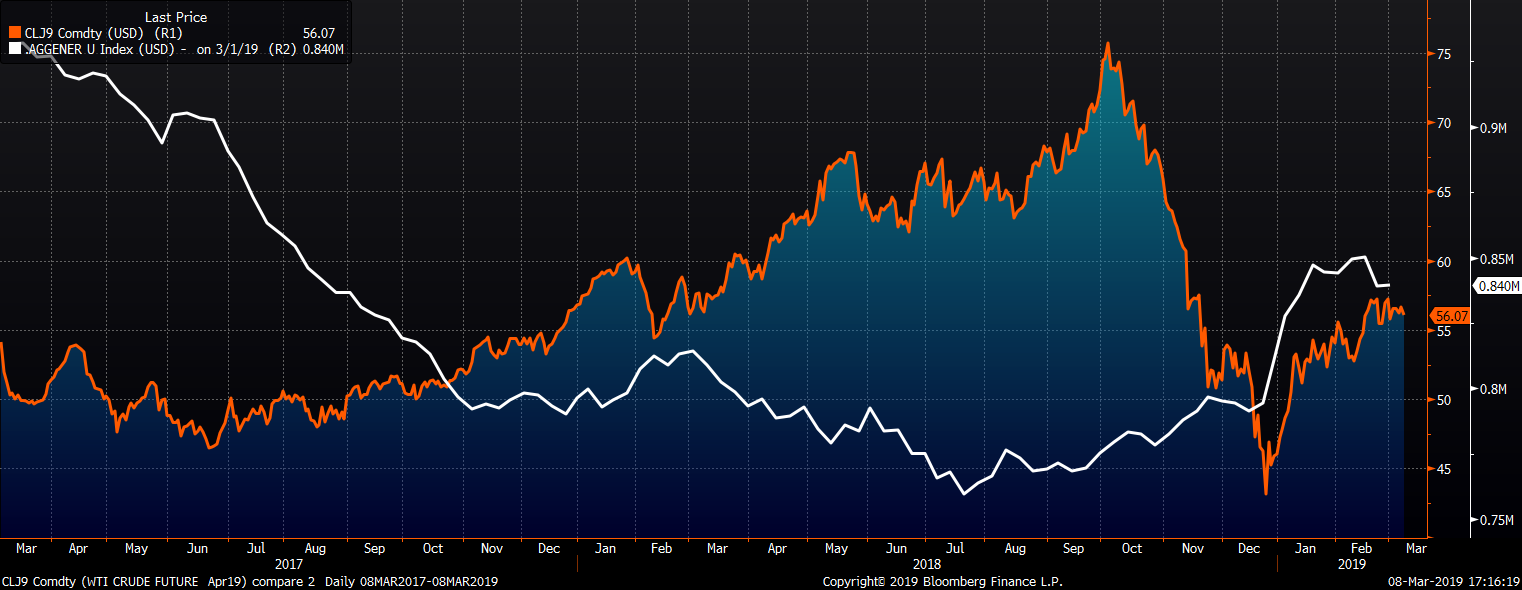

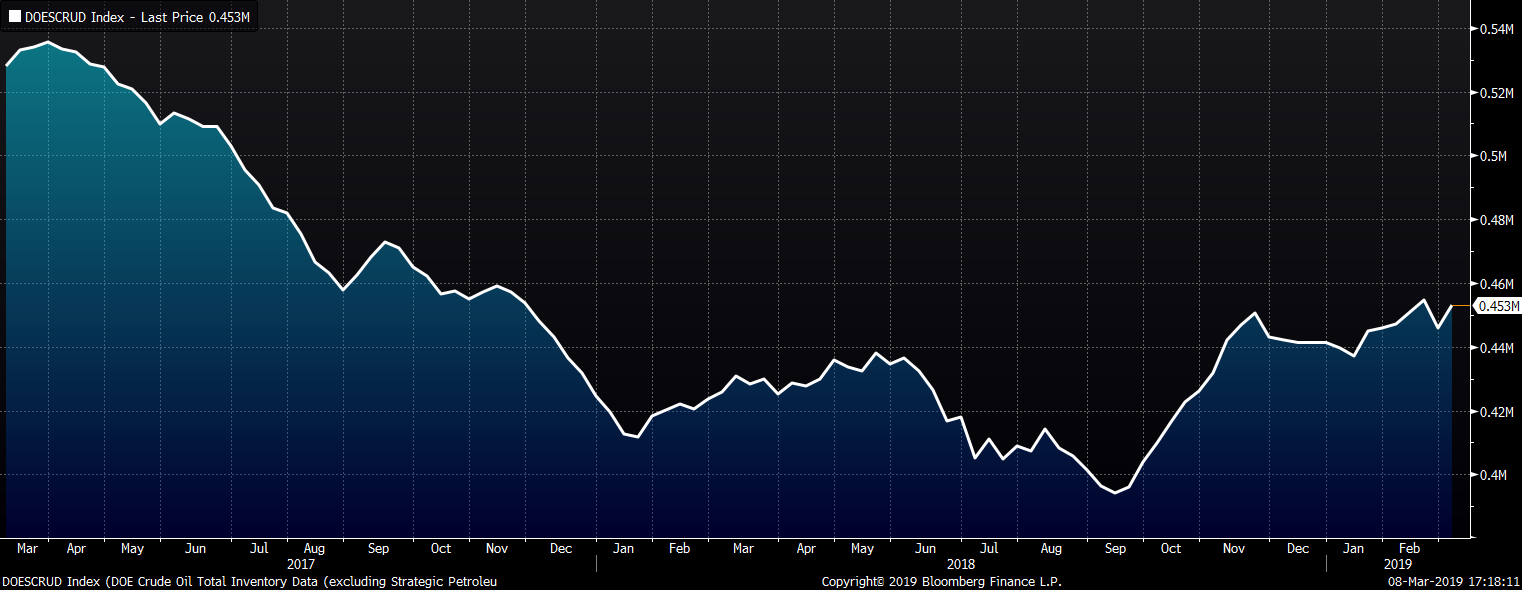

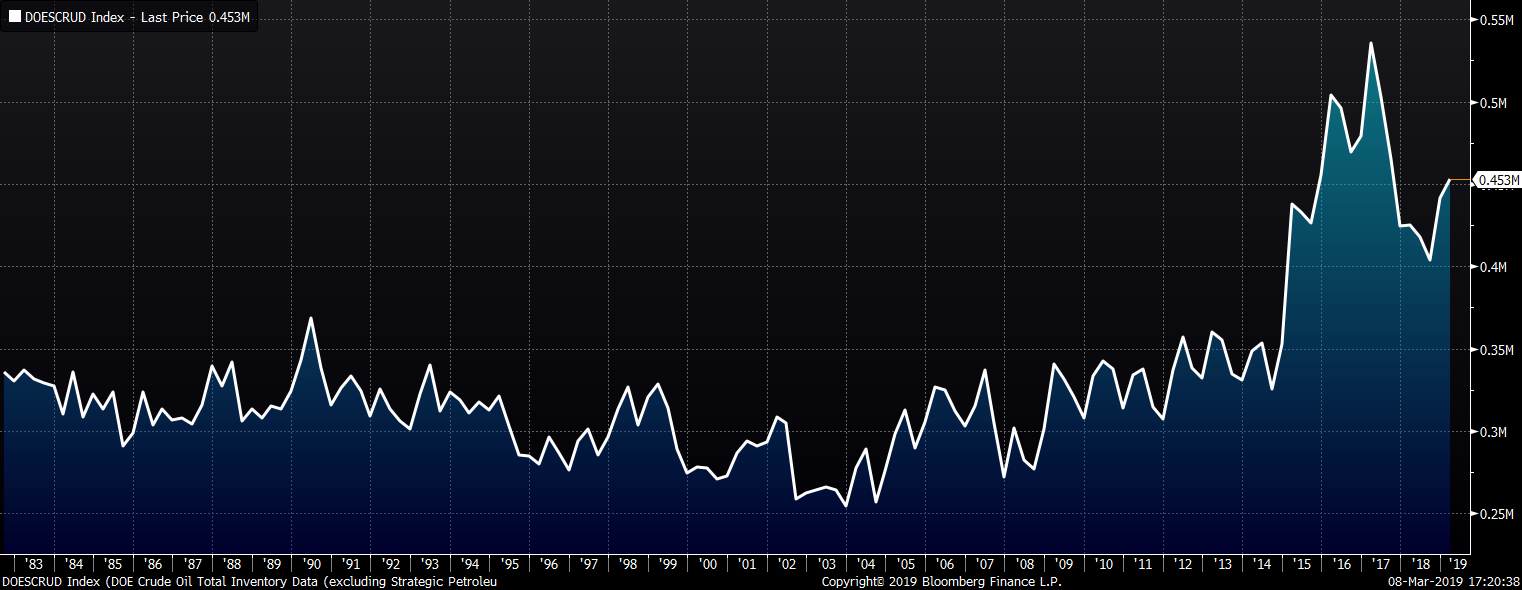

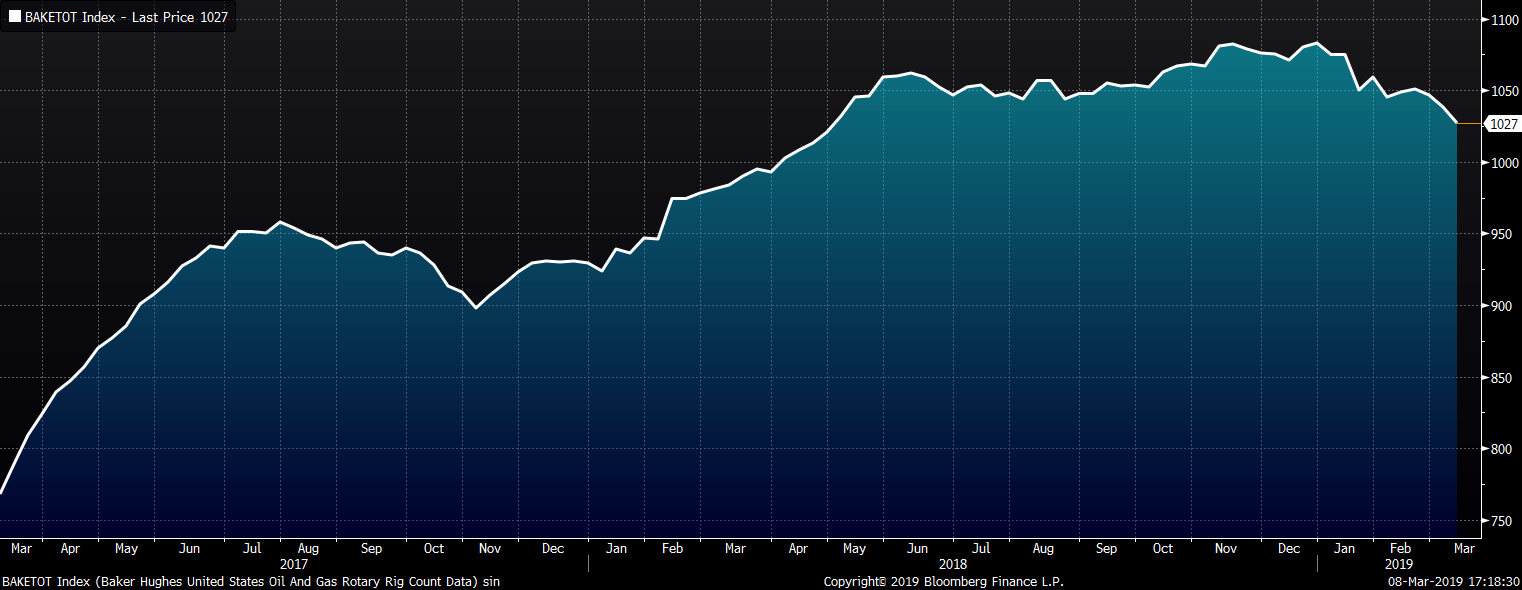

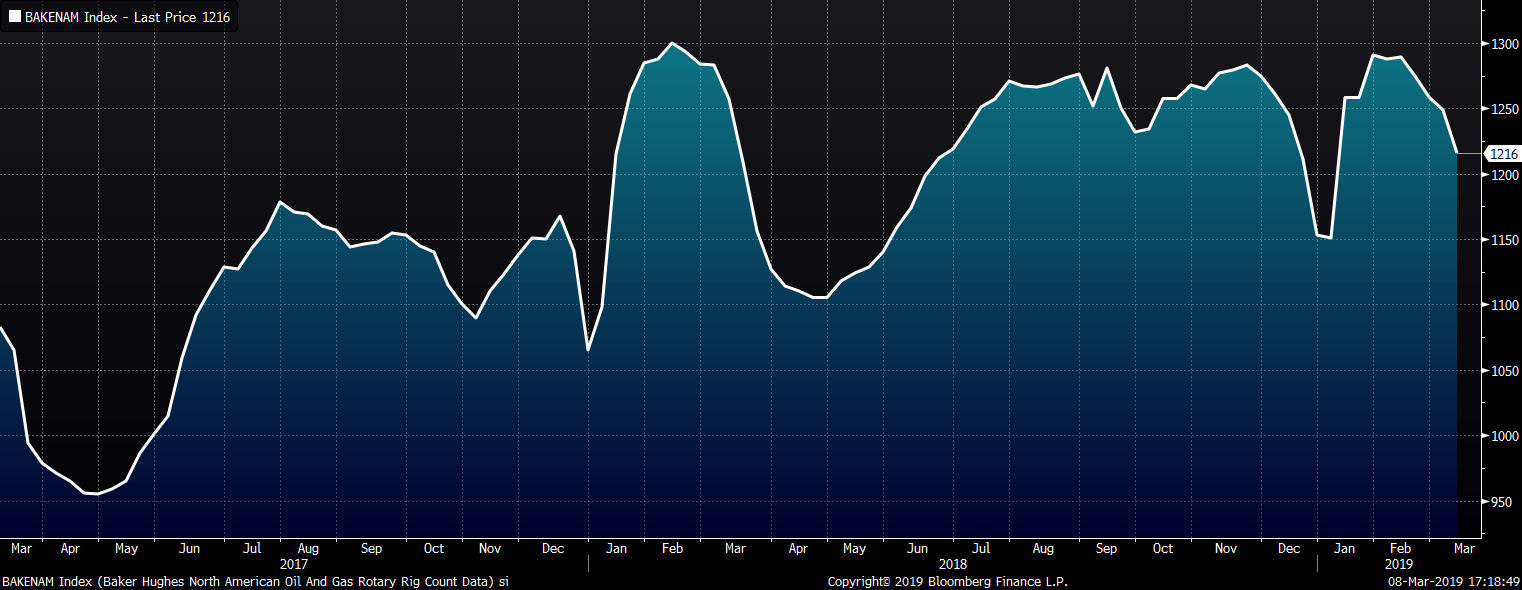

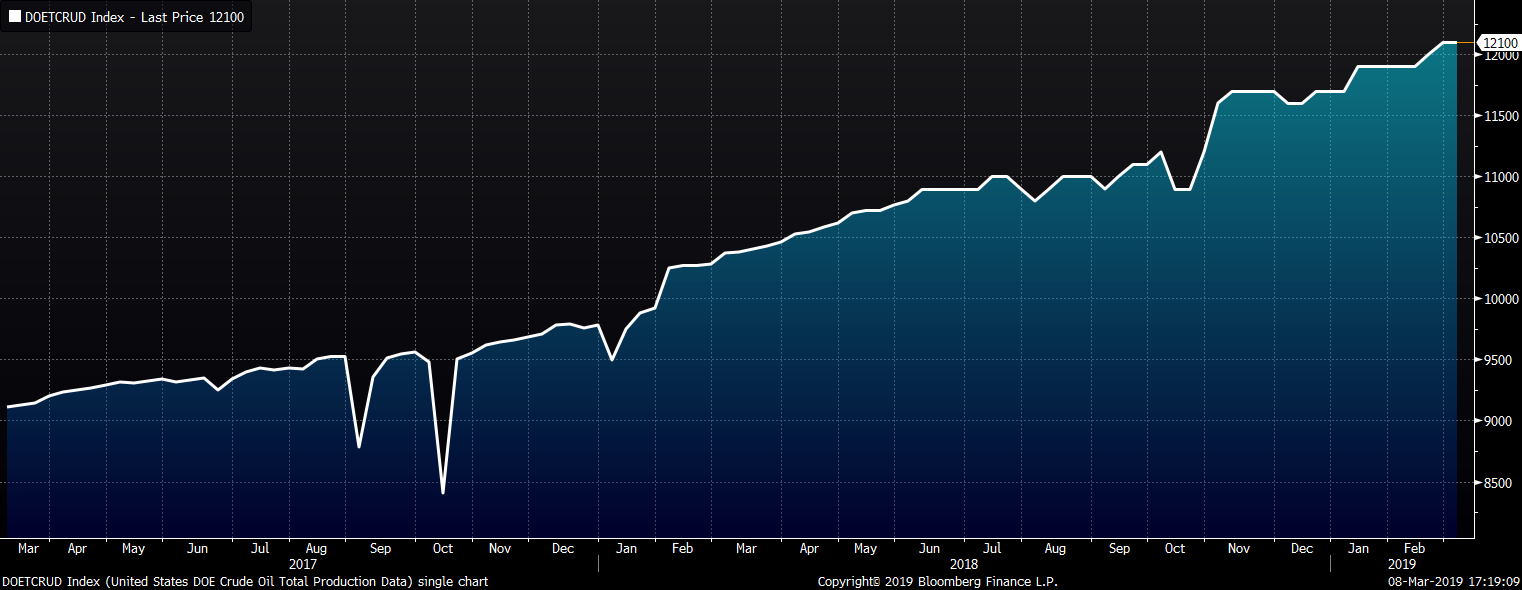

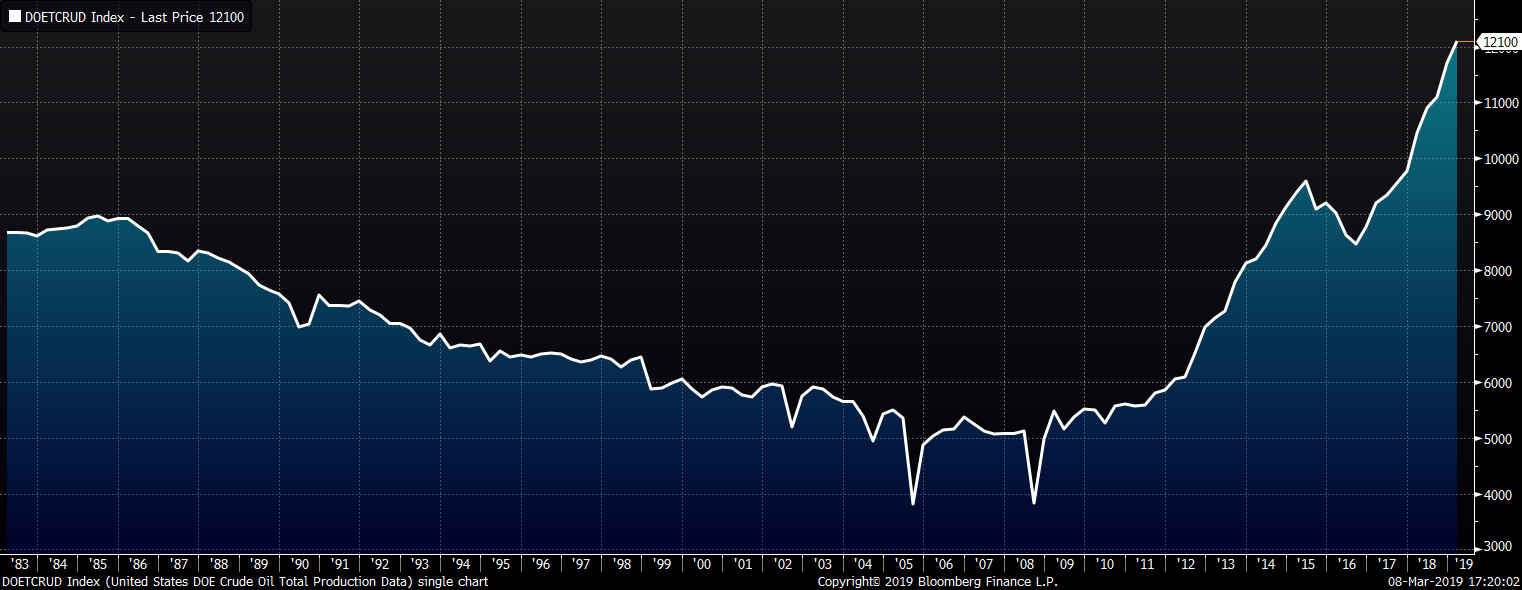

Last week, the April WTI crude oil future gained $0.27 or 0.5% to $56.07/bbl. Crude oil inventory rose 1.6%, while distillate and gasoline inventories each fell 1.7%. The aggregate inventory level was unchanged. Crude oil production remains at 12.1m bbl/day. The U.S. rig count lost eleven rigs while the North American rig count lost thirty-three rigs. The April natural gas future gained $0.01 or 0.2% to $2.87/mmBtu. Natural gas inventory fell 9.7%.

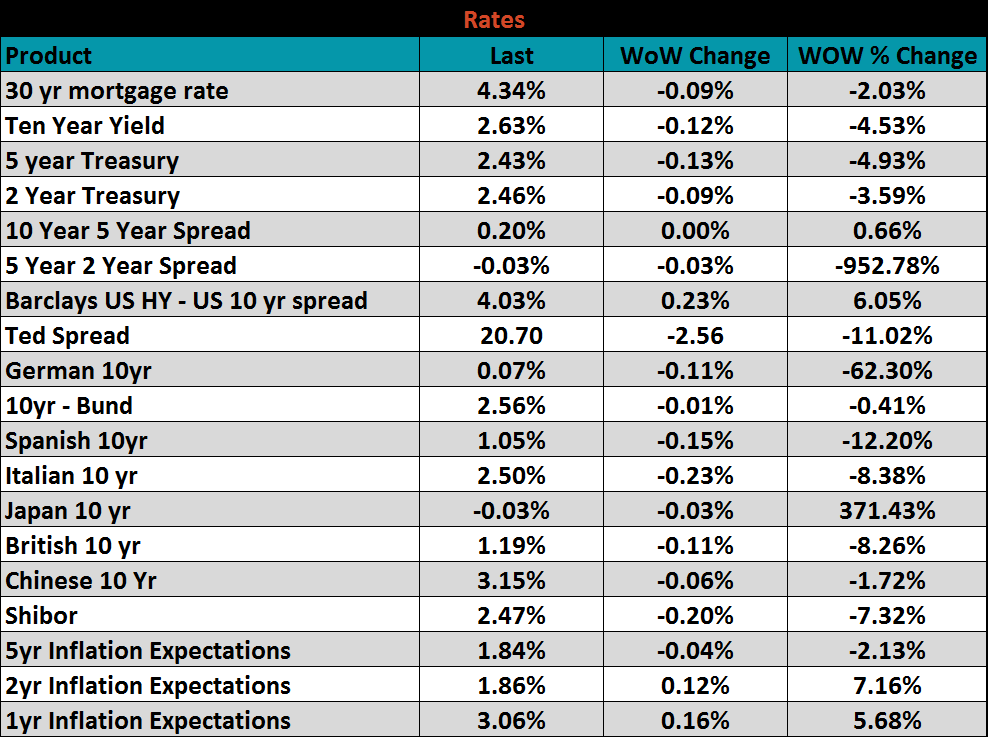

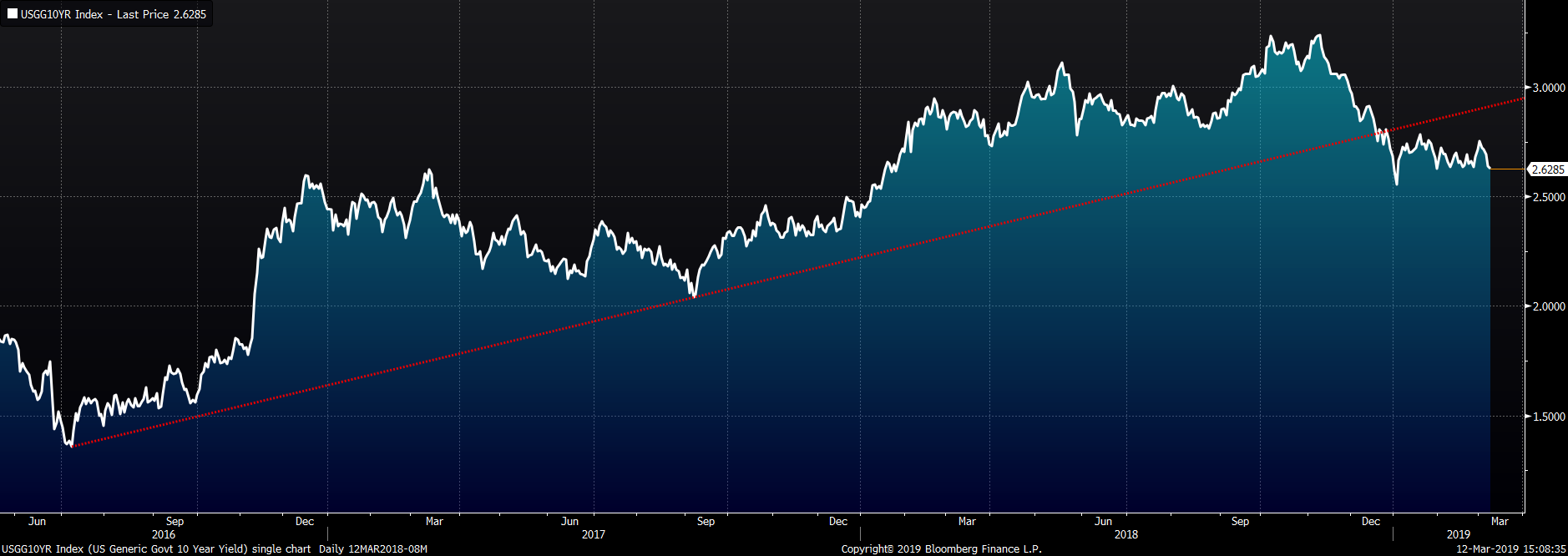

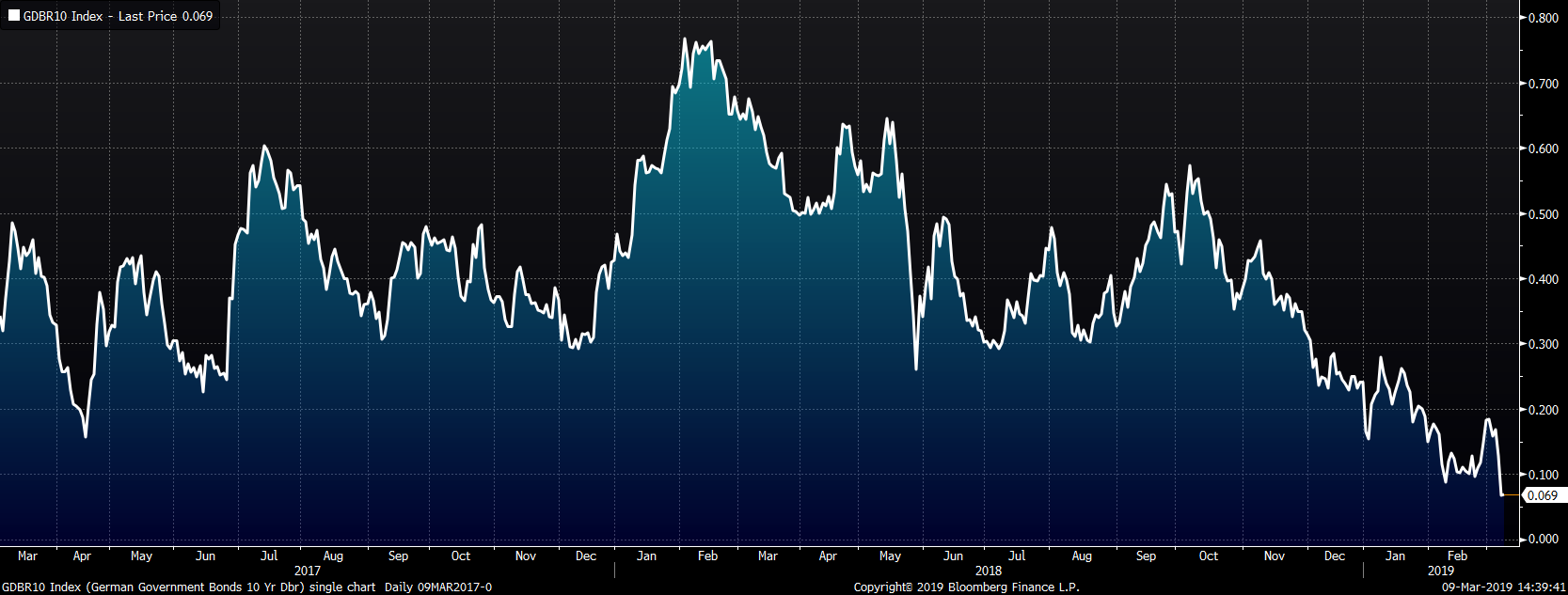

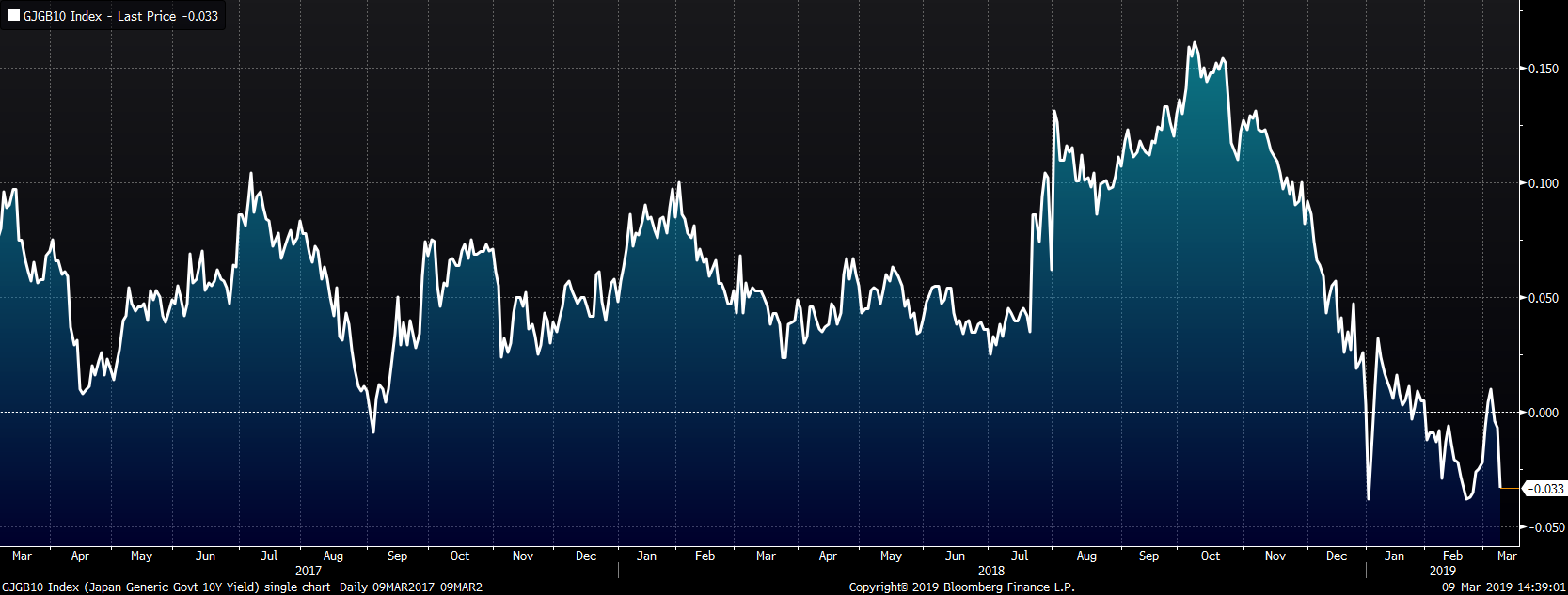

The U.S. 10-year treasury yield was down 12 basis points closing the week at 2.63%. The German 10-year yield was down 11 basis points to 0.07%. The yield on the Japanese 10-year yield lost three basis points ending at 0.03%.

The list below details some upside and downside risks relevant to the steel industry. The orange ones are occurring or look to be highly likely.

Upside Risks:

Downside Risks: